I am going to try and keep this as jargon-light as possible. If you are a generalist like me, which I expect you are, you need to know what you don’t know and where you are making a concession trying to understand these companies. Especially if you intend to go long.

Here we try to understand:

Sive Semiconductors

Applied Optoelectronics

Soitec- I am long

We can try our best to wrap our heads around the valuations.

Sivers Semiconductors AB

The most hyped of the bunch.

They are basically fabless. They make lasers.

These lasers are individual parts that are used to make up a photonics ‘module’. The lasers are just one part of the module. And everyone wants to use Siver’s lasers in their own product.

Their photonics lasers:

InP DFB lasers

laser-array specialist for SiPh, optical I/O, CPO,

lasers for pluggables

Closest peers are Coherent and Lumentum who offer a much broaded range of optics. Coherent and Lumetum make the lasers AND the modules.

Sivers photonics are very focused on the three mentioned above.

Sivers is similar to NVIDIA in that they hold the IP and get TSMC to make the chips.

Lets briefly try and undestand what all these partnerships mean for Siver’s Semiconductors.

-Ayar Labs partnership to use Siver’s lasers in their own products.

-Win Semiconductors, basically the TSMC for Siver’s, add real capacity to scale of production (of the lasers).

-O-Net is there to use Sive lasers and make modules (External Laser Small Form Factor (ELSFP) optical modules.)

-Poet Technologies also using Siver’s lasers to make a full module product (eg Pluggable transceivers)

-Enablence also using the lasers to make a full product.

How you should think of all these partnerships is that Siver’s lasers work well and now they are partnering with companies so they can make a full product using their lasers.

They are essentially preparing themselves for the launch of light. This is what the market is pricing in.

They are busy sampling their product, qualifying their product for manufacturing. The revenue has not arrived yet, but it will.

The quantity? That’s hard to tell.

“CW is like a lightbulb…It just shines a constant light. It is easier to make and is available from multiple sources and it’s inexpensive,” Nguyen said. “All of the high speed magic for modulating data happens in the silicon photonics.”

Valuation

You cannot value this company looking in the rear view mirror.

The best thing we can do is provide a wide band of what it should obviously not be worth- too expensive, or too cheap.

Price to sales and EV/EBITDA do not tell you anything now.

ALL the company’s real revenue will start next year, in 2027.

The market is trying to figure out what quantity that could be.

So what could it be?

Currently market cap sits at ~$400m (USD) EDIT*- now changed to $270m within like a day of me writing. yikes.

So how do you value it?

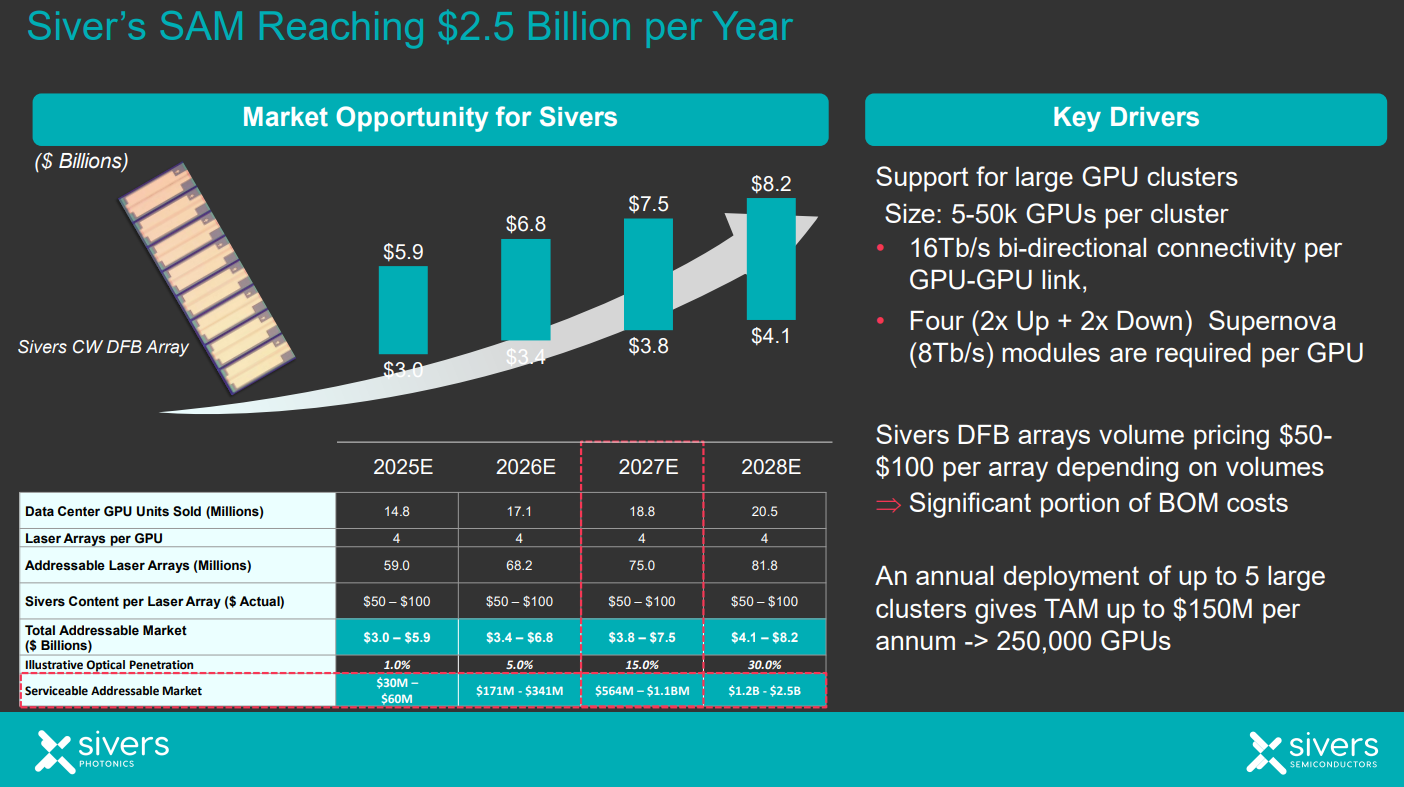

You need to try your best to quantify the 2027-2030 and beyond revenue opportunity. Siver’s gives us their DFB array TAM below.

2027E - $564M to $1.1Bn

2028E - $1.2B - $2.5Bn

BUT then they tampered these expectations down- $2bn in 2028?

If they don’t know their TAM, how are we supposed to?

Below is from their capital markets day presentations:

But its the oldest, November 19, 2023. We have an anchor of $10bn for Sivers as whole (not just lasers).

Lets try make some sense of this

The market currently is trying to price in their photonics opportunity.

If we use their LATEST Tam projection of $2bn + in 2028. And they get, like, 10% of that?

$200m revenue.

Latest results- Q4 2025, they did $8.4m. Annualized for 2026, lets say ~40M revenue. This is before they ramp up right?

That’s not bad, then you have a company trading at 2028 P/S of 1.

It’s okay.

The company right now, with all this information is not worth $1Bn today.

$500m is expensive and pure speculation.

$200m is ‘meh’ given the information is so sparse, the TAM got LOWER according to management.

$100m is where I would start looking to get in, to me personally, as an investment, or at least thinking hard about it.

Why the wide wide range? Because the information is so unclear.

It is worth noting that they have NOT started ramping yet, so we cannot look at current revenue. We are looking at their TAM and what they think they can acheive.

AAOI

Similar to SIVE, AAOI depends on some insane projections. But looks better.

Zephyr is saying that in the most aggressive optical transceiver rollout, the market is expected to do 100m - 120m units by 2030. Remember, Zephyr and Citrini were both bearish on AAOI in their recent photonics post here on Substack.

This bearish position is in stark contrast to the bullish projections AAOI management has given.

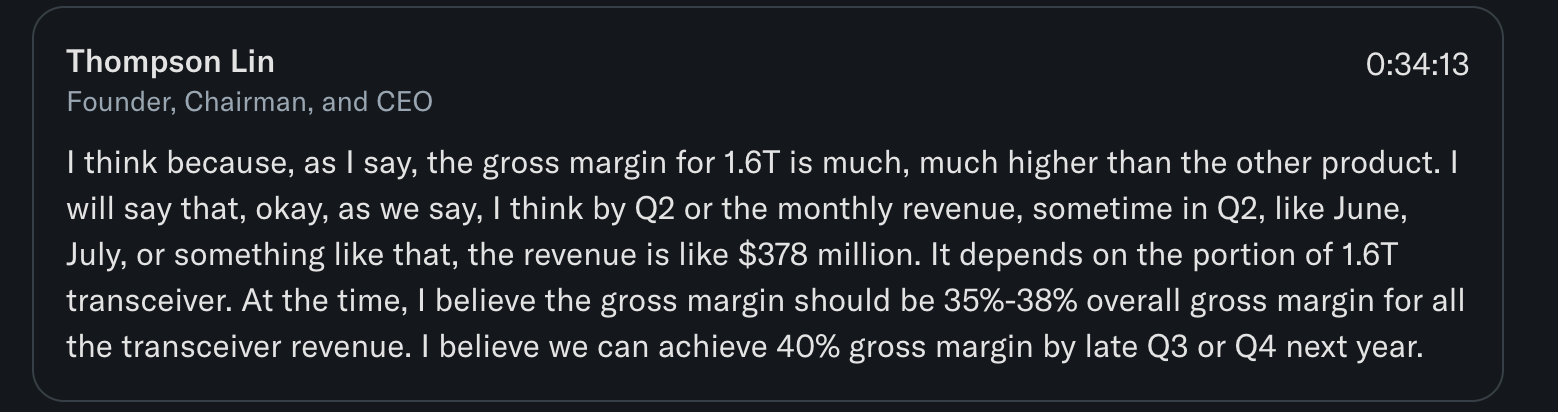

They say that they can do $378m by Q2 2027.

That’s a revenue of $1.5bn on a market cap (currently) of ~$7bn.

Let’s go with what they say, and assume they can do 40% in 2028, with a growing revenue.

By 2028 they could be doing a $2bn revenue and 40% margins. close to $1bn EBITDA.

Add the cash they made in 2027 from their bullish projections = ~500m

If market cap is constant, cash increases then by the beginning of 2028 you have a company trading at EV = $6.5Bn

Forward EV/EBITDA = ~6.5x

Not bad if you must believe the management.

These numbers are not super accurate, and it doesn’t matter in this enviroment because these numbers are going to change drastically.

It gives us a general feel. It feels a lot more ‘investment’ vs SIVE.

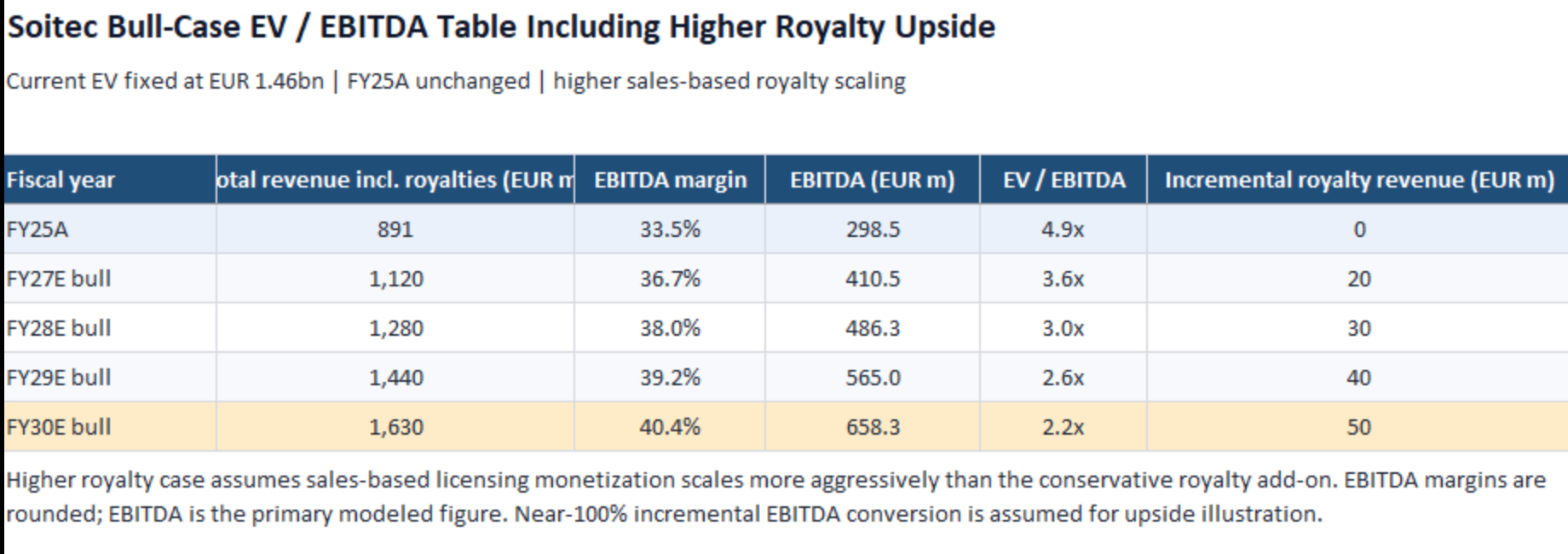

Soitec

Soitec is probably the most undervalued even at current metrics when you incorporate its:

1- Moat

2- TAM

3- Current and future multiples.

It’s probably the most undervalued photonics play.

With the best risk to reward profile.

Trading at EV/EBITDA ~7x is insanity for a company like Soitec. I am long. It is my biggest and only position in the photonics space for now.

Soitec. Is there operating leverage? What about valuation? What do the Fundamentals say?

Disclaimer: This publication reflects my personal opinion based on publicly available information and my own independent research. It is provided for informational purposes only and should not be construed as financial advice or a recommendation to buy or sell any security. Readers should conduct their own due diligence and consult a qualified financial adviser where appropriate.

Great work -

For SOI I worry about 1) yields , 2) substrate efficiency on Sipho side and 3) most revs / EBITDA still being smartphone which is likely still getting worse . Do these trouble you at all?

Great post! One correction on AOI that has some pretty major implications. The $378m is a MONTHLY revenue projection sometime mid year 2027. Not quarterly :) So now it really sounds good, dont it??