These underfollowed Substacks will make you rich

With their undervalued quality ideas

Scouring stocks A-Z is a full-time job, and you only very rarely come across a company where you’re like ‘holy shit this is undervalued’. There are also countless investing Substacks out there now, and I have seen that many of them have realized (to our detriment) that posting quantity over quality is a way to win follows thanks to Substacks algorithm. They earn followers, but dilute our feeds. Then you have some undercover fund managers lurking on the platform, with one or two great ideas. They don’t need to post weekly, or monthly because that’s not their job.

In my own attempt to add value to you, my followers, I would like to share with you 2 extremely underfollowed Substacks (and their free-to-access pitches- which I have personally invested in). No- they did not ask me to do this. I am sharing because the quality of their write-ups, and the pitches themselves are very enticing.

I add value to the pitch where I can, like for instance, with Wasion Holdings. Where I cannot (because they have done such a good job) I recommend you just read them yourselves and give them a follow. I’m quite certain they will make you money, as they have me :)

Wasion Holdings Ltd (HKG: 3393)

First up, we have Wasion Holdings, which I found on this super underfollowed Substack

Wasion Holdings supplies electrical measurement, MV/LV switchgear, transformers, and is qualifying liquid-cooling/HVDC solutions for DayOne’s overseas builds. It screens cheap at ~13× EV/EBIT despite rapid growth and a visible backlog. It also owns ~60% of Willfar Information; on a look-through basis, that stake is worth roughly Wasion Holding’s entire market cap, however it doesn’t seem like that value will be ‘realized’ anytime soon- its still part of what you own when you own Wasion.

At EV/EBIT you might say ‘that’s not that undervalued’, but for how fast the company is growing, as well as the transparency into its future growth, I believe it is significantly undervalued and so I have taken a position.

Given that China is around a year behind the U.S. in its datacenter buildout, there exists a fat-right tail (the potential for earnings to really skyrocket) outside 1 to 2 years. I can ramble on about this, but that would defeat the point -

Read the pitch first, then come back here because I add a small part about the risks I think are prevalent to understand, and how to think about them.

The risks to Wasion Holdings

DayOne is building out datacenters using the most advanced AI NVIDIA chips that China cannot get their hands on locally. So the loophole, which is well known to the U.S. regulators now call the “cloud/compute loophole”, is just to rent the capacity abroad- like in Malaysia where DayOne is building for Oracle and Bytedance.

So the U.S. just shuts them down? Not really. Biden Admin tried and then the Trump Admin rescinded the order because it was too diplomatically messy.

Policy timeline:

Jan 15, 2025: U.S. “AI Diffusion Rule” published (controls on advanced computing and model weights). Sidley

May–Jun 2025: Growing scrutiny of Chinese AI training in Malaysia; probes launched. Reuters

Mid-2025: Rescission of AI Diffusion Rule announced by BIS (signals policy volatility). Bureau of Industry and Security

Aug–Sep 2025: Malaysia tightens chip-movement rules and reins in DC growth. Wall Street Journal

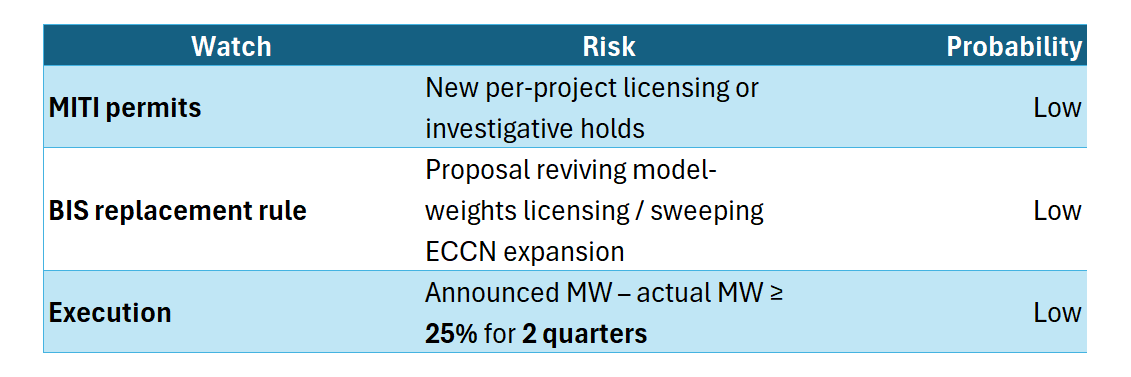

Risk Map

So these are the top 3 ‘things to watch’. I feel like BIS replacement rule would be the most damaging, but demand would still re-route.

(MITI) Malaysia’s Ministry of Investment, Trade & Industry put a permit/notification gate on the export, transshipment, and transit of “Advanced AI chips.” This is largely to show they are in alignment with U.S. regulations. We can monitor releases to see if regulations become more stringent (I doubt this because it will harm their economic growth, this seems more likely done to appease U.S. regulators).

The U.S. rescinded its broad AI Diffusion Rule in May 2025 (signalling away from blanket model-weights controls), while Malaysia tightened chip-movement and DC oversight in July–Sept 2025, so the constraint moved to host-country permits rather than a new U.S. blanket rule.

What we need to watch for: new BIS rulemakings or guidance, Malaysia MITI permits and enforcement, and slippage between announced MW vs energized MW on DayOne projects.

Thakral Corporation & Chongqing Machinery & Electric Co ltd

Maius Partners

Maius Partners has exceptionally high quality ideas on their Substack, with a great record of performance too.

Two ideas I currently like a lot are Thakral Corporation which I think is still very undervalued, with all the necessary catalysts in place.

And Chongqing Machinery & Electric Co Ltd (HKG: 2722)

I am very excited to see what they put out next. I don’t have much to add to their theses. They have done an excellent job of explaining the opportunities, the catalysts, as well as the risks.

I second this. I am doing some work on these names as we speak - talking to them on the ground in Singapore. CQME has a rep at a trade show here who has been very helpful.