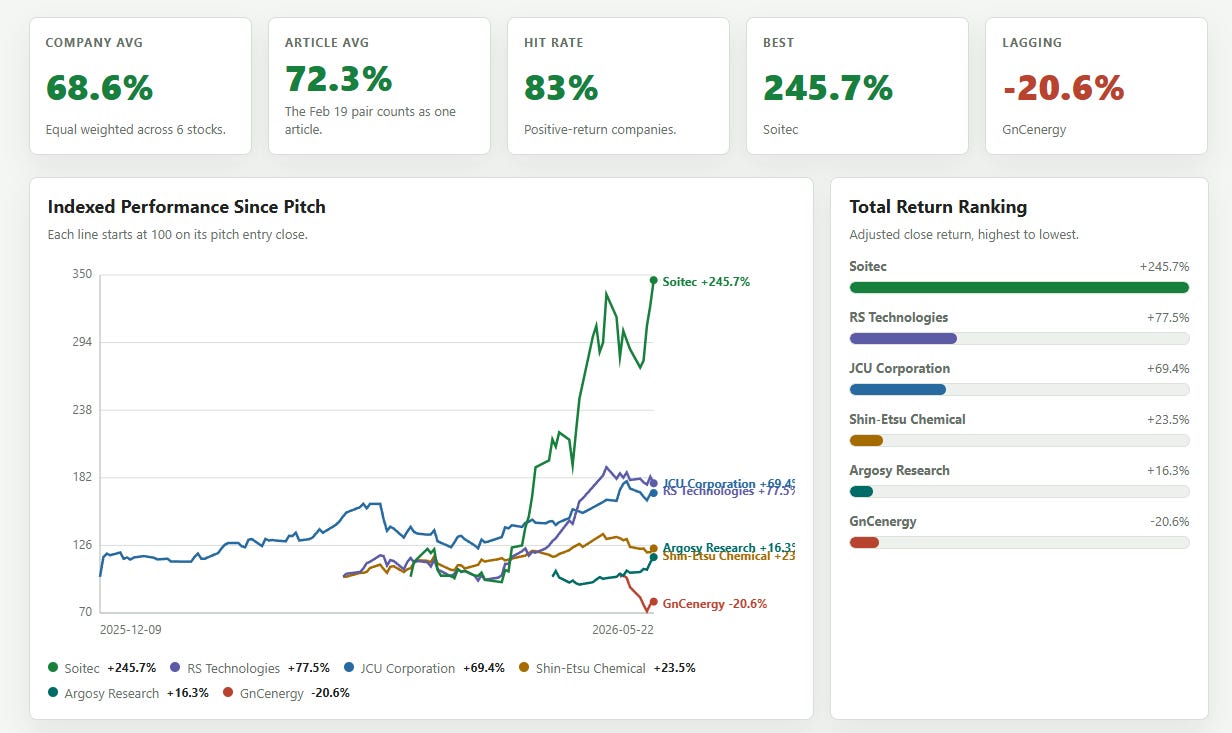

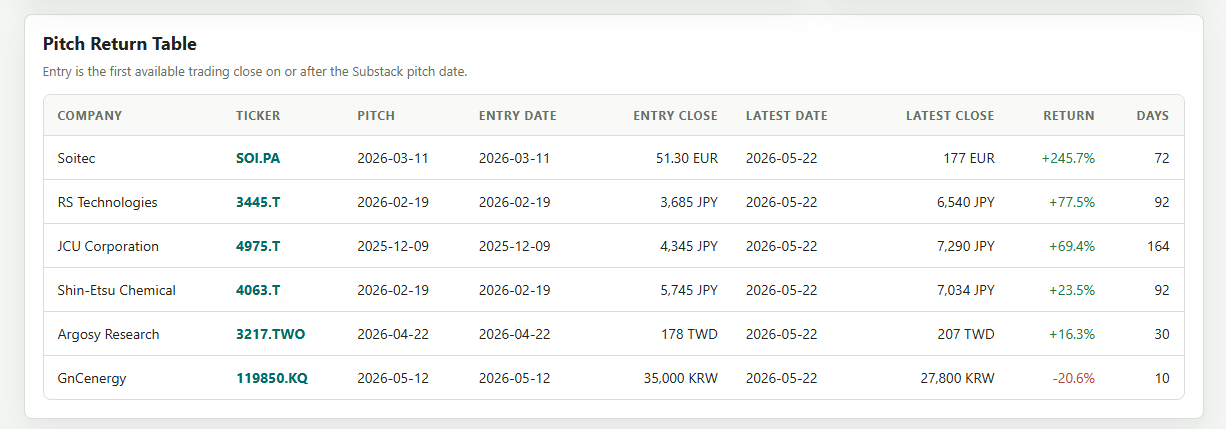

Update on positions

Since going paid- what I'm holding, what I sold, what I wish I held, and the lessons learned along the way

Since going paid in December with JCU Corp, we have done quite well. I thank you for your support.

I personally, have made some major mistakes. Not just this year, but I have become very aware that if I just held the stocks I pitched longer (since I started writing) I would have done drastically better. If I held one of the first stocks I ever pitched- $HRTG, I probably would have been retired 2 years after. (But I would never stop looking at stocks).

I have always sold too early, and I think this comes from an inherent risk-aversion. For the majority of my investing career I also held 50% of my portfolio in cash, waiting for a crash that never came.

Initially my rationale for holding so much cash was a good one, I was painfully aware of the Dunning-Kruger effect.

I also knew that getting to the point where you have looked at enough stocks to pick the good ones takes years of practice, extending the ‘peak of Mt. Stupid’ further out.

Investing is not like a tennis game where you hit 1300 balls a game and your neurons adapt after each hit.

It takes much longer because you need to wait months and possibly years to verify your initial thesis as new information is slow to come out. The price of a company shooting up or down short-term, is not a verification of a thesis, it is the market voting on the outcome.

I have been looking at stocks daily for almost 13 years now. And I do feel I am out of the valley of despair. Finally. That doesn’t mean the lessons are over, though.

Lesson I need to apply: I need to hold my winners.

My new strategy will be to sell 25-50% and sometimes 75% of my winners after massive runs (70-100%+). But to always hold some and let the market do its thing.

JCU Corp (+70%)

We will start with the pitch that began it all- JCU Corp.

JCU Corp was never meant to be a 10 bagger. I saw it as an extremely positive reward to risk play and I mentioned that in the pitch. The market has re-rated the company since then. I positioned myself extremely heavily in JCU because I thought the downside was minimal, and the upside had 50-100% in it. I have taken off most of the massive position since but now still hold a full position in the stock.

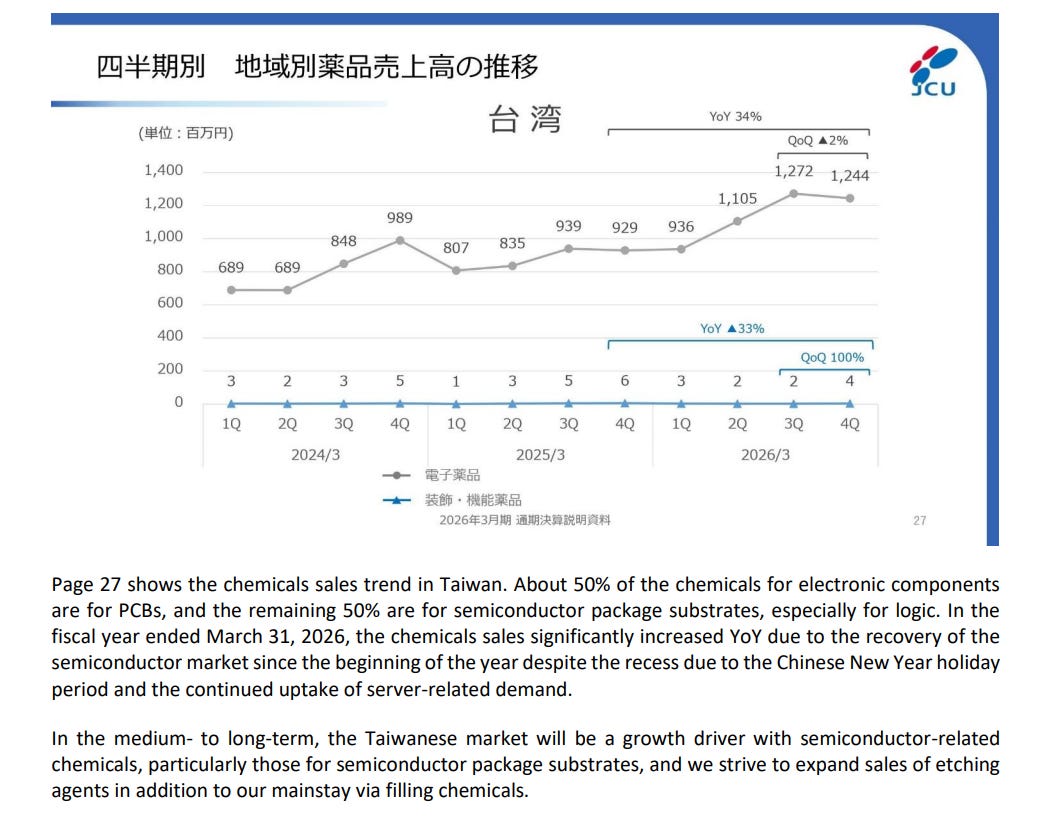

Recent earnings show increasing profitability, and most importantly- the increased memory prices have had a negligible effect on their via filling (80% of their operating profit) growth. I had assumed the softness in the smartphone market would lead to a decline in their biggest segment. It had minimal to no effect. Chemicals for high-end PCBs (mostly smartphones) have surprisingly been on the rise.

What about AI-Datacenter exposure? Our proxy for this is Taiwan, Japan, and Korea. Taiwan more specifically. I think it is lagging and we will eventually see out-sized growth from Taiwan because it takes a long time to qualify the chemicals in the packaging facilities. They have yet to come online.

Ibiden, Unimicron, are expanding capacity. They make the package substrates that are then filled by chemicals like CU-BRITE. They have to build the facilities and then they have to qualify the chemicals in the facilities. It all times a lot of time, and the bulk of the facilities will come online later. When these facilities are qualified, that is when I believe we may see a big ramp-up in the chemicals used to via fill PCBs.

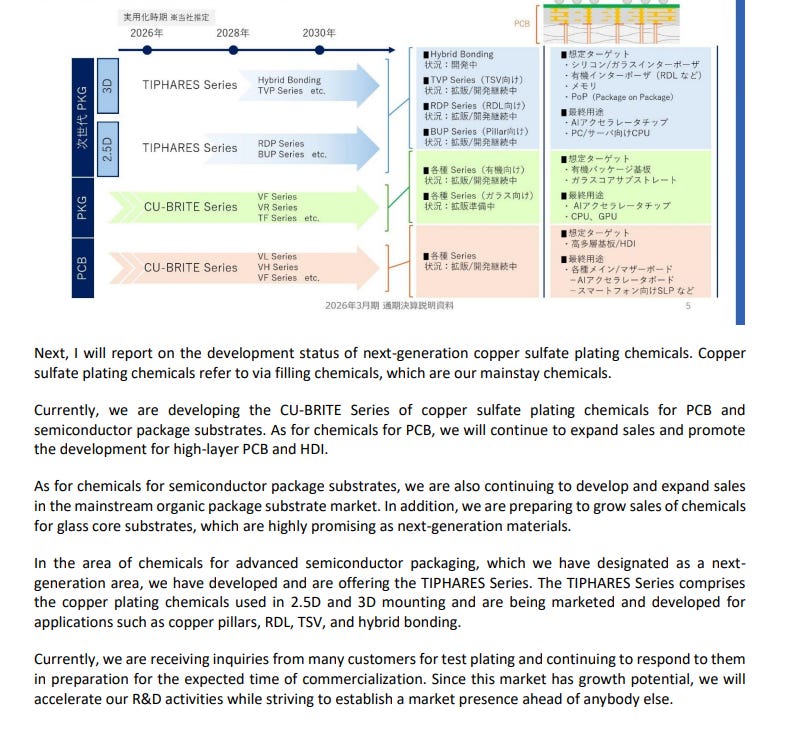

Then there is the TIPHARES, JCU’s line of surface-treatment chemical solutions and the Kumamoto facility near the TSMC Gigafab in Japan.

This is very important to the company, its the first thing they mention in their update.

JCU presents us with a lot of optionality too, as most of their current capex is to increase their exposure to the highest end semiconductor package substrates- as mentioned in the image above.

This all makes JCU look like a long-term hold. They are quietly positioned to do very well as capacity increases.

Current EV/EBITDA at 11.46x is a fair to bargain multiple to pay for a business that will probably see outsized growth into the future. I still don’t see much torque for the stock, the business is not like that, but I do see a steady compounder.

Position update: sold most of my super overweight position, now holding a full position of 7%.

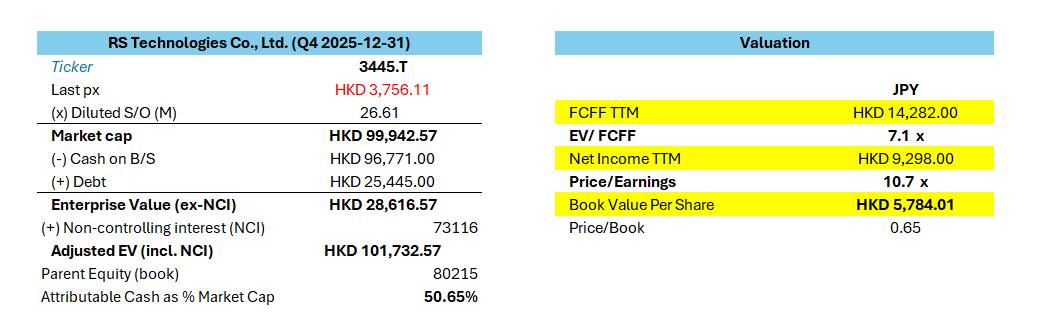

RS Technologies (+80%)

When I pitched RS Technologies it looked like quite an obvious and safe long. The company has surprised me. It re-rated quickly as the market realized it shouldn’t be lumped in at the same multiples as other prime-wafer businesses.

Reclaimed wafers are a different game, and the company does in fact have a qualification-like-moat at competitive price points.

My favourite thing about RS Technologies was the reward to risk profile. It was the kind of company I love to pitch because at the valuation (at the time) it had minimal downside (and 50% cash as a % of market cap). It’s hard to lose on companies like this.

For Q1, the overall outlook is positive.

The company saw an increase in revenue and margin in its reclaimed wafer business YoY and a 31% YoY increase in its prime wafer segment. It puts the company at a P/E of 18. Still relatively cheap due to the amount of cash it has on the books, but it does not have the same appeal now as when I pitched it initially.

Position update: I have sold 75% of my position.

Shin Etsu (+23%)

Shin Etsu’s electronic’s segment, now its biggest segment and highest operating margin segment, is exposed to almost everything chip-related. They make products for:

Front end wafer fab: Silicon wafers, SOI wafers, photoresists, hardmasks, photomask blanks, synthetic quartz mask substrates, pellicles

Back-end packaging, thermal protection: Encapsulants, liquid encapsulants, die attach, thermal interface materials, silicone coatings, low-dielectric materials

Adjacent electronics, infrastructure: Rare-earth magnets, HDD VCM magnets, optical-fiber preforms/coatings, LT wafers, PBN, compound semiconductors, QST/GaN.

Shin Etsu is a bet on longer term AI and datacenter demand.

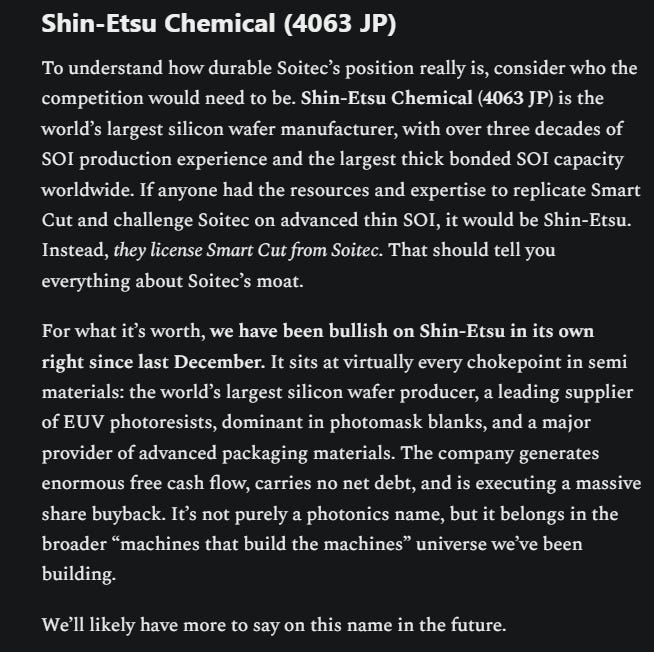

The company is also a photonics play. They have the largest SOI capacity worldwide (according to Citrini) and we are likely to see them start mentioning this market soon as the photonics buildout ramps up. They license Soitec’s smartcut technology and we have seen Soitec run up 245%! I believe Shin Etsu’s time is yet to come.

This from Citrini’s “Let there be light” article.

I think Shin Etsu will experience a similar dynamic to JCU Corp- where most of the growth lies ahead of it.

We are also watching the company slowly shift to a higher margin business as its “Electronic Materials” segment sees gains from the datacenter buildout and its infrastructure drags.

Position update: no change, holding a full position.

Soitec (+245%)

Soitec. Is there operating leverage? What about valuation? What do the Fundamentals say?

Disclaimer: This publication reflects my personal opinion based on publicly available information and my own independent research. It is provided for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any security. Readers should conduct their own due diligence and consult a qualified financial adviser where appropriate.

I found Soitec from reading Jason's Chips when he will still criminally underfollowed. I have no qualms pitching stocks from others when I believe in them— as long as I give credit where it is due!

I did this for Wasion Holdings, ChongQing Electric Machinery, and Thakral Holdings from Maius Partners. Wasion Holdings and ChongQing both did 80%+ and I have since sold both, although ChongQing might warrant another look.

Thakral Holdings has an extreme margin of safety and is only up 16% since the pitch. Deep value.

With the amount of Substacks and X accounts pitching stocks soon every stock on the market will have a pitch, and it will be our job again, to filter noise.

I have always wanted to build my own Substack around one goal- to make you money with limited downside while not posting noise. I will continue to pitch other people’s theses if I think it will make you money.

Thank you Jason for finding Soitec. I hope my subscribers made some money on it and didn’t sell early like me!

Soitec is currently up 245% since I pitched it. I learned a very expensive mistake on Soitec. I started weighting it more and more and ultimately paper-hands half of my position on a dip, and then proceeded to watch the stock double from there- then sold my entire position and watched it double again!!!!

(This is a major part of the reason I tend not to announce trades I do personally unless I get 100% out of a position or the thesis changes- because my analysis shows that just buying and holding the stocks I pitch perform better than I do myself!!! Lesson learned.)

I will admit that Soitec now has a much steeper valuation than when I first pitched it.

But things have fundamentally changed too- the photonics demand TAM expectations have increased drastically.

It is for this reason I wish I held. The optics buildout is truly gargantuan. Beating all previous expectations.

The Goldman-style thesis says AI networking shifts from “some pluggable optics at the network edge” toward massive numbers of optical links inside scale-out and scale-up AI fabrics. That creates demand for silicon photonics PICs, and those PICs are commonly built on Photonics-SOI wafers. Soitec is one of the key suppliers of those engineered substrates. They also benefit through the licenses they license out- to Shin Etsu, for instance.

Position Update: Sold out of all, but I wish I didn’t.

Argosy Research (+20%)

Argosy gives me a similar feeling to RS Technologies in its setup. It’s largest segment has bottomed out (SO-DIMM) and Server (R-DIMM) is growing at 30% annually.

I think the market hasn’t woken up to the fact that R-DIMM benefits from the CPU bottleneck- adjacently.

Agentic AI makes CPUs more important. More CPUs and CPU servers mean more DDR5 server memory. In conventional x86, that memory is usually RDIMM / MRDIMM.

It benefits because agentic AI likely increases:

CPU server count

CPU:GPU ratio

memory per CPU socket

DDR5 speed requirements

high-capacity RDIMM, MRDIMM adoption

RCD/PMIC/SPD hub content per module

As we see M2 become a bigger portion of Argosy’s revenue (it’s also higher margin with a bigger moat vs SO-DIMM and their M.2) we will see the company re-rate and probably do what RS Technologies did- a double.

GnCenergy (-20%)

Would’ve been nice to buy this dip but immediately after posting Korea, and a lot of Japan entered into a brief correction.

They also released earnings which I reported on here:

Think this one needs a bit more time to play out as their backlog comes into their income statement at much higher margins (my thesis).

Position Update: still holding a full position

Please leave me feedback on what markets you would prefer I focus on, and what kind of value you get out of this Substack.

Thanks for the shout out, Davy!

Congrats on your success! We’re in the throes of an historic bull run for an intensely cyclical industry. I’d argue for some more nuance in your decision rules about which stocks to #neversell and which to scale out of completely as they rip.