Gambling isn’t an addiction, its a disease.

Problem gambling prevalence rate was 4%; the rate among online gamblers was five times higher at 21.9%; more than 20% of online gamblers were at-risk gamblers (vs. less than 10% of non-online gamblers). Online gamblers were twice as likely to experience gambling problems compared to non-online gamblers. - research paper on gambling

This is why its better to own an iGaming stock compared to a physical casino.

Thesis:

This scenario mirrors the opportunity presented by Super Group (SGHC) which delivered a swift 60% gain in just two months. Similarly, Betsson AB, an online casino operator based in Sweden, offers a compelling value proposition. Operating across Central & Eastern Europe, Central Asia, Latin America (LatAm), and Western Europe, Betsson has consistently grown revenue and profits through both organic growth and strategic acquisitions.

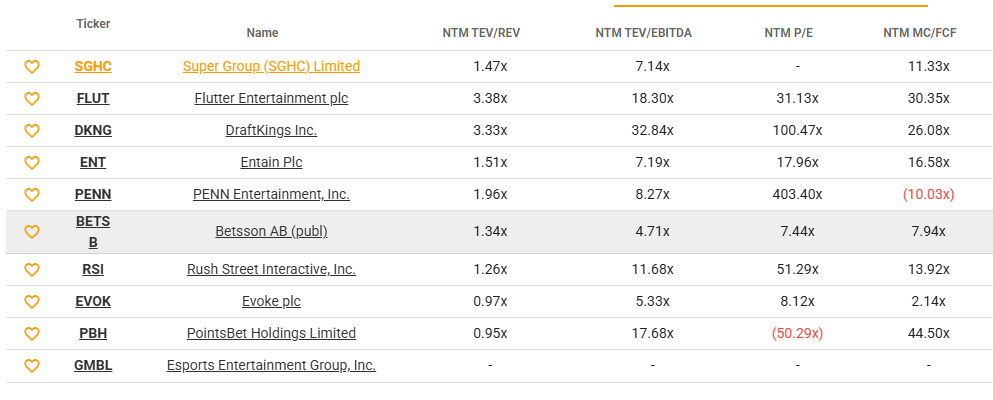

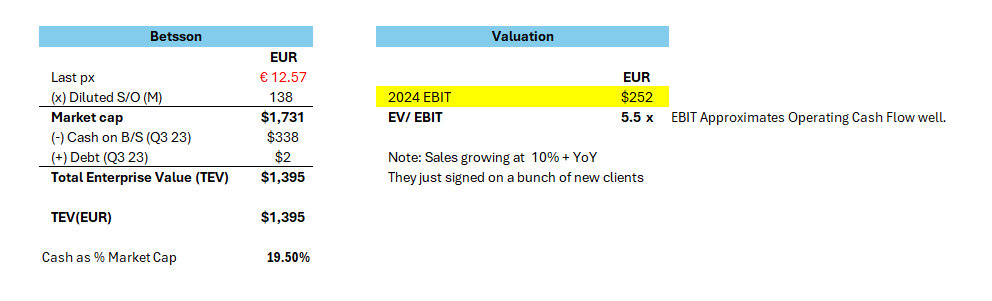

Currently, the company trades at a historically low EV/EBITDA multiple of 4.71x—significantly below peers. This valuation is too low for a company of Betsson’s scale and efficiency. (Below images TEV/EBITDA is calculated incorrectly).

When I invested in Super Group, a business with lower margins (due to exiting the U.S. market), it was trading at just over 5x EV/EBITDA. Despite a slight pullback in Super Group’s share price, its performance highlights the potential upside for Betsson AB, which operates in a similar market segment but with superior margins and strategic positioning.

Information Supporting Thesis:

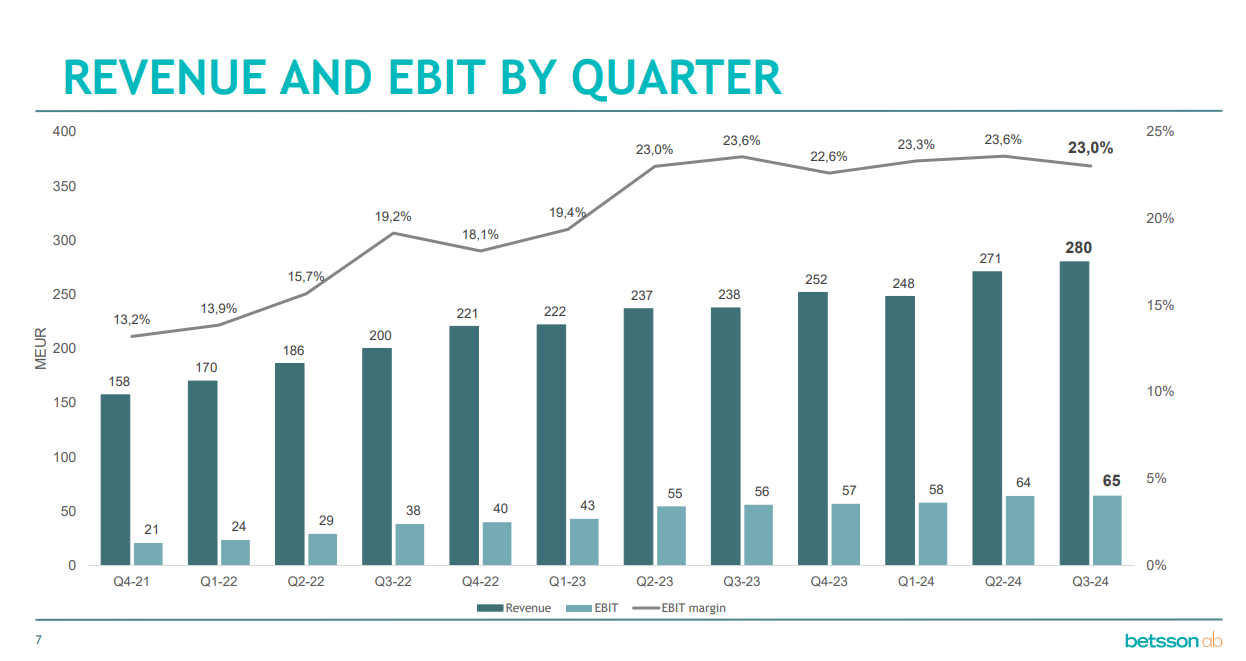

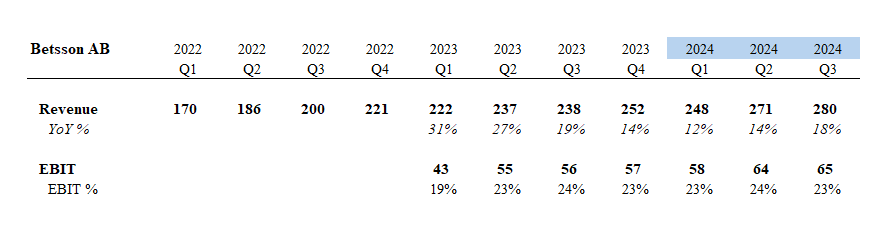

Betsson AB has grown revenue very steadily and they have managed to increase their EBIT margin to 23% which is close to industry peers.

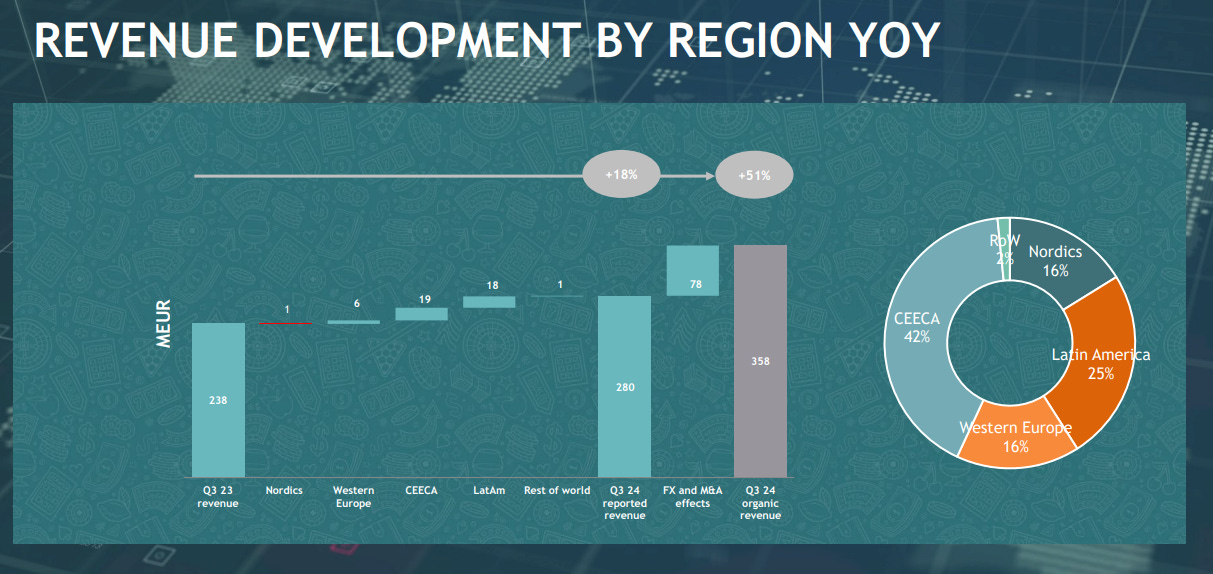

Latam and CEECA (Central & Eastern Europe and Central Asia) remain their top exposures for now. Latam presents a risk in 2025 because Brazil is introducing new regulations for the iGaming industry. Betsson AB has applied for their license.

After a few acquisitions the company has moved to a net-cash position. I expect the company to return the cash via dividends, or buybacks. It is in their strategy to make acquisitions, which have worked well in the past, so we may see more of that which is a good thing.

Strategy for future growth:

Techsson (lol at the name) is Betsson Group's proprietary Player Account Management System (PAM) platform, serving as the backbone for its online gaming operations. This in-house developed platform manages critical functions such as payments, customer information, account management, and game integration, ensuring a seamless and secure user experience across Betsson's various brands.

By owning and operating Techsson, Betsson maintains full control over its technological infrastructure, allowing for rapid adaptations to market changes, enhanced scalability, and the ability to offer tailored solutions to both B2C and B2B clients. This strategic ownership supports Betsson's long-term growth objectives and reinforces its position as a leading operator in the online gaming industry.

Offering Techsson out B2B and B2C allows Betsson to get an inside look at a potential acquisition target. It can generate a pipeline. I think they plan to leverage this strategy going forward with their acquisition of Sporting Solutions in partnership with FDJ. I am almost certain that Sporting Solutions will enable them another inside look at potential acquisition targets.

With 24% of the companies revenue generated from ‘system delivery’ I have some conviction that these managers are smart and have a good sight on future acquisitions.

Price. Management. Company.

Price:

This is not a difficult company to value. They generate a steady stream of income from their *ahem* problemed gamblers. At 4.7X EV/EBITDA, its cheap. Especially given its growth.

Note- below is EBIT, not EBITDA.

I would actually like to see them lever up and make an acquisition. If they lever up and do an acquisition at the right price, we could get a significant growth to earnings.

Management:

The CEO has extensive extensive experience in the industry and founded Net Entertainment (online casino) so he knows the business.

Taking a look at their strategy makes me think they are really good strategic thinkers with a long-term view.

He also holds quite a few shares of the company. (1.8m split between A and B). The A shares have 10 votes compared to B which has 1 vote each.

Good Company/Competitive Advantage

If you read the Super Group writeup I wrote recently, you would note that they were doing an acquisition of the technical platform that a third party build for them. They were bringing it in-house.

Betsson already owns their technical platform and sportsbook. They mention its a part of their strategy, I think it allows them more access to acquisitions because they can see how those companies are doing using the data from the platform.

Target & Weight:

5%, same as SGHC. Hopefully we get another 60% gain lol.

Monitor:

Key Risks Identified in Betsson's Regulatory Update

The regulatory environment presents various risks for Betsson, which can significantly impact its common stock.

1. Nordic Market Risks

Finland: Pending changes to the Gambling Act may affect market operations and regulatory compliance requirements.

Norway: Introduction of DNS blocking for unlicensed operators poses a direct risk to Betsson's access to this market if deemed non-compliant.

Importance: Nordic markets are key to Betsson's revenue. Restrictive actions like DNS blocking in Norway could directly limit market access and revenue generation.

2. Western Europe

Italy: Uncertainty around the licensing process and potential delays in renewing licenses could impact operational continuity and market share.

Importance: Italy is a significant market for Betsson, and any disruptions in licensing can affect revenue streams and market presence.

3. CEECA Risks

Croatia: Proposed restrictions on gambling advertising and stricter responsible gambling measures may increase operational costs and reduce player acquisition opportunities.

Importance: Limits on advertising and compliance costs can negatively affect profitability and brand visibility in the region.

4. Latin America

Brazil: Regulatory changes requiring local licenses could necessitate additional compliance costs and operational restructuring. Any delay in securing a license may temporarily hinder market operations.

Peru: The introduction of a consumption tax and legal challenges regarding its implementation could affect profitability. Legal uncertainties may also delay strategic decisions.

Colombia: Increased withholding tax rates and VAT on gaming operations will elevate costs. Advertising restrictions could further impact customer acquisition.

Importance: Latin America is a growing market for Betsson. Regulatory challenges and increased taxes can reduce profitability and complicate expansion.

This is what the modern day Tommy Shelby looks like:

Have been holding this stock for a long time. A gambling friend talked about it over 5 years ago. Two downsides:

1 my initial position was too small

2 my wife doesn't like the gambling position