This is not financial advice. DYOR.

This research is not complete, I will be editing this document as I discover more, but wanted to get this out because the market is onto these two.

I think Nippon Chemical is a superior play. I just started analyzing Sakai first so that’s why it reads in this order.

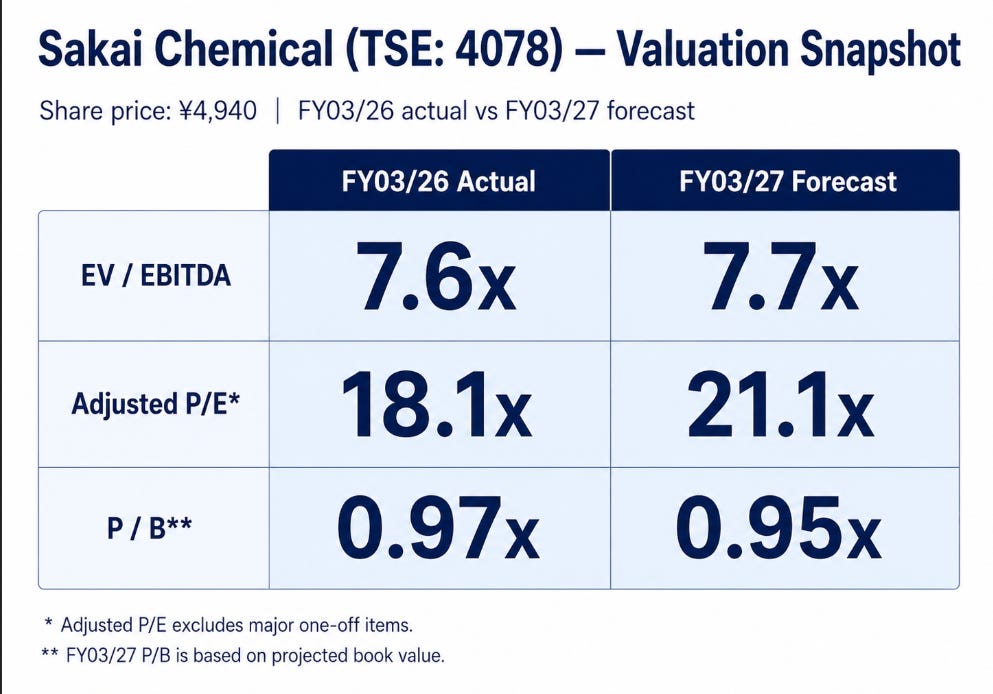

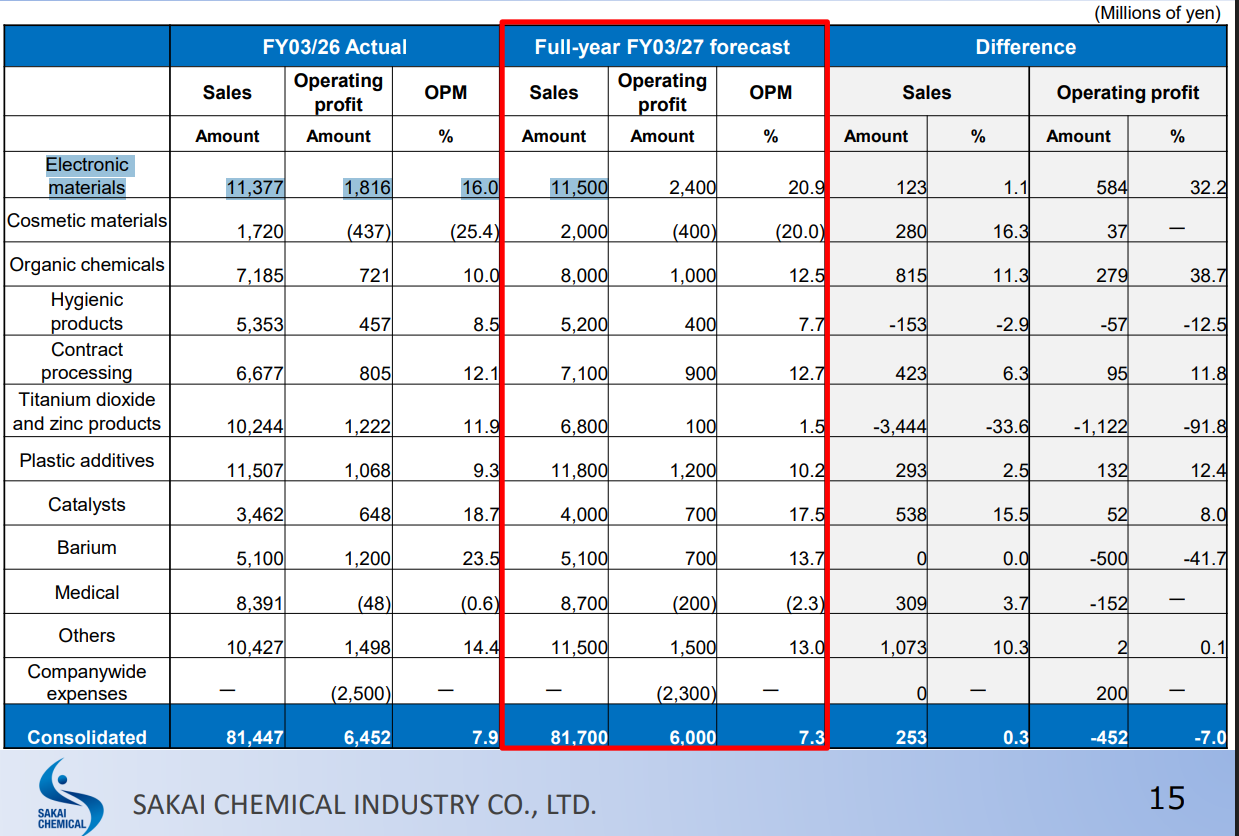

Sakai Chemical (4078.T)

2027 numbers are based on management’s estimates which I believe might be far too conservative given the growth in AI server MLCC.

The TL;DR is that:

1- 30% of Sakai Chemical Operating income, (Electronic Materials segment) is exposed to high-end MLCC most of which through its hydrothermal Barium titanate. (Not all of this 30% is AI-Server!)

2- The AI server MLCC market is expected to grow at 80%+ CAGR (, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR).

3- The company is cheap ahead of the biggest expansion in MLCC we have ever seen.

From the Zephyr tweet below:

“The AI server MLCC market is growing at 80%+ CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)

MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers.

We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27.

Humanoids are another future high-growth market for MLCCs

Book-to-bill ratio for most MLCC suppliers is over 1 now

“MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers.” -Zephyr

What is important to note here is that the MLCC market is around $15Bn. Sakai and Nippon both sell into automotive, and electronic consumables- it’s not all AI-Server. But demand is very likely to increase across the board.

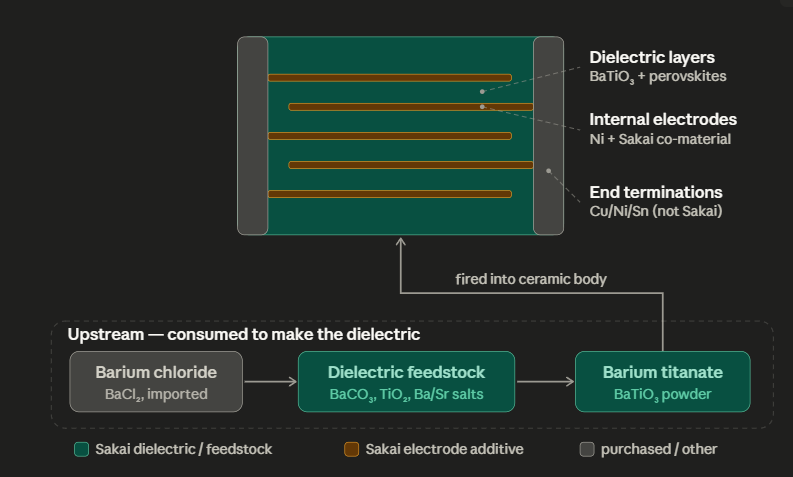

Sakai uses hydrothermal and Nippon uses Oxalate- these processes both produce BaTiO3 of extremely high quality- which is most likely the ones used in AI-Servers.

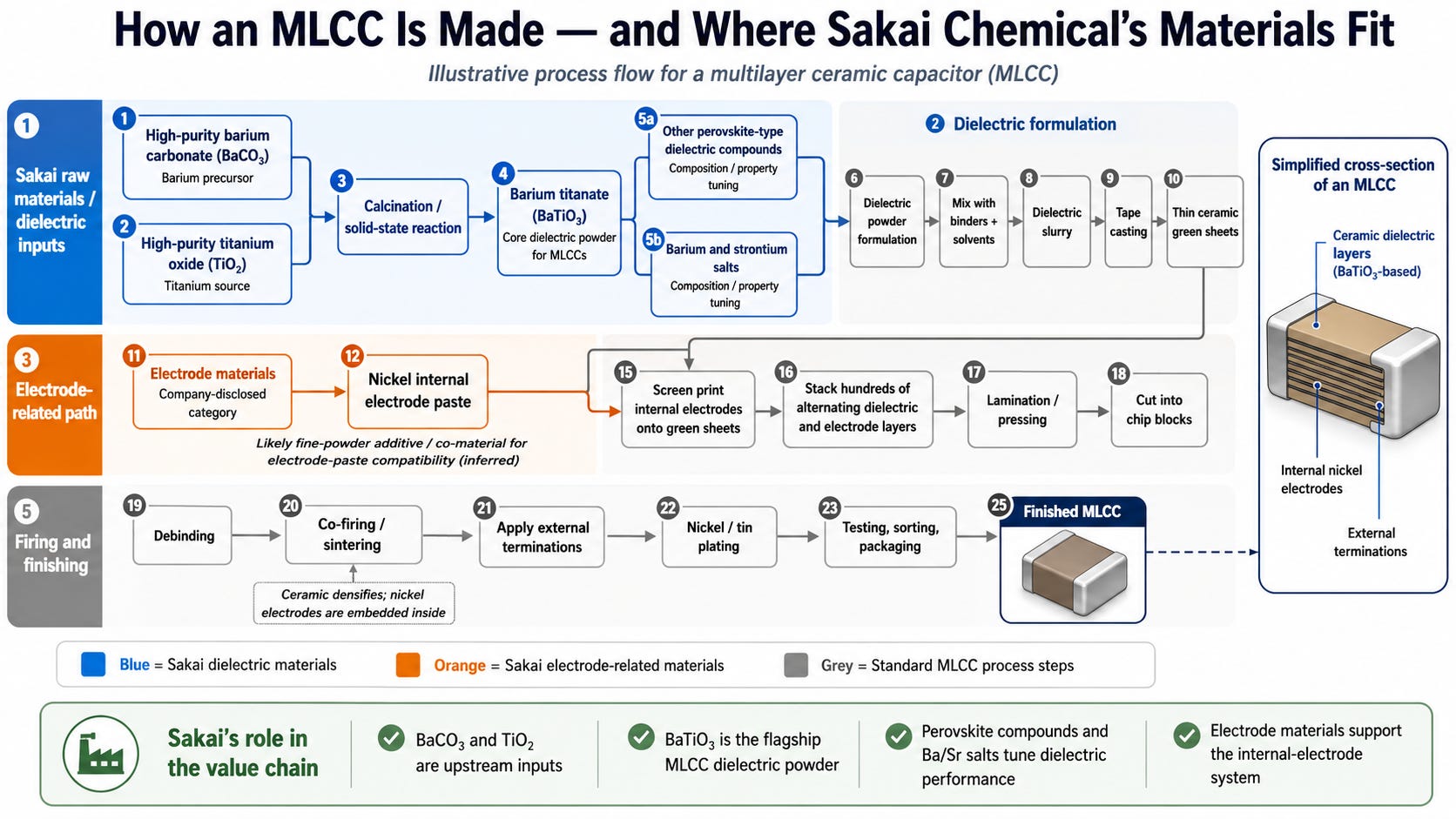

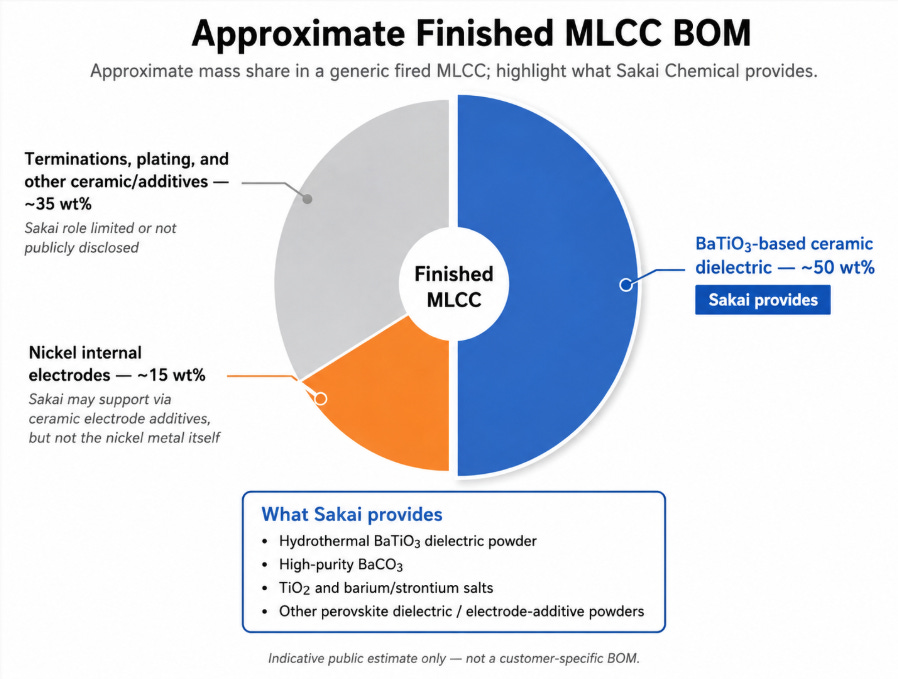

These are the materials that Sakai Chemical makes that goes into making an MLCC (multi-layer ceramic conductor)

Or a clearer diagram for you:

The dielectric layers:

Barium titanate. BaTiO₃. The flagship. This is the core MLCC product.

Other perovskite-type dielectric compounds.

Dielectric raw materials & composition tuning:

High-purity barium carbonate. BaCO₃.

Barium and strontium salts.

High-purity titanium oxide

Electrode-related:

Electrode materials.

「当社電子材料のほとんどがMLCC用途」

“Almost all of our electronic materials are for MLCC applications.”

— Sakai Chemical Integrated Report 2024.

It’s probably 99% MLCC at this point.

I am very certain they are sand-bagging their 2027 estimate for electronic materials revenue because the demand for the AI server MLCC market is growing too fast.

How exposed is the company to MLCC? Operating profit for 2027- according to management estimated, they are about 40% exposed to mostly high-end MLCC.

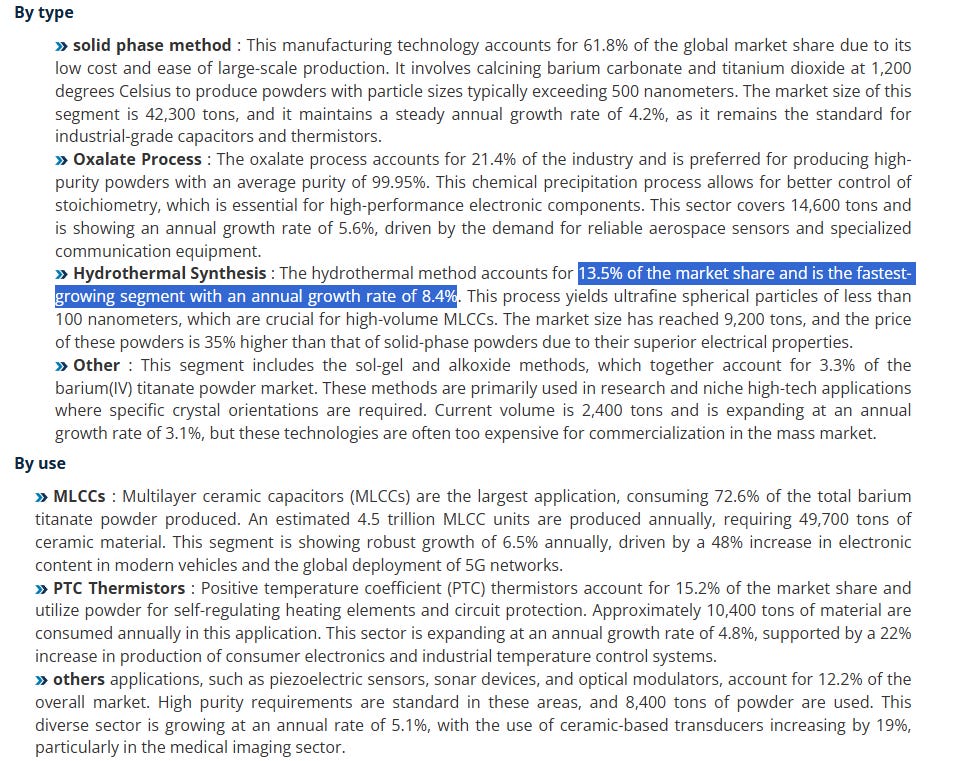

Why do I say high-end? Because there are three ways to make BaTiO3.

1- Hydrothermal. Sakai’s focus. Grows BaTiO₃ particles in a hot, pressurised liquid reaction. Produces very fine, highly uniform particles, ideal for thinner, higher-end MLCC layers.

2- Oxalate. Uses a chemical precursor that is precipitated and then heat-treated into BaTiO₃. Very uniform composition and can compete in high-performance MLCC applications.

3- Solid-state. Mixes solid powders such as BaCO₃ and TiO₂, then fires them to form BaTiO₃. Cheaper and good for scale, but particles are generally less fine and uniform.

Hydrothermal is 13.5% of the market.

Oxalate is 21.4% of the market share.

Solid state/ or phase is 61.8%.

Given that “the AI server MLCC market is growing at 80%+ CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)”-Zephyr

The demand will most likely be skewed towards Hydrothermal and Oxalate because AI servers increase demand for high-capacitance, high-reliability MLCCs.

That should benefit multiple premium BaTiO₃ routes, like Sakai.

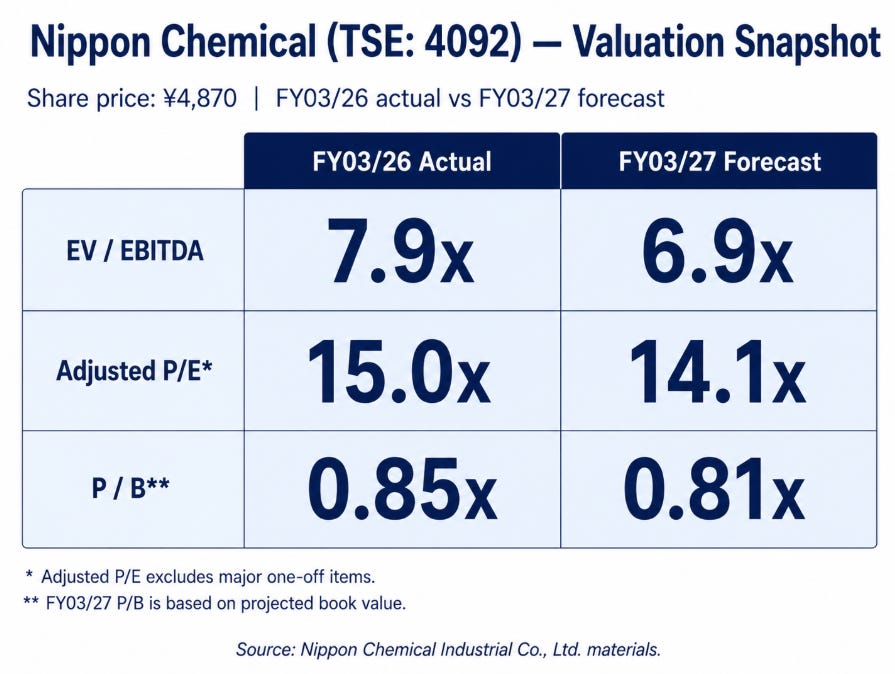

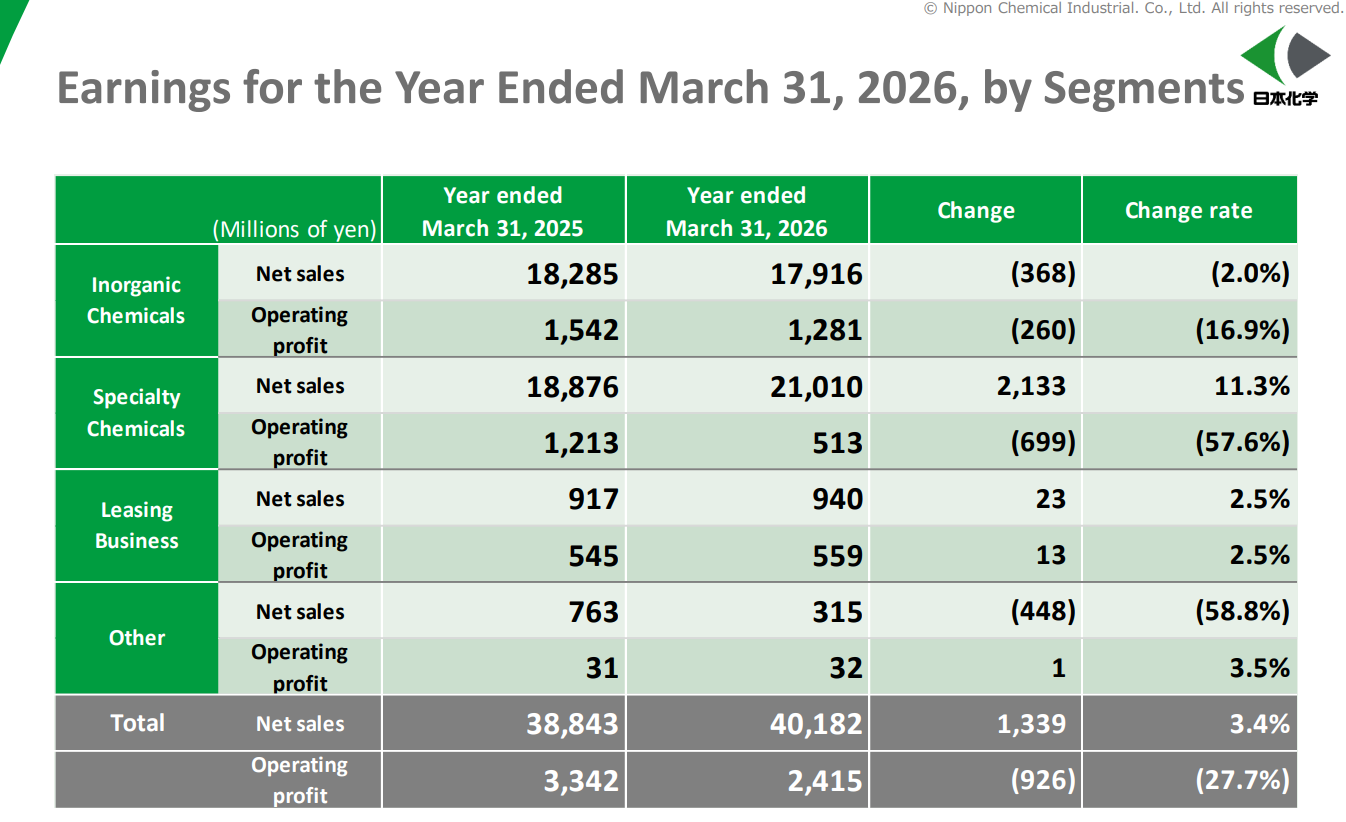

Nippon Chemical (4092.T)

Nippon Chemical is an even cheaper play to Sakai.

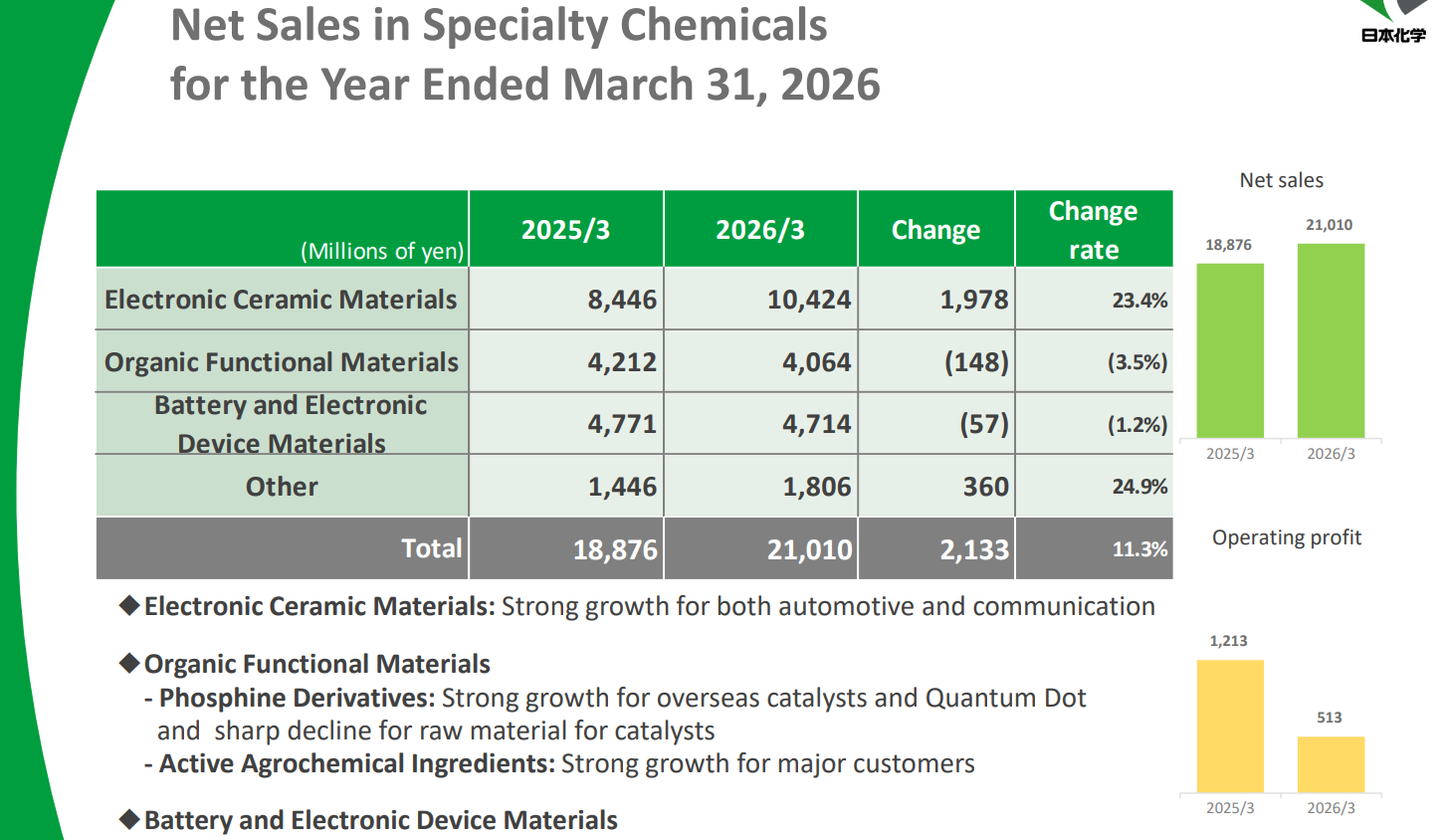

And it also likely has even more exposure to AI-server MLCC material through its own Electronic Materials segment. Which is at 25% of total revenue.

But operating profit for this segment dropped even amidst a 23.4% rise in sales for Electronic Ceramic Materials (Mostly MLCC). Caused by problems: mainly battery materials, temporary prior-year inventory benefits reversing, and restructuring, consolidation costs.

If we assume that Nippon’s Electronic Ceramic Materials segment can do the same 20% operating margin as Sakai’s, then at a 12,000(mYen) 2027 segment revenue (my own estimate) we get a contribution of a 2400 to operating profit.

This contains a lot of assumptions though, because it means the problems they had in battery materials, temporary inventory, restructuring etc, get cleaned up.

But that would push them from a EV/EBITDA 8x to EV/EBITDA of 4x in 2027. (unless share price re-rates and all else equal which is a big ask).

This 2400 is significant. The companies operating profit in its entirety was 2400 (mYen) for 2026.

They could very quickly re-rate 100%, or become far too cheap.

Nippon Chemical also has capacity to produce high-purity red phosphorous, used for optics, but the amount is not quantifiable from the statements.

Great post! Where does Shin Etsu fall in with these 2 names. Leading edge sure going to do well. Maybe a 3-4 name basket including JCU? Thanks