I was going to put a position on here, but as I dug deeper into ownership, and management, I came to realize this stock belongs on the Watchlist, and not a Buy. I apologize for hyping it up, I’m sure you will understand why I was excited- there is a ton of value here, and I am going to wait on a response from management before I initiate a position.

The one line that irked me was from an earnings call in February, from the CFO, where he stated that they would buy back stock at a PB<0.3. Which to me was the signal that the company is not as serious as I thought about unlocking value.

That being said, if I receive a positive response from management, about what they intend to do with the Bandai Plot proceeds (when they sell it). I will have enough information to put on a position.

As it stands now, this is a value trap.

There is not an intense amount of detail that one needs to go into to understand this company, so I will lay out the short of it here:

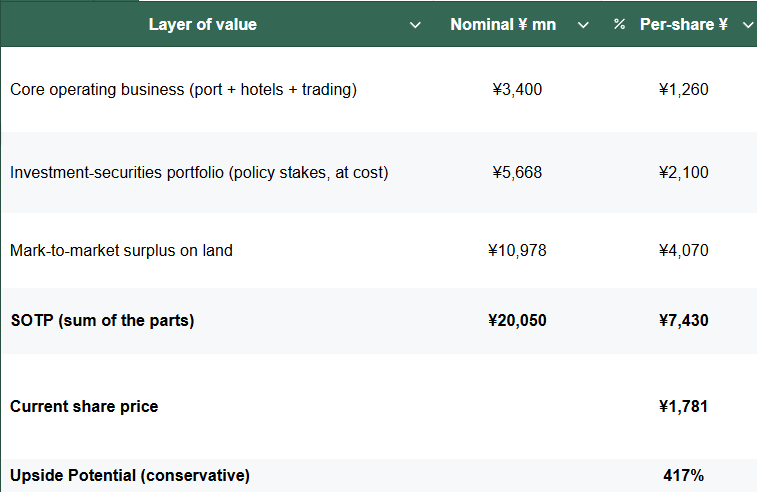

Core operating franchise (6 × EBITDA, net working debt) … ¥3,400 (¥1,310/sh)

Investment securities at ¥5,668. (¥2,190/sh) (Cross-holdings)

Monetizable Land at ~¥7,000-¥11,000. (ultra conservative value, last appraised in 2002). (¥2,700-4,100/sh)

A total intrinsic value of more than ¥20,050 equity.

or ~¥7,430 per share

Currently trading at ¥1,773 per share.

Its your typical Dirt Cheap Stock.

Why this opportunity exists:

1- Its tiny and very illiquid. Its sub $50 market cap. This, in my opinion, is the MAIN reason the stock trades at such a bargain price it is the reason many (even readers here) will scoff at the opportunity- and hence, why the opportunity exists for patient investors.

2- Management has a Capital Allocation problem. Which seems to be getting better slowly…but not quite there.

Rinko Corporation (9355.T)

Monetizable Land and Management Plan

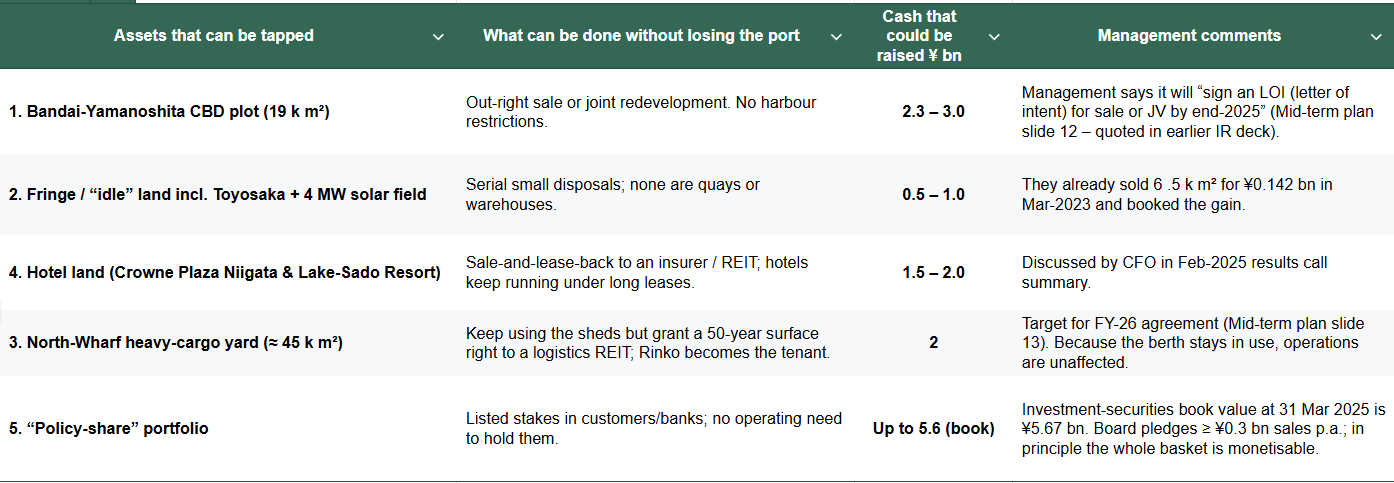

The easiest thing to monetize is their share portfolio and management has stated that they will reduce their investment portfolio every year by ¥0.3bn (They have not said exactly where the proceeds will go). The whole thing is monetizable because its a bunch of cross-holdings.

The next ‘most likely’ asset is their Bandai plot. And this is CRUCIAL to my thesis. Management said they will sign a letter of intent to sell it or conduct a JV. I hope they sell it. They could raise 2-3bn.

Bandai plot

Bandai-Yamanoshita CBD plot, 19 000 m²

2025 MLIT 公示地価 for Niigata-shi Chūō-ku, Bandai shows (¥341 k)

So 19 000 m² × ¥220k (after tax profits) = ¥4.2 bn. Cut it down after tax or a joint venture to be more conservative and we get ¥2.3-3.0bn

Other monetizable assets I have tabulated below but the investment portfolio, and Bandai plot will be the first things to watch before the others.

If they gain traction monetizing the Bandai plot, it increases probability of them monetizing the others sooner. But what they do with the proceeds is the crux- on their slides, which are all in Japanese, they have stated that they want to put 10% of their operating cash flow into shareholder returns (dividends and buybacks) while reinvesting the rest to increase ROE.

The Bandai Plot sale is not an operating cash flow, so I want to hear what management plans with that.

They have a lot of other land they can monetize too…what will happen to the proceeds?

Operating Business

Rinko’s port & logistics does ¥9bn annually. - read about it here

Hotel operations do ¥2.3bn annually.

While the operating business is not very relevant to my thesis (the thesis depends majorly on monetizing investment securities and land), they are profitable.

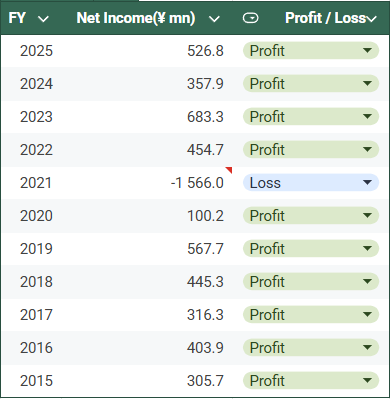

There was a tweet on Rinko that said that company was not profitable, this is false.

The company has been cash flow positive and profitable for a long time, and the loss it made in 2021 was a non-cash impairment write-down of its Hotel. (pandemic). It was cash flow positive (after capex) in 2021 too.

So the brief analysis that you may see on X is incorrect.

They run some small ancillary businesses but they are too small to effect my thesis. Like this new “dangerous goods warehouse”, and a bunch of other small operations.

Initially it looked like management was going to play ball.

They had the plan to monetize old land. Selling of cross-holdings which all looked like a positive to unlocking shareholder value.

But when I read between the lines, I figure management are more likely just conducting a ‘box-ticking exercise’ to stay off the real name and shame TSE list.

They still deserve shame because they have said nothing about trying to get their P/B to 1, which was a TSE guideline.

Let’s see what management says on the Bandai Plot, or what they plan to do with the proceeds. I’ll let you know.

Option-like payoff

This stock looks like a call option, where the cost is opportunity cost of the nominal value of your position.

-If management indicate anything about unlocking shareholder capital- the stock will rocket.

-If not, it keeps treading water until they get shamed enough to make a change.

Thanks for the writeup! I have gotten a bit hesitant with net-nets and SOTP bets. Money is easy to lose, e.g. invest with bad returns, offset operating losses or "mistakes" like value destructive acquisitions. It only means something if we as shareholders can get it out of the business. And we can only get it out if the management is very shareholder friendly and wants to give it to us (selling assets and buying back stock, special dividends). That is rarely the case. So if they would consider e.g. a special dividend from the bandai plot sale, that would be a strong signal for me that they understand what their job as managers (not owners) really is: improve shareholder returns by running a great business and monetising assets. It's not very reassuring that they don't care about their P/B and cheap shares even though they have assets and are profitable. Either they don't know what to do with their assets (invest, buybacks, dividends), or they don't think reinvestment for growth makes sense. Both options make me worry that they are not great capital allocators. And this brings me back to the beginning: I don't trust bad capital allocators with a lot of money that I can't get to.

Appreciate how you update your thinking on the fly. Keep us posted as you learn more. Management remaining opposed to buybacks at such a low fraction of NCAV is grounds for naming, shaming, solitary confinement and a diet of American gas station sushi.