The Best Memory Trade Isn't a Memory Stock

The company trades at my bear case, the upside to peers is 3X

This article is for informational and educational purposes only and does not constitute investment, legal, tax, or financial advice, or a recommendation to buy or sell any security. The author may hold a position in Worldex (KOSDAQ: 101160) and could transact at any time without notice. The analysis reflects personal opinion and includes forward-looking estimates and assumptions that may prove wrong; figures are drawn from sources believed reliable but not independently guaranteed, and some (including legal interpretations and probability weights) are the author's own judgment. Korean securities, tax, and corporate law are complex and fact-specific. Do your own research and consult a licensed professional before investing. You alone are responsible for your investment decisions.

Disclosure: I own this stock.

Also* The stock has been moving while I have been writing this up- so some prices/valuations are stale- but still not close to my bull case- the “catalyst” has still not activated.

I think I have found the Korean version of Succession, except instead of a media empire, the family drama is sitting on top of a deeply undervalued Korean semiconductor consumables company exposed to one of the biggest memory capacity expansions in history.

This company, on a comparable basis, should trade at around 3X its current valuation. Easily.

But first we need to understand the fun stuff.

The company is Worldex and the CEO and founder is Bae Jong-sik- he’s our Korean version of Logan Roy. A Tycoon and a real turd to be honest. (Sorry Bae- but you are).

He was born in 1951, so he is 75, and he has still not properly implemented succession to either of his sons. The two sons currently own 0% of the shares, which is the entire game. The founder needs to gift his shares to his son, and he wants to gift them at the lowest possible price. A low price means a lower gift-tax bill, which could save the family billions of won. But time is running out.

After the succession happens, the incentives flip discretely to align with minority shareholders- and this is, along with a recent passive shareholder now flipped activist, is why the governance situation is so interesting, and so ugly, and so ripe with opportunity once you understand the outcomes.

(I will go into depth into these governance events, and how I am going to play it later in the article).

The tactics used by Bae Jong-sik are dirty, but he is fighting what I believe to be a losing battle- against activists, and against the new Korean pro-minority shareholder policies.

The company previously tried to push through a golden-parachute style clause that could have allowed special severance payments of up to 20X the three-year-average salary, on top of the ordinary retirement allowance, if directors were dismissed before the end of their term due to hostile M&A. That clause was removed after shareholder opposition, including opposition from VIP Asset Management- which is our Knight in shining armor.

In Succession terms, VIP Asset Management would represent the largest activist shareholders who see massive value in the company, but need to fight Logan Roy to get it. And last week, on the 9th of June, they went even more activist- VIP filed to change its holding purpose from “simple investment” to “general investment”, increased/confirmed its stake at 15.64%, and formally pushed for buybacks, cancellation, higher shareholder returns, and TSR-linked executive pay.

This followed the 26 March 2026 AGM in Gumi, where VIP’s CEO reportedly attended in person, opposed Worldex’s director-compensation proposal, and, with the controller’s votes restricted, helped minority shareholders defeat it with 69.2% voting against.

69.2% voting against.

There is a caveat: Important voting wrinkle: the family’s ~35% stake did not have normal voting power here. Because this was a director-compensation proposal, the founder/controller was treated as a specially interested party and his votes were restricted. So, for once, the minorities actually mattered — and they voted it down.

This is the new South Korea, baby. The age of tycoons is over. How are you going to make money with this?

Let’s first understand the juicy undervalued gem that is Worldex. Then I will get into how this situation likely plays out.

Worldex

The company is called Worldex and they make Silicon parts mostly (73% revenue), quartz parts, and fine ceramics.

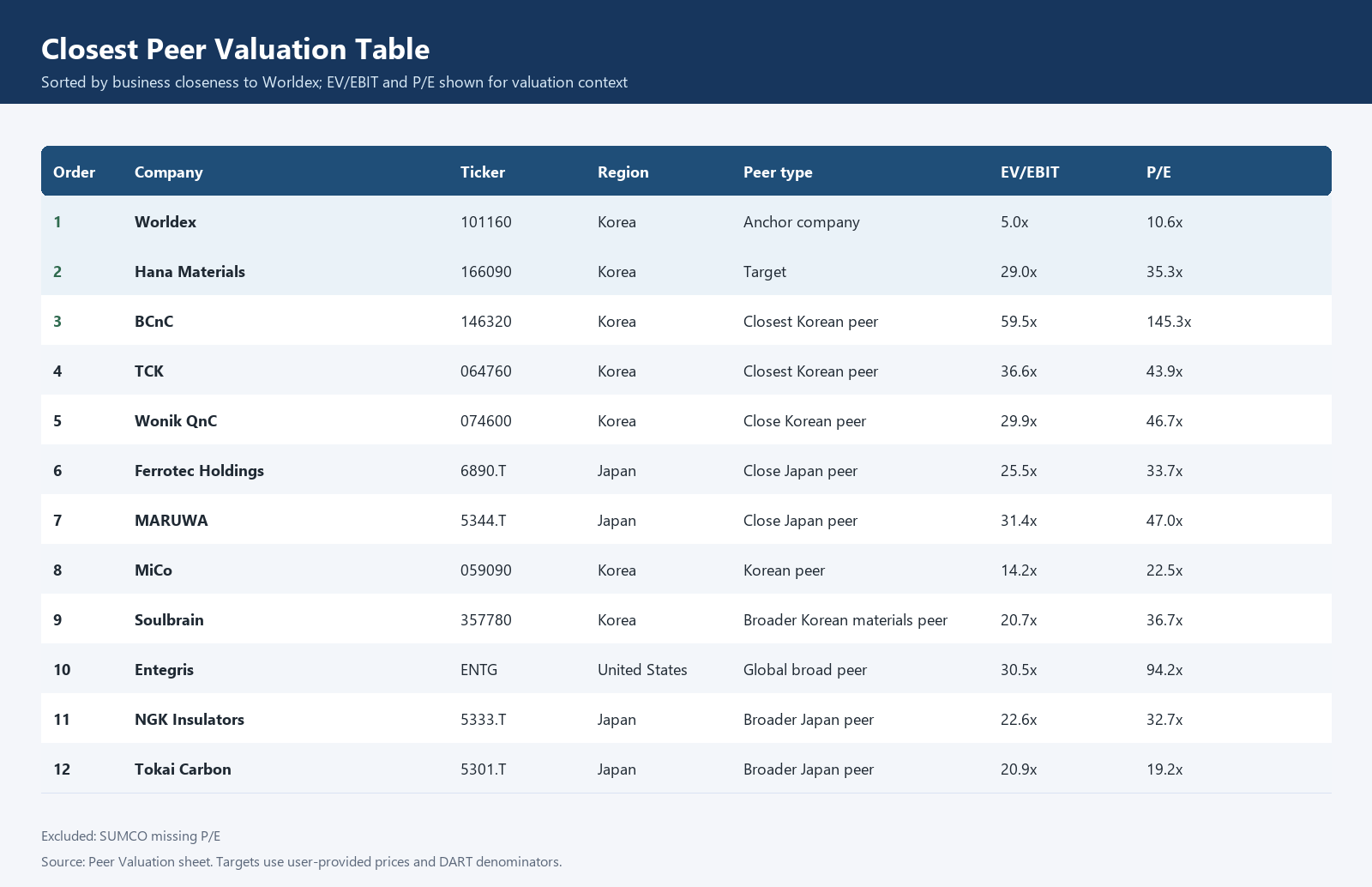

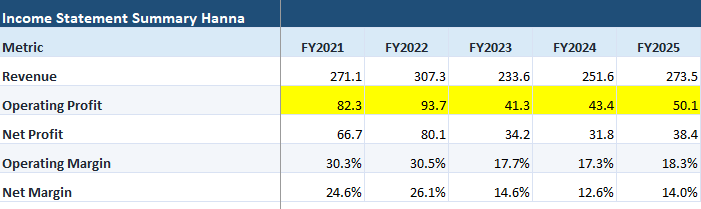

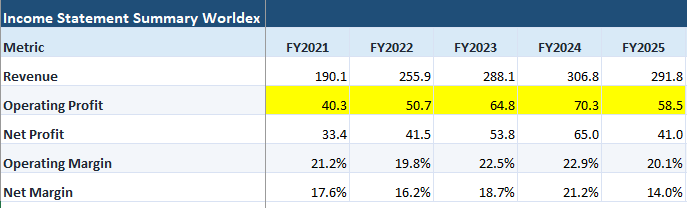

Their closest competitor is Hana Materials and trades at around 3X the valuation- except that Worldex has better financial operating metrics- Worldex will benefit from the demand draw created by SK Hynix and Samsung Electronics the memory makers expand capacity. The most recent financials for Worldex showed that 45% of their revenue came from SK Hynix and Samsung Electronics.

This is the valuation sorted by closest peer. The valuation is rather striking.

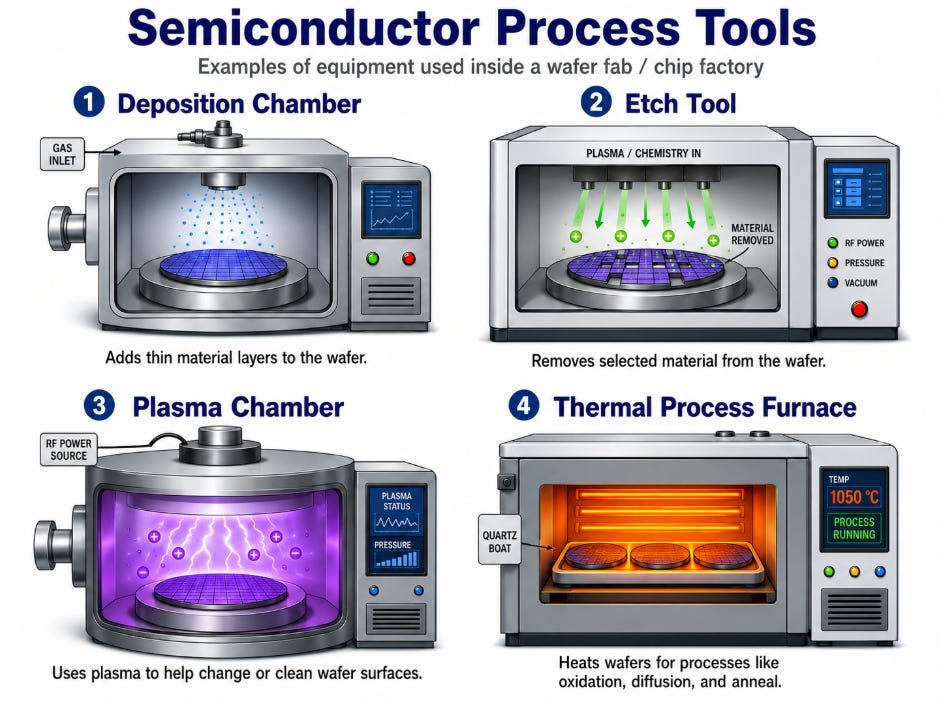

Silicon Parts are used in semiconductor process tools (machines) that make wafers. Plasma or etch chambers that could be running DRAM etch, HBM, 3D NAND etch, logic or foundry etch, other processes.

Worldex is an “after-market” supplier of silicon parts, quartz parts, and fine ceramics and other, whereas Hana Materials is a “before-market” supplier.

What does this mean? It means that when the memory makers like SK Hynix, Samsung Electronics, expand capacity, players like Lam Research, Applied materials, (and a few others) who make the machines you see below order directly from Hana Materials for the silicon parts- the silicon focus rings, silicon electrodes, etc, that go into the machines. They order from Hana first.

This is why Hana Materials is called a ‘before-market’ supplier. Their Silicon products are used to fit the machines first.

Worldex is mostly used after the products depreciate, and need replacement.

Worldex stated that 45% of Q3 revenue came from Samsung Electronics and SK Hynix. Worldex was registered as an SK Hynix supplier in 2001 and Samsung semiconductor supplier in 2002, they have been qualified a long time.

Don’t get me wrong now, there should exist some kind of a discount, which I will explain later, but in the face of one of the biggest memory capacity expansions in history, Worldex trading at a P/E ~10 and EV/EBITDA of 3.8, is far too cheap.

The reason for the massive discount, is governance, and which we delve into deeply later. The story is changing very quickly.

Worldex at a EV/EBITDA of 3.8 has a massive margin of safety due to its current valuation and a surprisingly clear path to future revenue growth- SK Hynix said to double memory capacity in 5 years and I wouldn’t be surprised if we hear the other memory makers following suite.

This tweet by Jukan is also favorable in the general direction for Worldex, not because it means Worldex will absolutely get price increases, but it points to the actual demand benefiting the entire chain.

Where things get even weirder- valuation-wise.

Hana Materials is considered Worldex’s most direct peer or competitor, BUT

Worldex does more revenue, more operating profit, and more net profit

YET Hana trades at a market valuation of 1.34T KRW.

Worldex trades at a market valuation of 424.33B KRW.

Hana Materials trades at a P/E of 27.

Worldex trades at a P/E of ~9.

Today the company released a “value plan” which was bearish, in my opinion, but the bottom seems to be in for this company, so the market took it as bullish, and the stock rose +10%

The reason for this massive discount, is governance. But that’s about to change, you just need to understand how to play it.

But there’s more- if the price rises before a “gift” is done- the bull case may only materialize much much later. It’s complicated.

The point of this article is not to convince anyone to rush and buy the stock, I believe there is opportunity here, but within bounds, and the situation needs to be understood completely to extract that opportunity.