Soitec. Is there operating leverage? What about valuation? What do the Fundamentals say?

Finally, a photonics exposure at a more than fair price.

Disclaimer: This publication reflects my personal opinion based on publicly available information and my own independent research. It is provided for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any security. Readers should conduct their own due diligence and consult a qualified financial adviser where appropriate.

Soitec

Soitec caught my eye after reading Jason’s article.

This strapping young lad (Jason) is doing some great research, I suggest you read his article before you continue with mine.

As a generalist, I want to understand Soitec’s operating leverage, bottleneck potential, moat, and valuation.

I do not have a specialist know-how, but I have relied on my fundamental knowledge of companies to make money.

Before we can even get to valuation, we need to understand a few things, quite briefly:

1- What Soitec actually makes?

2- Is there a moat, is it hard to make?

3- Is there operating leverage? If there is enough demand, can they pump them out and capatilize on that with economies of scale?

4- Roughly, what will the demand for SOI wafers be in future

Once we know this we can get to

Valuation- and how that relates to how fast the company will grow.

Fortuantely, Jason already answers most of our questions in his article.

I finished reading his article and thought- “I need to understand the nitty gritties of the valuation, how many of these SOI wafers the market will demand (roughly) and whether that leads to a blast off in operating leverage”.

I look forward to reading his parts 2-7, but I’m too impatient and I want to undrestand this business more thoroughly, right now.

I’m going to recap a bit, because as a generalist I still needed to wrap my head around what this company actually does.

1- What Soitec actually makes?

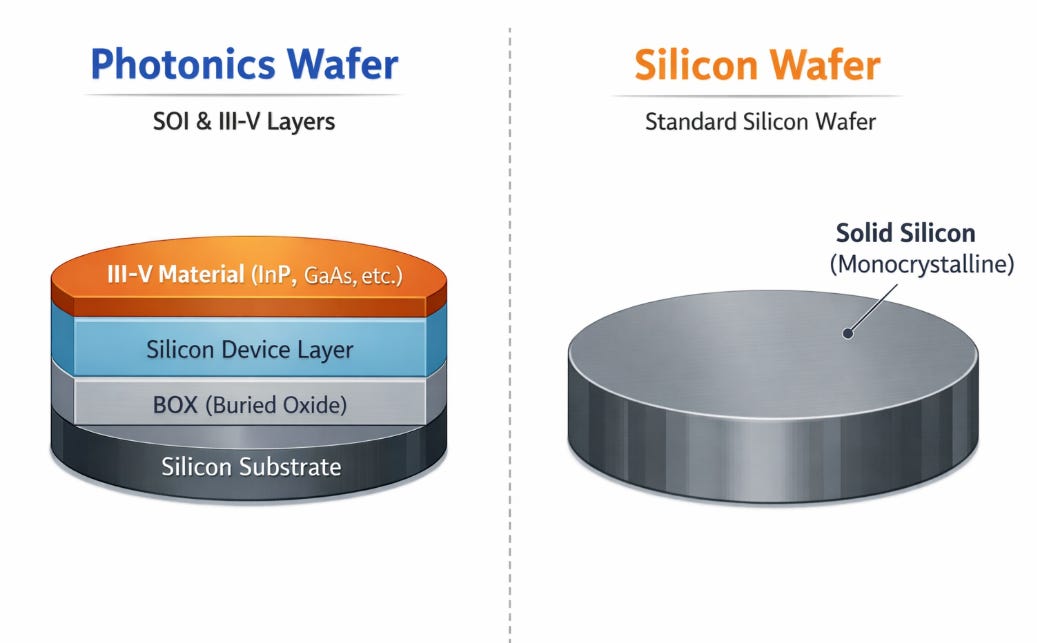

We’ve got a Soitec SOI wafer on the left, and normal wafer on the right.

Companies we’ve spoken about- like Shin Etsu, and RS Technologies, (and there are tons of others), make wafers. RS Technologies makes the wafers on the right. Shin Etsu makes both. Soitec makes the ones on the left.

The big risk to our ‘normal’ silicon wafer companies is that everyone now knows how to make them. China is increasing capacity a lot.

When it comes to SOI wafers, Soitec has a special process- its Smart Cut Technology. It actually licenses this out to Shin-Etsu Handotai (owned by Shin Etsu). So great! Shin Etsu also makes photonics wafers! We are positioned well! (But probably a small % of revenue…for now…).

Back to Soitec- they ALSO manufacture these SOI wafers themselves.

2- Is there a moat, is it hard to make?

Jason has described the moat quite nicely.

Smart Cut™ - This is the foundational enabling technology for engineered SOI substrates and Soitec says it underpins nearly all SOI wafers sold globally.

The moat exists.

3- Is there operating leverage?

There is. Via its own manufacturing capacity for SOI wafers and also via its royalty stream.

And what is even better is that the licenses are royalty based- so Soitec will benefit from any increase in demand for SOI wafers. This means if there is a ramp up (which is coming next year and beyond), Soitec will get close to pure profits from Shin Etsu, and other companies that hold Soitec Smart Cut licenses.

That is pure operating leverage if you ask me.

The company also has operating leverage in the form of its own manufacturing capacity.

The company has publicly disclosed their capacity too, on their site.

It’s very likely that Soitec can rellocate their mix within the SOI lines, I’m just assuming this because BERNIN 2 for instance says that they can produce multiple SOI types.

But the royalty revenue will impact the bottom-line (net profit) directly, and that is pure operating leverage without the risk of expanding capacity.

Pure profit play.

Which means any potential bottleneck that leads to a price hike would also be captured via the royalty stream.

From Soitec’s filings: in FY2024-2025, Soitec reported €891 million of consolidated revenue, and its customer mix table shows “Other customers/royalties” = 13% of revenue.

We don’t know how much of “Other” is purely royalties. But 13% isn’t small, especially when it comes with almost 0 cost. Also, most of the end markets where these SOI wafers are used in, are only actually coming to market in 2027. So this is very early.

4- Roughly, what will the demand for SOI wafers be in future

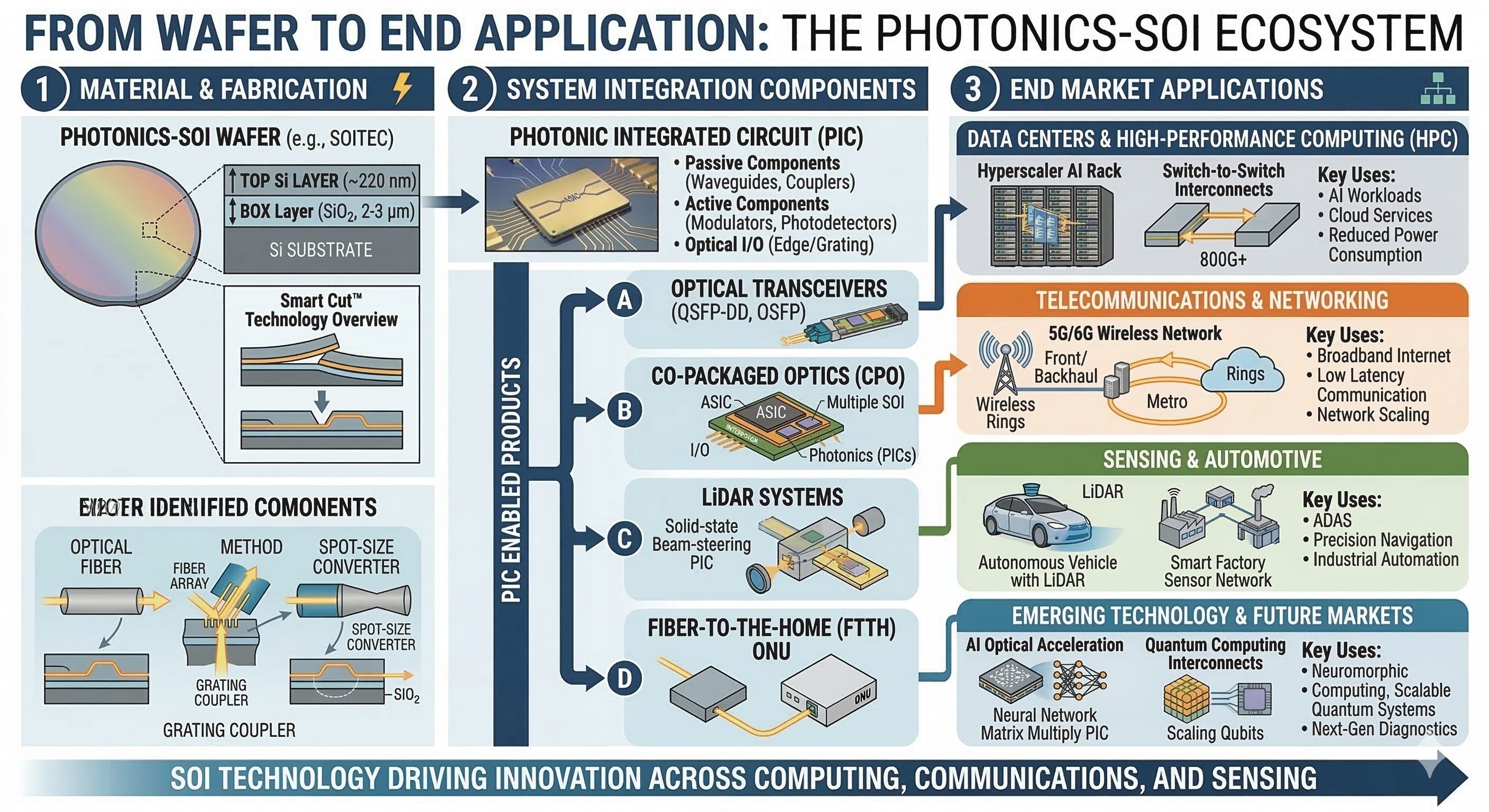

These SOI wafers are used to make Photonic Integrated Circuits (PICs) which are used in things like Transceivers (think AAOIs recent management call about the insane demand for transceivers for 1.6T) as well as is CPO (Co-packaged Optics).

We have already had real world proof from AAOI incoming orders and management commentary that this space will be insanely massive.

Companies like Coherent, Lumentum, AAOI, make products that use PICs (photonic integrated circuits). The insane demand we’ve seen in this space will certaintly lead to a massive increase in SOI wafer production.

The fact that most SOI wafers produced use Smart-Cut technology mean that Soitec will certainly benefit.

Let’s try and quantify it, roughly.

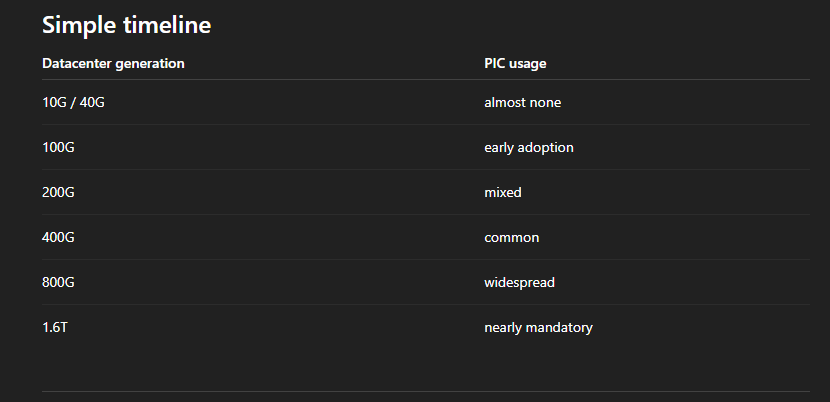

The evolution of PICs used in Datacenters:

I will publish my full demand/supply model for the wafers in the next post (free). It will require more work because their are different kinds of SOI wafers to account for, which have different end uses.

The setup is compelling and demand appears to be building rapidly, and Soitec looks unusually well placed to capture that upside. At roughly 6.5x EV/EBITDA, the stock still does not strike me as priced for that possibility, which made it easy for me to add to the position.

I am long.

My conviction really strengthened once I built out the valuation, which is where I think the numbers start to get interesting.

5- Valuation- and how that relates to how fast the company will grow.

This is how I have modelled the business based Soitec’s own SOI wafer capacity. I have also used bullish assumptions.