$HKG: 8371 Taste . Gourmet Group Ltd

Multi-bagger cheap Hong Kong Stock: 8.5% + Dividend, Growing at above 30% for the last 3 years, PE = 6.8, EV/Earnings = 4.7

Mini Table of Contents:

Restuarants

Financials/Valuation/Peers

Risks

Executive Summary

A rapidly expanding restaurant holding company with a unique business model, achieving over 30% growth annually for the past three years and well-positioned for continued high-paced expansion. With revenue that grew even during COVID.

Operating in a geography with strong economic fundamentals, further bolstered by favorable government policies creating a powerful tailwind.

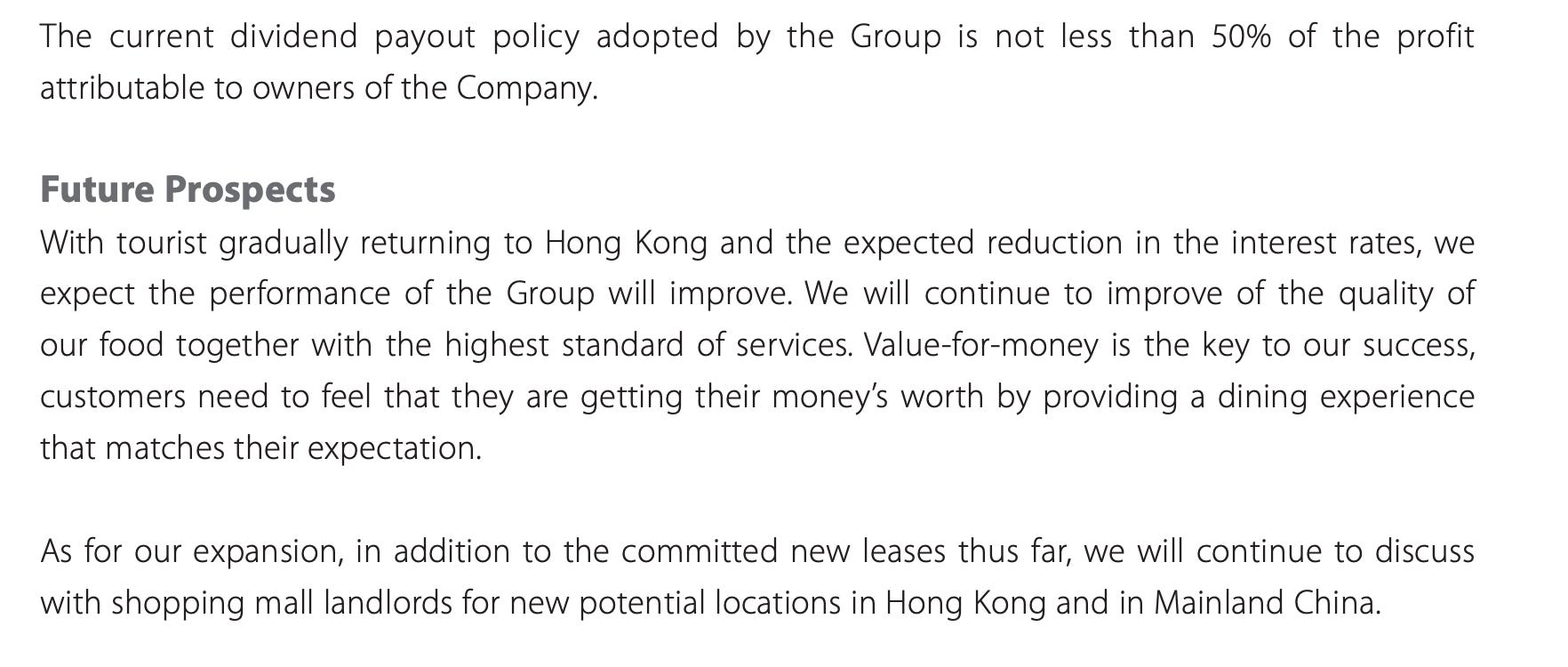

Committed to shareholder returns, the company maintained a generous dividend payout policy—rising from 30%+ to 50%+—even through the challenges of COVID.

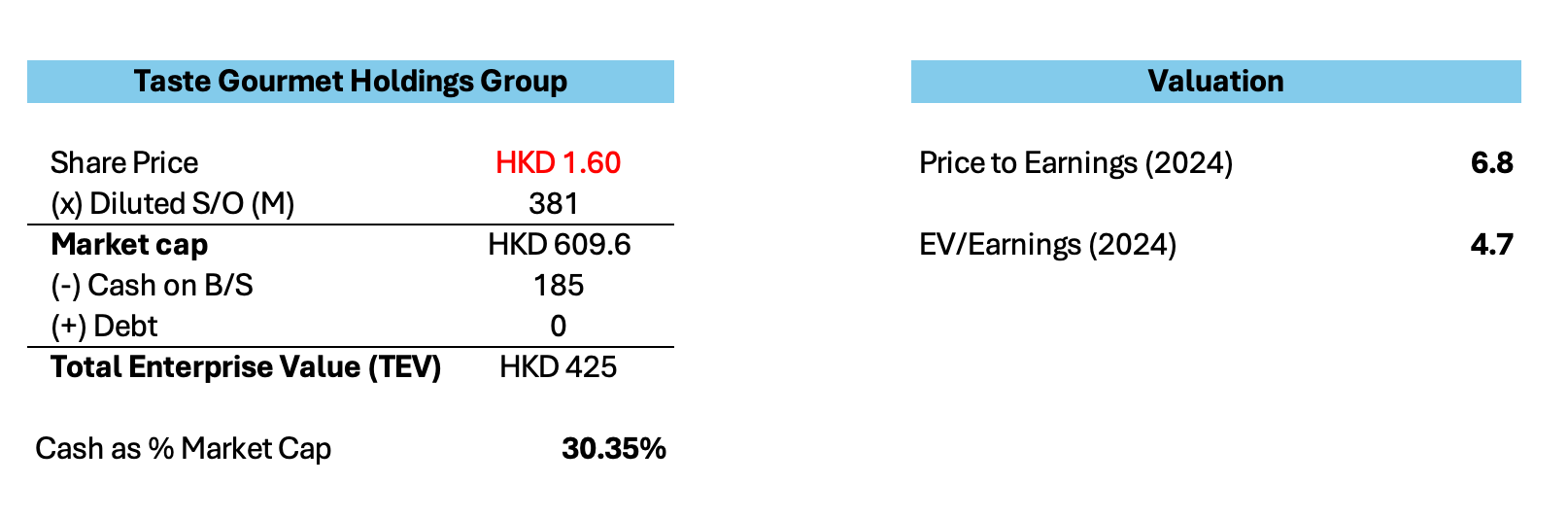

Despite significantly outpacing its peers in growth, it trades at a deep discount, with a P/E of just 6.8 and an EV/Earnings multiple of 4.7—far below industry averages.

Poised for an uplisting, yet currently undervalued due to its small market cap, making it overlooked by institutional funds.

In Chinese the phrase 出去玩儿 (chūqù wánr) literally translates to "go out and have fun," which (in China) often means going out to eat with friends.

What amazed me most when I lived there was the difference in dining experiences. In my home country, restaurants are often set in scenic locations, offering beautiful natural views. In China, the cities are too dense, restuarants are often bound to the street or in malls, so they create the scenery within—transforming indoor spaces into immersive, otherworldly environments that make dining an experience in itself.

If you've never been to China, chances are your perception of it is far from reality, and thats fine- go watch a few youtube videos. Having lived there, I often reminisce about my experiences, and when I look at the restaurants this company operates, my heart yearns to return to try them out. After living in China, I am a long-term China Bull. The people are extremely hardworking, the technology is insanely advanced, and to be completely honest with you- China is ahead of the West in many aspects.

So, without further ado, let me introduce you to this small-cap restaurant holding company. I'll break down their business model and explain why I believe they are positioned for success, and very undervalued.

Also, please do yourself a favor and like, restack and comment on this post, because it will help me write more and help you make more money.

1. Taste. Gourmet Group Ltd

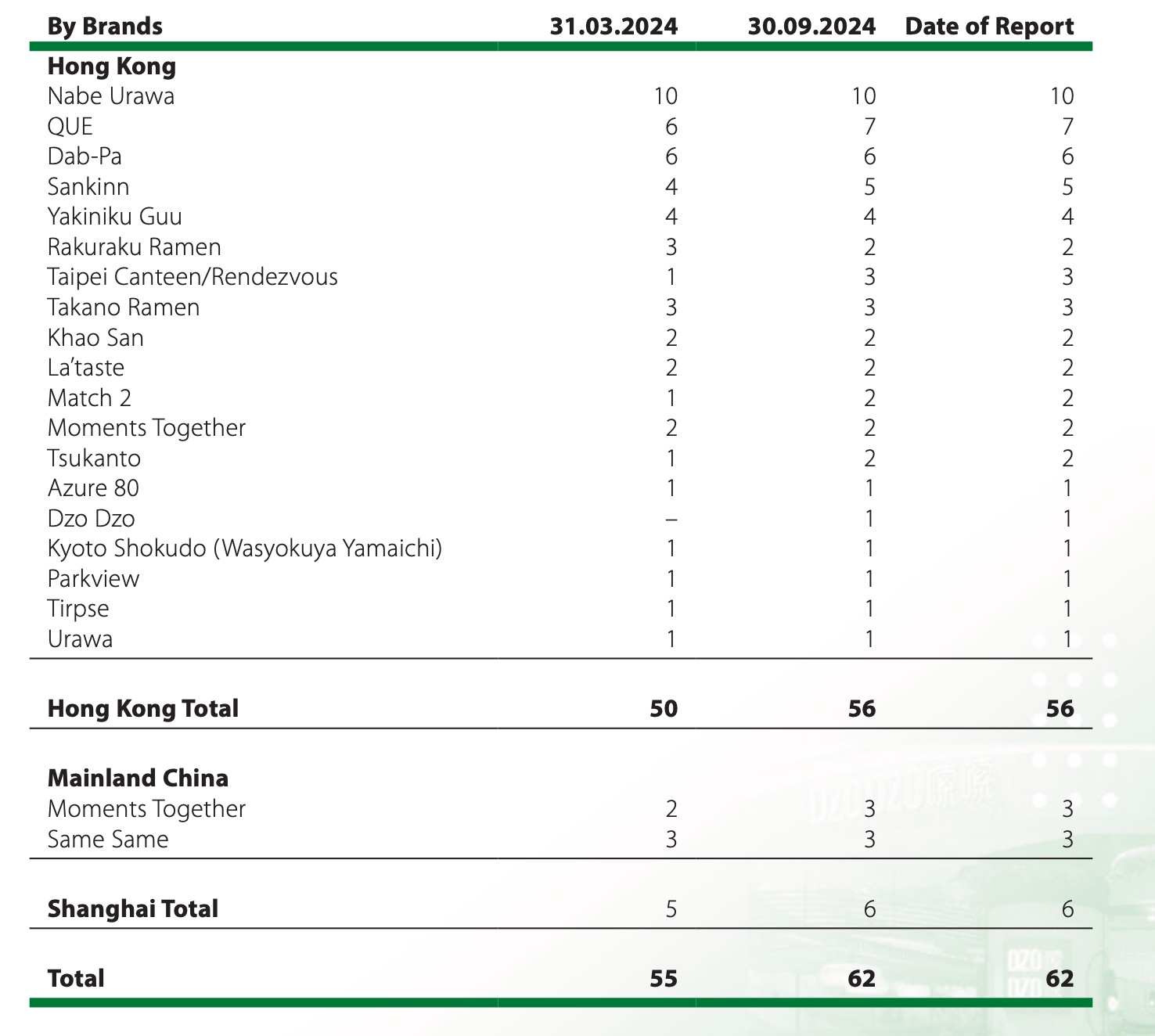

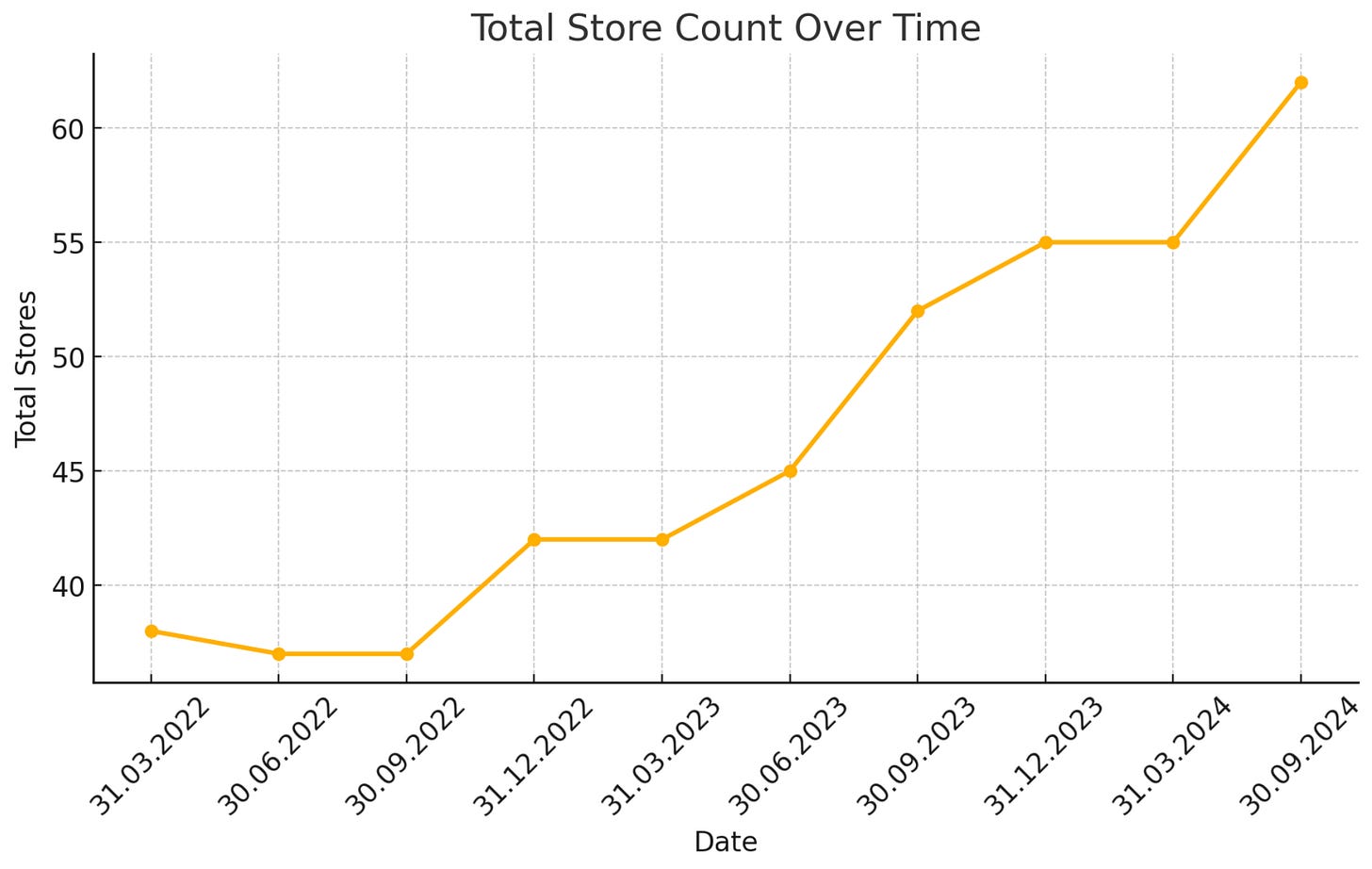

Taste Gourmet Group is founder led and owned and operates restaurants in Hong Kong and has recently expanded into mainland China, Shanghai.

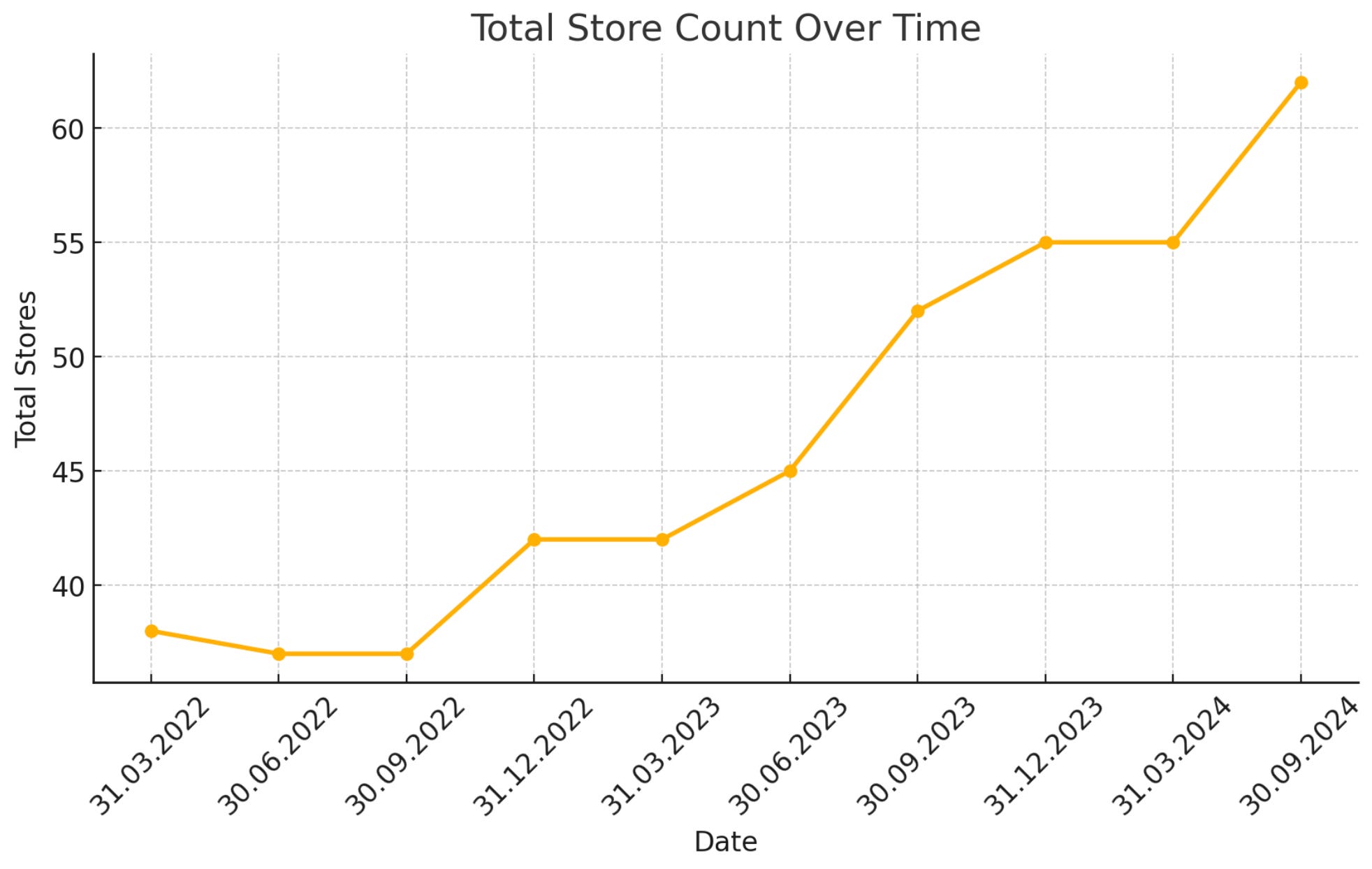

The group's restaurants serve Vietnamese, Japanese, Chinese and Western cuisine, targeting mid-to-high-end diners and the young. These restaurants are mostly located in first-tier shopping malls and on street levels in premium areas of Hong Kong Island, Kowloon and the New Territories. The new restaurants are in first-tier shopping malls rather than on the street level, since there is less competitive pressure in the malls where rent increases are gradual. The payoff period of its restaurants is 15 to 20 months, while most outlets will reach a balance in revenue and expenditure within a month.

Management follows a strategic business model centered around testing and scaling restaurant concepts. They acquire or develop a concept, trial it to assess performance, and if it outperforms their existing offerings, they roll it out aggressively.

A prime example of this is their restuarant concept QUE…

Previously, Dab-Pa held the second-largest store count, but once QUE proved successful, management quickly expanded its footprint until it surpassed Dab-Pa. Notably, QUE consistently outperforms Dab-Pa in Google ratings, likely due to its stronger appeal among younger generations.

Management also takes a pragmatic approach to underperforming locations. Rather than holding on to struggling stores, they shut them down, simply stating that “the returns didn’t justify the labor costs.” It’s a straightforward, results-driven business model—and so far, it’s working exceptionally well.

Management, I believe, are also better operators compared to their closest competitor (Jiumaojiu), but more on that later.

First, let’s take a glimpse into what these concepts look like.

16% Nabe Urawa

Nabe Urawa positions itself in the upper mid‑to‑high tier of Japanese dining and is a vibrant culinary destination that captures the heart of traditional Japanese hot pot dining while adding its own modern flair.

~4 star Google Reviews.

11% QUE

This one gets me excited.

In late 2022, Taste Gourmet Group opened its first QUE store. At the time, Dab-Pa had 6 locations. Fast forward to today, and the company now operates 7 QUE stores… Dab-Pa STILL has 6 locations—a clear testament to QUE’s resounding success and a peak into the company’s strategy of testing concepts, and expanding successful ones.

With an impressive 4.5-star rating on Google, QUE consistently earns above-average reviews, further solidifying its strong appeal and growth potential.

Yum!

I genuinely appreciate you taking the time to read this post. Please like, restack, and comment anything on this post, you'd be incentivising me to share more of these kinds of ideas with you.

New Concepts - SameSame (but different) in Shanghai

The company began its expansion into mainland China in March 2021 with Same Same and Moments Together—remarkably, during the country’s prolonged COVID lockdowns. Despite the challenging timing, they pushed forward, demonstrating confidence in their growth strategy.

One concept that particularly intrigues me is Same Same (but different). Achieving 4.5 stars on Dianping is an impressive feat—especially considering that Dianping is the go-to platform for Chinese consumers to rate virtually any physical establishment (since Google is banned in China).

Same Same stands out from the company’s other offerings. It leans slightly more upscale, with a refined aesthetic that sets it apart while still fitting within the brand’s overall premium positioning.

And here is a little snapshot of Moments Together, their other concept leading the charge into the mainland.

Restack this pretty please.

2. Financials/Valuation/Peers

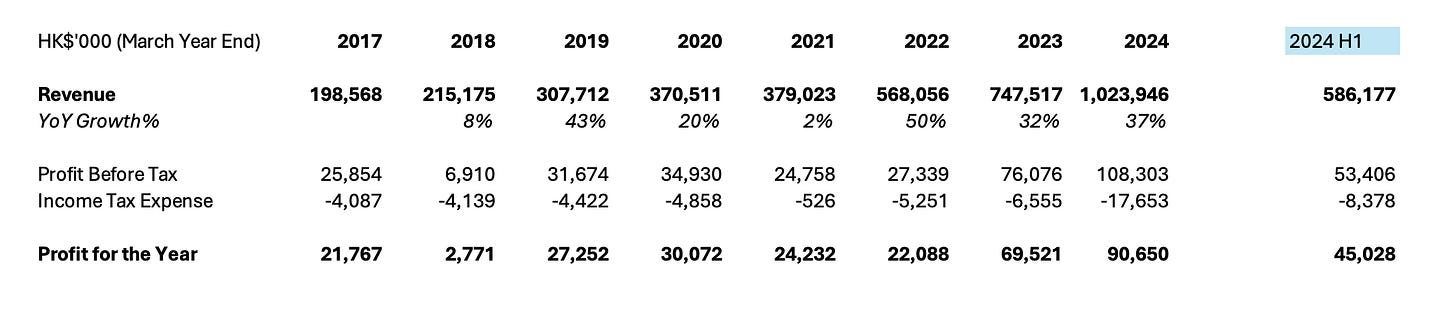

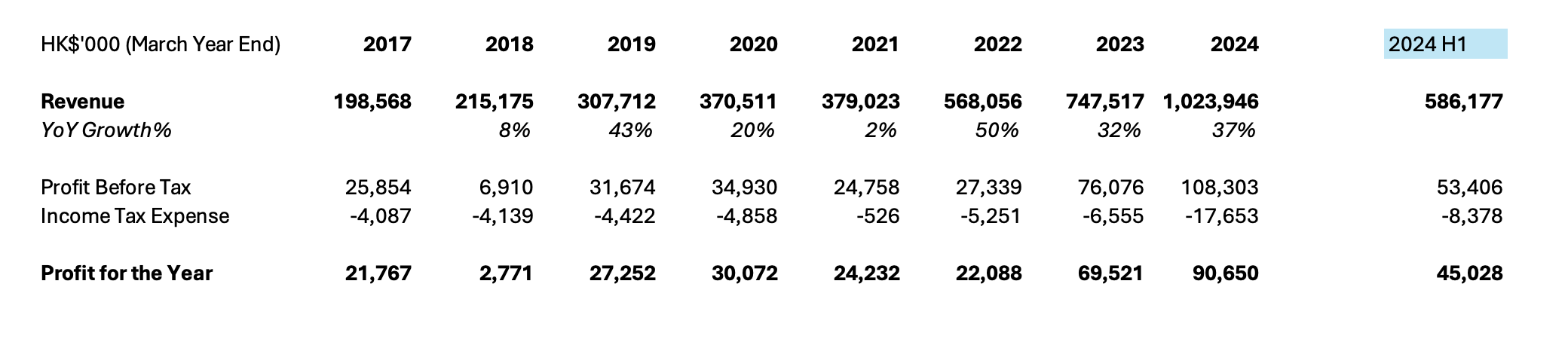

Above 30% annual revenue growth over the last 3 years.

50% dividend payout ratio.

Chinese government pushing stimulus to get consumption.

It’s not unlikely we continue to see +20% or +30% growth as they roll out new stores. That 8.5% dividend will mostly likely grow.

PLEASE TAKE THE TIME TO LIKE, RESTACK, AND COMMENT BECAUSE IT WOULD HELP ME WRITE MORE!

Valuation/Peers

They grew revenue at 37% YoY TTM

Dividend payout is 50%

Valuation is quite absurd given the growth + the clear shareholder payout.

I’m not going to overthink the valuation. I could go and put a fair value on it and say its worth a P/E of 12 or 15 given the growth, but I don’t need to - its obviously very undervalued.

Don’t h@te me for not adding lease liabilities here.

I treat lease payments as rent, which is why I compare earnings to EV excluding lease liabilities. In my view, adding lease liabilities to the equation doesn't necessarily provide a clearer valuation picture.

Why? Because lease payments are an operational cost, not a debt that an acquirer could simply "pay off"—it’s rent. The key takeaway is that as the company expands, new stores that don’t perform well will temporarily compress margins, but that’s an expected part of the growth process.

As long as you recognize this dynamic, there’s nothing more to it.

Peers

Compared to peers, Taste Gourmet Group is the obvious outlier from a valuation perspective. I believe this is because it’s small and relatively underdiscovered compared to the rest.

Market Penetration & Positioning: A key element of Taste Gourmet’s strategy is its multi-brand portfolio, which differentiates it from single-brand rivals. By operating concepts in different cuisine categories (Japanese, Vietnamese, Northern Chinese, Taiwanese, Western, etc.), Taste Group can tap multiple customer segments and dining occasions. This echoes some tactics of larger Chinese groups (Jiumaojiu also runs several cuisine brands under one corporate roof but is overly concentrated in Tai Er, Saukrat fish which has faced volatility with changing consumer preferences), but within Hong Kong it’s a unique proposition – many local chains stick to one specialty. The group also leverages digital engagement to penetrate the market; for example, it launched its own mobile app for promotions and loyalty, which quickly rose into the top 10 food & drink apps in Hong Kong.

Jiumaojiu

Jiumaojiu is Taste Gourmet’s closest competitor, following a similar strategy of introducing new restaurant concepts. However, they overexpanded during COVID-19, leading to the closure of many locations. Additionally, they are heavily reliant on their flagship brand, Tai Er, which specializes in sauerkraut fish—a dish facing intense competition from other restaurants.

Jiumaojiu also operates in a lower price range compared to Taste Gourmet. The average per-person spend at Taste Gourmet is around 150 HKD, whereas Jiumaojiu competes at a more affordable 66 HKD. This positions Taste Gourmet in a slightly different market, appealing to wealthier consumers seeking a premium dining experience without the exorbitant costs of high-end fine dining. I believe these wealthier customers are slightly less price sensitive compared to Jiumaojiu’s average consumer.

PLEASE TAKE THE TIME TO LIKE, RESTACK, AND COMMENT BECAUSE IT WOULD HELP ME WRITE MORE!

China consumer stimulus tailwind

The CCP has been adament to try and balance their economy and move it towards a more consumption driven model. The recent policy changes prove this. While these policies and stimulus packages have fallen short in the past to get the Chinese people anywhere close to consuming like their western friends I believe its a nice tailwind that the thesis does not rely on, but that could help boost consumption too.

Chinese stocks are currently trading at exceptionally low valuations. Having lived in China for several years, I've witnessed firsthand the nation's remarkable capacity for innovation and growth.

My time in China has instilled a deep confidence in its people and economy. While the political landscape remains volatile, there appears to be a recognition of past missteps, such as the 2021 crackdown on the private education sector that led to significant job losses. Since then, many of these restrictive policies have been rolled back, reflecting an understanding of the importance of supporting private enterprise to sustain economic growth.

Risks

Management:

The company is founder-led and majority founder-owned (75%), though this could change with the planned uplisting. While there was an incident involving an employee injury and delays in enrolling some employees in the Mandatory Provident Fund (MPF) retirement scheme, these issues have been fully resolved. This stands in stark contrast to the challenges faced by Jiumaojiu, which has dealt with serious brand-damaging incidents, including the discovery of a banned antibiotic in its fish, consumer backlash over shrinkflation in meal sizes, and reports of detergent residue on chopsticks.

Industry-Wide Risks

Cost inflation and economic downturns are less of a concern for a company that managed to survive—and even slightly grow revenue—through some of the worst black swan events a restaurant group could face.

Agree on your treatment of lease liabilities. It's a stupid idea to treat this as debt. As long as you use net income or EBITDA making sure that it's adjusted for rent if accounted as interest + depreciation, all good.

Why do you think its mispriced by the market?

I don't like the 75% largest shareholder.

Also their dividend policy is strange if they could reinvest funds in opening new stores, why pay out?

Reading for tonight! Here from twitter