The Founder Is Keeping This Stock Cheap on Purpose

And he's on a deadline. Worldex: the signal, the timetable, and my targets.

Disclosure (this is now my second biggest position — added after the 29th June meeting results came out). I might add more, I am getting more and more bullish.

The market is pricing this company as if there isn’t a memory capacity expansion and as if the cash on the books will never be seen by shareholders. For good reason too — governance, which I believe is changing.

The asymmetry involved is striking.

The company is already valued as if cash will be trapped forever. The pessimism is fully baked in, and even in my bear case, the company is worth more than it is here. There is a reason for this too: the founder needs to keep the price low for tax reasons, but only for now.

There is a clear signal that will indicate to the market when that time is up.

Valuation snapshot (at the ₩28,700 close, July 3, 2026):

Market cap: 16.51m shares × ₩28,700 = ~₩474bn

Less net cash: ~₩220bn (₩230bn cash & financial instruments, minimal debt)

Enterprise value: ~₩254bn

EV/EBIT ≈ 4.3x trailing (FY2025 EBIT ₩58.6bn)

EV/EBITDA ≈ 3.3x trailing (EBITDA ~₩78bn)

On my FY2026 estimates that falls to ~3.3x EBIT / ~2.6x EBITDA, and on FY2027 to ~2.7x / ~2.3x — the market is paying less for this business every year the capacity build compounds.

While competitors trade at EV/EBIT of 10x+.

If you want to catch up on the business, I analysed it in the post below. This article will focus solely on the governance. And our pathway to alpha.

The Best Memory Trade Isn't a Memory Stock

This article is for informational and educational purposes only and does not constitute investment, legal, tax, or financial advice, or a recommendation to buy or sell any security. The author may hold a position in Worldex (KOSDAQ: 101160) and could transact at any time without notice. The analysis reflects personal opinion and includes forward-looking estimates and assumptions that may prove wrong; figures are drawn from sources believed reliable but not independently guaranteed, and some (including legal interpretations and probability weights) are the author's own judgment. Korean securities, tax, and corporate law are complex and fact-specific. Do your own research and consult a licensed professional before investing. You alone are responsible for your investment decisions.

This situation is COMPLICATED, but it is damn well worth understanding. I think there is money to be made here.

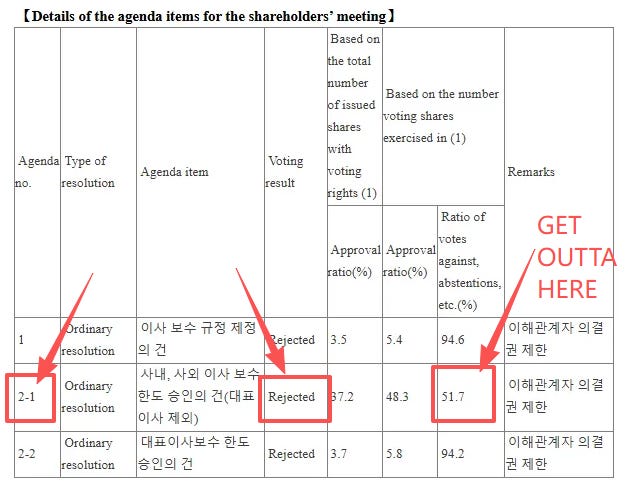

On the 29th of June, shareholders rejected ALL of Bae’s (CEO, Founder, Controller) ordinary resolutions.

These 3 resolutions were all trying to vote on similar things — exec pay. Egregious amounts of it.

The 2-1 ordinary resolution is important to understand (red boxes above). It was a vote on execs’ compensation excluding Bae’s pay — and this means that Bae himself and his full 35% ownership could vote — which is why the vote was so close at 51.7%. This is crucial because even when you include Bae’s full 35% vote, the other shareholders came together and politely told management to go and “F*%$ themselves”, and rejected the vote.

This was his last desperate attempt in my opinion.

In ordinary resolutions 1 and 2-2, Bae’s full 35% was excluded because of a rule where controllers cannot vote on their own pay. Which is why we see it lost by such a large margin.

This is insanely bullish because prior to the meeting, Bae pulled out all the stops for this meeting to try and raise his pay:

He disabled e-voting.

He forced a stamp process to introduce friction for proxies.

He forced an in-person meeting in Gumi.

And he got voted down.

The outcome of this vote is insanely bullish for Worldex minority shareholders. (not because they won anything, but because it means they can win).

It is far more bullish than I expected it would be.

I did not expect the minority shareholders, against the disabled e-voting, against the frictions, to be able to vote Bae down when his full 35% share vote counted.

The share price did a nice 10% pop on the news, but the next day it didn’t go anywhere. I think the market is completely asleep on this name — while Hana Materials trades at a 3x higher valuation on a P/E basis. Especially when I regard Worldex as the better financial operator vs Hana.

I really do believe this is only the beginning for Worldex shareholders.

Worldex is exposed to the biggest HBM capacity buildout in history — which will be a tailwind for more than 5 years (most likely). Memory prices aren’t what matter to them — it’s the capacity buildout.

At a price to earnings of ~10, with nearly half the market cap sitting in cash, and an activist that just beat the founder’s full 35% stake in an open vote — this changes the game completely.

But here’s the part almost nobody understands, and it’s the exact reason the stock is still this cheap:

The man with the most information in this situation is deliberately keeping the share price down. Legally. Methodically. And on a deadline.

Worldex is priced the way it’s always been priced — a company trapped inside a family. Succession, the Korean edition. Except Logan Roy is 75, cornered, and running out of calendar. The suppression that created this price has an expiry date — and it’s written in statute.

Better still: there is a single public filing that starts the clock. It will look like nothing — a routine disclosure most investors have never read and wouldn’t recognize if it printed in front of them. But the day it drops, everything after it is already choreographed: a quiet window I can time almost to the week, then the concession that unlocks ₩230bn of trapped cash, then a March 2027 meeting where the founder must win four separate votes from a register that has already beaten him at full strength.

The market will reprice when the results hit the headlines. The money is made by knowing what to watch before they do.

Behind the paywall:

The signal — the exact filing, who files it, and why it means the rest of the script is already running. My scraper watches DART for it every day; the moment it prints, subscribers hear it from me first — chat and email.

The tax mechanic that dictates the entire sequence — once you see it, the founder’s every move for the past 18 months snaps into focus.

The statutory deadline — why his whole strategy dies on one specific date in March 2027, no matter what he wants.

My base, bear and bull targets — including why my bear case is roughly the price on your screen right now.