This stock will most likely re-rate, upside ~100%+

P/E = 3 for a High Margin, Capital Light, Cash Generator

Oh boy, Archetype Capital is at it again buying from the pessimists!

QFIN 0.00%↑ or $3660.HK

Here is my TL;DR thesis:

The China Fintech lending sector has currently been oversold. The best of the bunch (undervalued + great business model) is QFIN. The market is waaay too pessimistic, and the business fundamentals are fine. I expect this to re-rate 100%+.

I believe the sector-wide sell-off in Chinese fintech was caused by consumer-finance reforms, and investors being skittish on China in general. Yes- I have watched the China-Hustle. I am well aware of the reverse-merger scams that were run. I do not believe QFIN is a scam, but I do believe that many investors believe China to be completely ‘un-investable’ and I thank them, because its for that reason we can make money, reliably, investing in China.

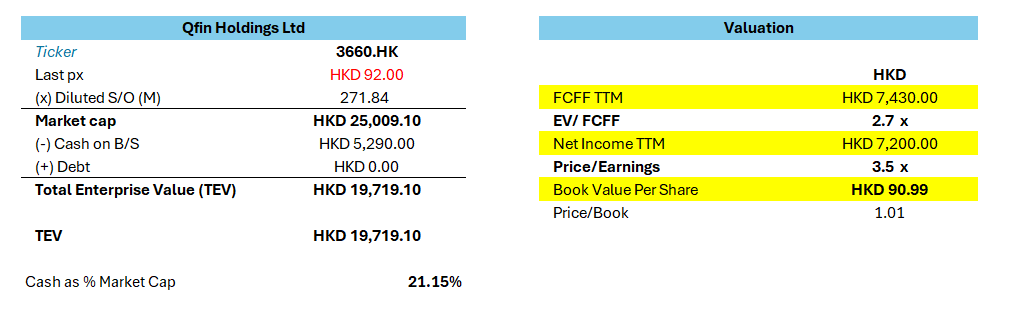

Cheap & High Margin, capital light, Cash generator: EV/EBIT ≈ 2–3× and ~3-4× P/E. Net cash and active cash returns (dividend + buybacks).

Upside: On mid-cycle EV/EBIT 5–6× (still conservative), equity is ~2–3× from here without needing growth to accelerate, just prove underwriting and keep ≥50% capital-light mix.

Why it’s mispriced: sentiment shock after cautious Q3 guide, data-policy headlines, slight QoQ dip in capital-light share, and convert-arb overhang. None of those break the cash engine.

What the risks are: PRC policy/VIE/HFCAA framework, mix drift back to credit-heavy, related-party ecosystem (360), credit cycle, and partner concentration.

An opportunity for my subscribers

There are only 2 spots left to subscribe to an annual pledge at the bargain price $239/year. That’s $19/month, basically the price of a burger.

After that, the price goes up. No exceptions.

These 10 pledges will lock in the one of lowest prices this research will ever be offered at.

Pledge now. Don’t blink, or someone else will take your slot.

What does QFIN do?

A credit-tech platform. They connect financial institutions with consumers who need credit. One of their business segments provides the credit but they also generate revenue from service fees. QFIN provides the plumbing, scoring, and servicing and earns fees.

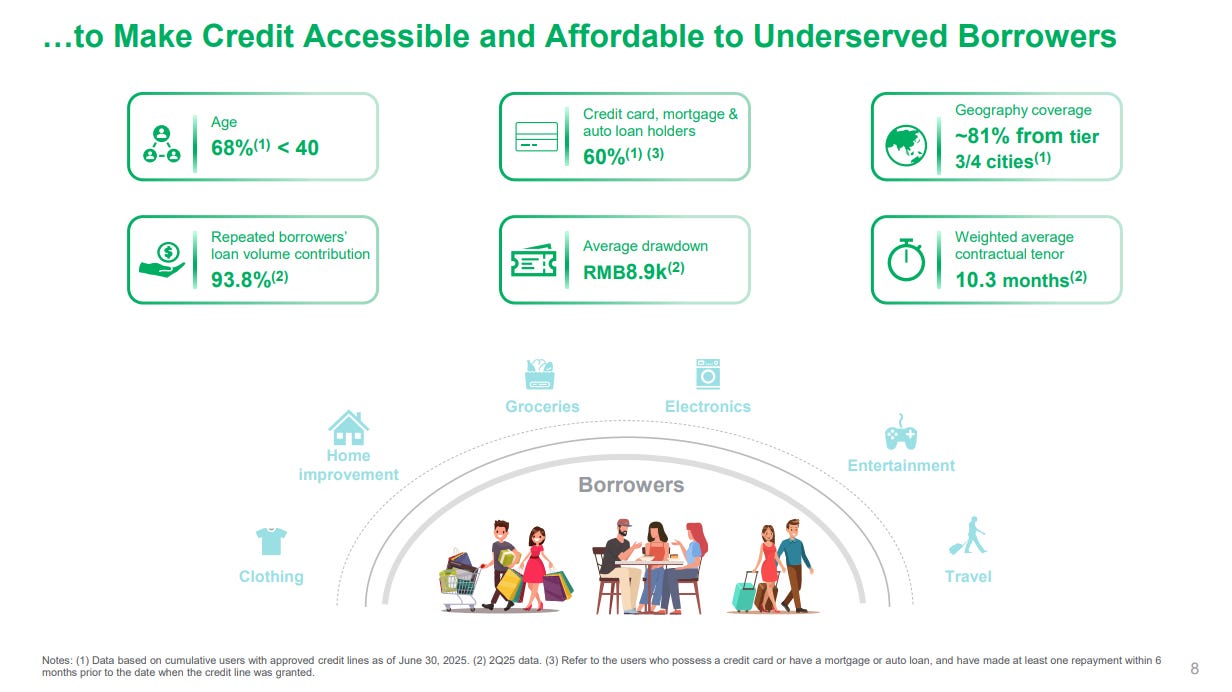

The loans are small, on average ~9000RMB or $1,200. To individuals and small to medium enterprises (SMEs). Exact portion is not disclosed.

They have two main segments:

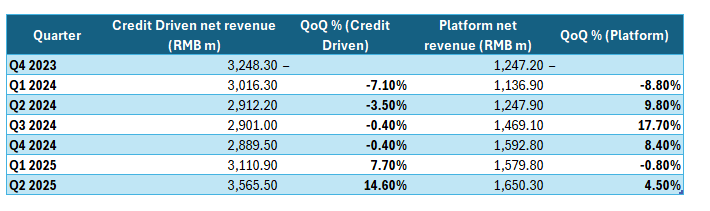

1- Credit-Driven Services: On balance sheet lending

2- Platform & Referral Services: Off balance sheet loan facilitation

1- Credit-Driven Services: On balance sheet lending

Not much to explain here- they loan to their own customers (small loans)

2- Platform & Referral Services: Off balance sheet loan facilitation

(capital light): Acquires borrowers through its app. Scores them using AI and credit data. Matches them with partner banks (who provide the funding). QFin charges the banks (or lenders) service fees.

This segment is high margin.

My thesis doesn’t rely on the company growing revenue. It relies on stabilization (which we see fundamentally in the numbers already), and a nice growing mix towards more Platform (higher margin, more SaaS-like).

Price to earnings graph for QFIN now at ~3.

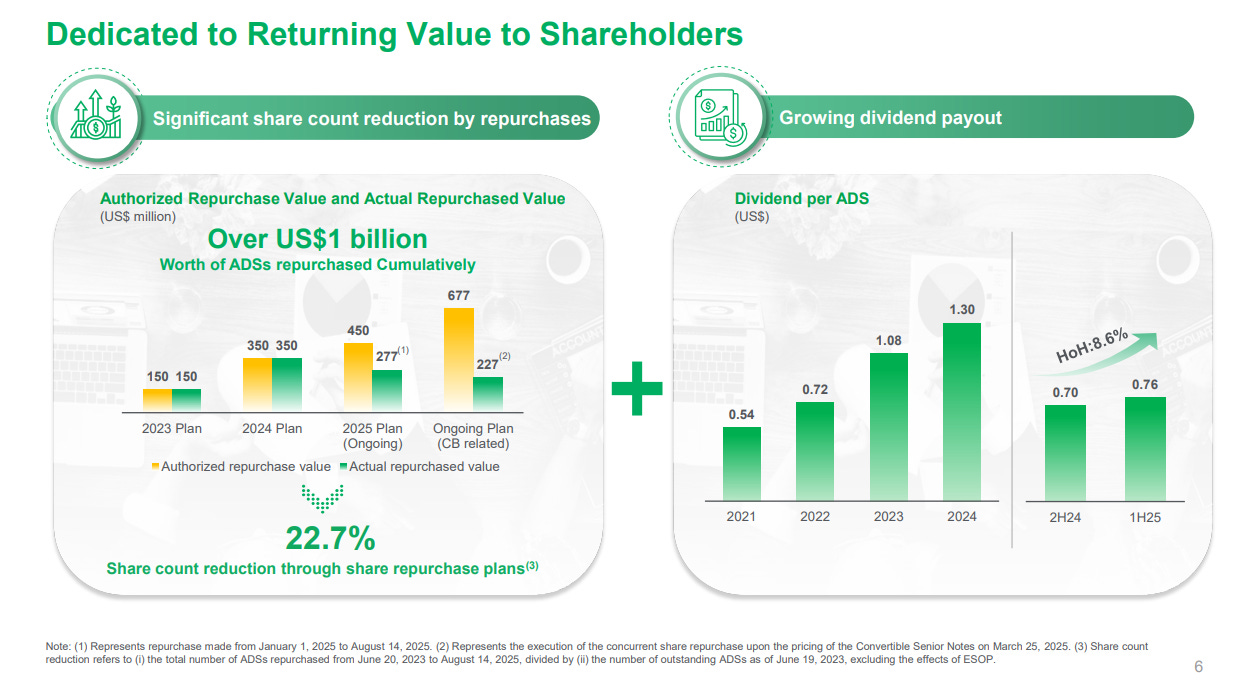

Dividends and Buybacks

The dividend yield sits at ~6% but I think the real value will come from a re-rate back to a P/E of ~6 or ~10.

Buybacks, though, could force a re-rate faster, or at least force share upwards even if the multiple stays the same.

Normally when you find a company like this its a value trap because management don’t pay shareholders. Here, they are paying shareholders.

This is a risk I want to take. I’m betting against you, Mr. Market. They have capacity to repurchase up to mid-teens percent of the float at current prices, which would be disgustingly accretive.

Risks

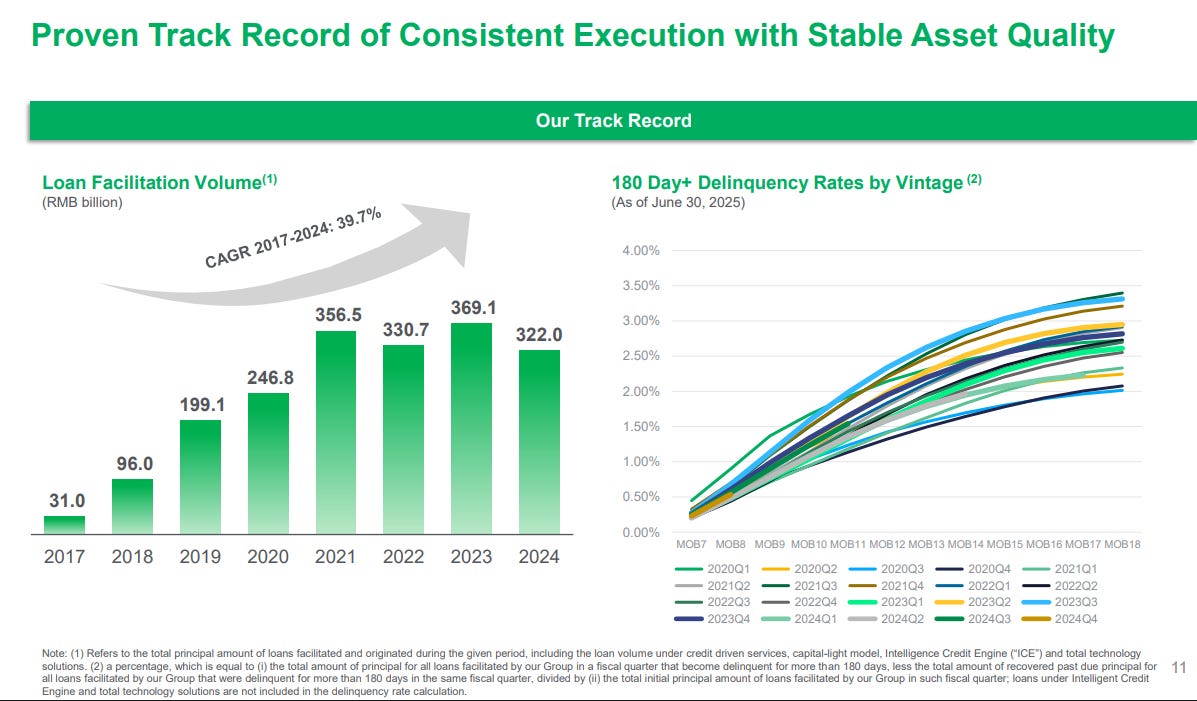

The main risks I see here are some policy-driven factors. Regulators could tighten the noose- historically we have seen this. China has a problem with shadow lenders, which Beijing has been reforming.

ADR wrapper / US-listing risk can be avoided by buying directly on the HKEX. The VIE and PRC policy risks are the same either way; I think the market is overpricing them.

Grizzly had a short-report out on this stock. I went through it, I think they're wrong because Grizzly claims profits are fake, but at the same time the company is able to do massive buybacks and dividends...Still, do your own due diligence.

You should check out Nasdaq: JFIN.