This is the cheapest energy-sector stock I’ve (ever) found. And I think the price is over-exaggerating the risks, drastically.

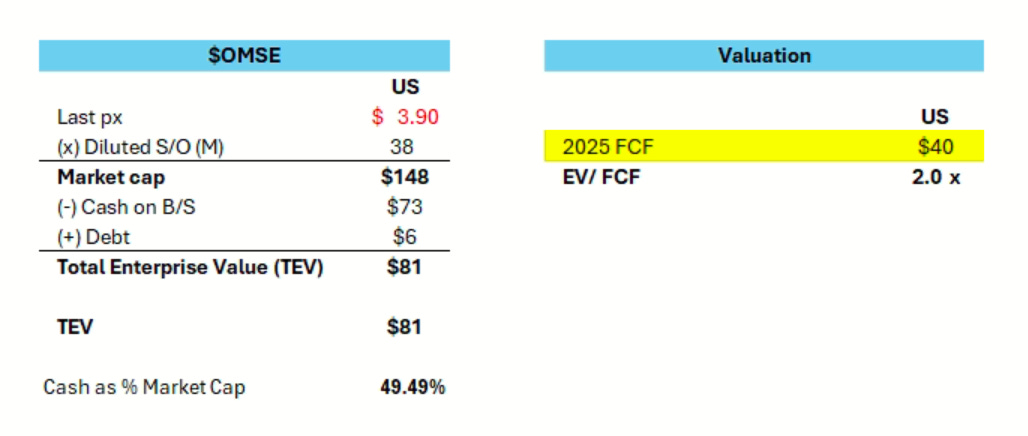

Cheap: EV/EBIT ≈ 1–2× (EV ≈ $75m vs. FY25 EBIT ≈ $60m) and ~3× P/E; cash-rich, no debt.

Real Cash Flow: FY25 revenue ≈ $204m, ~29% EBIT margin, solid operating cash flow.

Upside: On mid-cycle EBIT $40–45m, a modest 5–6× EV/EBIT implies a 2–3× equity upside from here.

Why it’s mispriced: small float/low liquidity + governance overhang + fear that FY25 was a one-customer spike.

What the risks are: backlog and contract quality, customer concentration.

An opportunity for my subscribers

There are only 6 spots left to subscribe to an annual pledge at the bargain price $229/year. That’s $18/month, basically the price of a burger.

After that, the price goes up. No exceptions.

These 10 pledges will lock in the one of lowest prices this research will ever be offered at.

Pledge now. Don’t blink, or someone else will take your slot.

What does OMSE do?

OMS Energy Technologies makes the metal “plumbing” for oil and gas wells.

Their core products are high-strength connectors and pipes that screw together to prevent leaks.

They also build the surface wellhead assemblies whcih are the valves and controls at the top of a well, and do premium threading and related services.

They don’t produce oil themselves, they sell equipment and services mainly to operators in Asia and the Middle East.

Saudi Aramco is and was their biggest customer for financial year end 2025, contributing 67% of their total revenue. At the current valuation, and given where the oil price is, I am more than happy to invest. Investing in the Oil & Gas industry is as simple as buying low and selling high, don’t overcomplicate it. And right now, its low.

I am not overly concerned about the concentration risk. They have a 10-year supply agreement with Saudi Aramco that they signed in 2024. See an excerpt from the news release below.

The $120-$200 million is management guidance, nothing contractual.

Where I think the market is wrong

I think this stock sold off along with the oil market. It’s a recent IPO, its tiny, not many people are on this- yet.

I have made money in the oil market before, and I don’t overcomplicate it. I buy a small-cap that's undervalued when oil is low and its a strategy that hasn’t failed me. Well- we are at that point again.

The IPO

The company IPO’d at $9. So shares have dropped in half since then. The proceeds are for “R&D, marketing & sales, compliance/governance, working capital” - so essentially just growth money raised to support execution and their Aramco contract.

The big risks

Aramco doesn’t order as much stuff as the company guided.

The majority holder (founder) isn’t friendly to minority shareholders. (wait and see). Founder is locked up for 180 days from the final prospectus (so lock-up expiry is around early Nov 2025). Watch for post-lock-up selling plans or 10b5-1 programs.

Ok. I'll comment. DAMN TOO LATE!

This thing never trades down to your entry price 😅