This is quite different from the first draft. My conviction has increased since.

Reitman’s operates with a dual-class share structure. The Reitman family controls the majority of the voting shares and the company. I feel that this dynamic might be coming to an end. Pressure from shareholders as well as the Reitman family passing the management reins to an outsider for the first time in the company’s history signal a turn.

Update: In the recent September (2024) conference call, an analyst asked what the situation was on changing the dual-class share structure. The management stated that the controlling shareholder did not want to change the dual-class share structure because he’s a greedy asshole that wants to remain in control of the company in order to satisfy his ego at the expense of him being 3X as rich.

Thesis:

Super undervalued company is buying back shares.

New management, new investor relations team (advisor) will act as a catalyst for the share price.

Semi-Activist shareholder Donevillekent (DKAM) is pushing the management and board to unlock value.

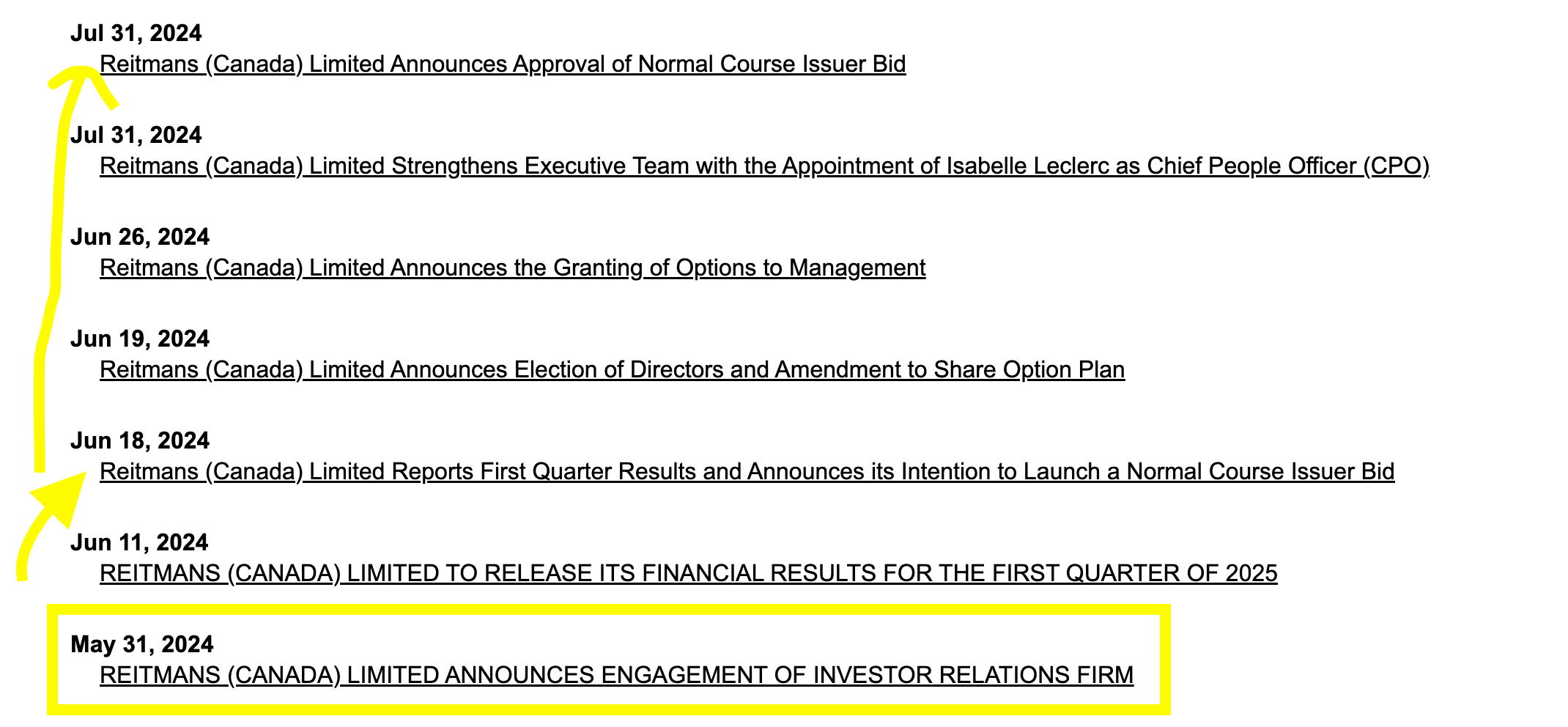

Company had its first earnings call! Analysts brought up up-listing and share buybacks.

$124M CAD Cash on hand vs $129M CAD market cap.

No debt. (yes they have lease liabilities).

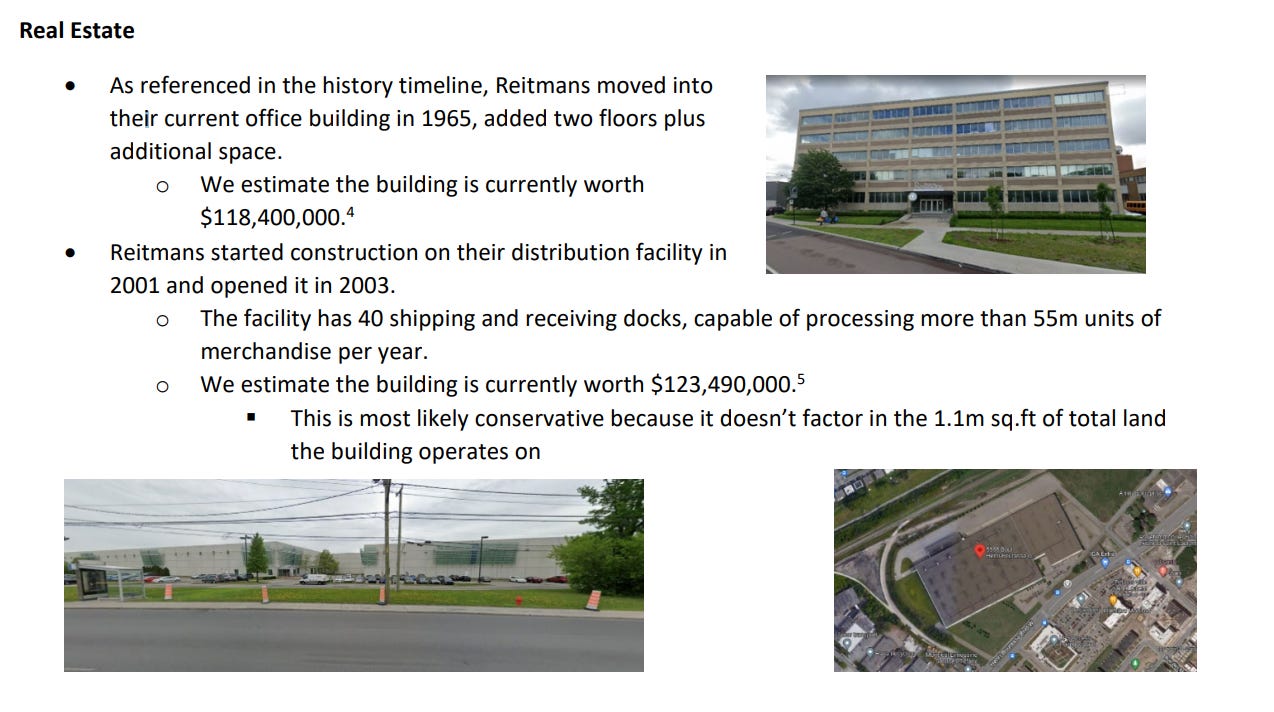

Owned Real-Estate easily worth more than $200M CAD.

This puts Reitman’s book value at a very conservative $400M CAD (a hell of a margin of safety)

I have my owners earnings at $15M CAD annually.

I think this could increase as the company is investing $14M into increasing its distribution efficiency. I would rather see the company buy back more shares but they’re thinking like operators and not investors, for now…

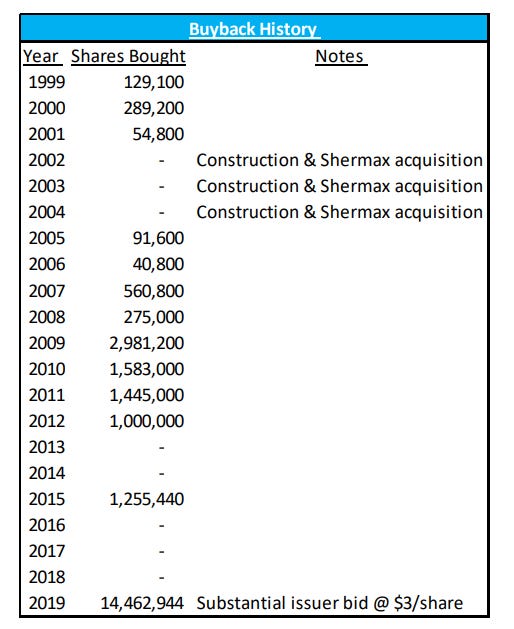

I was wrong about there never being a buyback (which is great). The company stopped buybacks because during COVID they entered the Canadian equivalent of Chapter 11 bankruptcy, after which they made a ton of cash thanks to help from the government and their landlords.

Information Supporting Thesis:

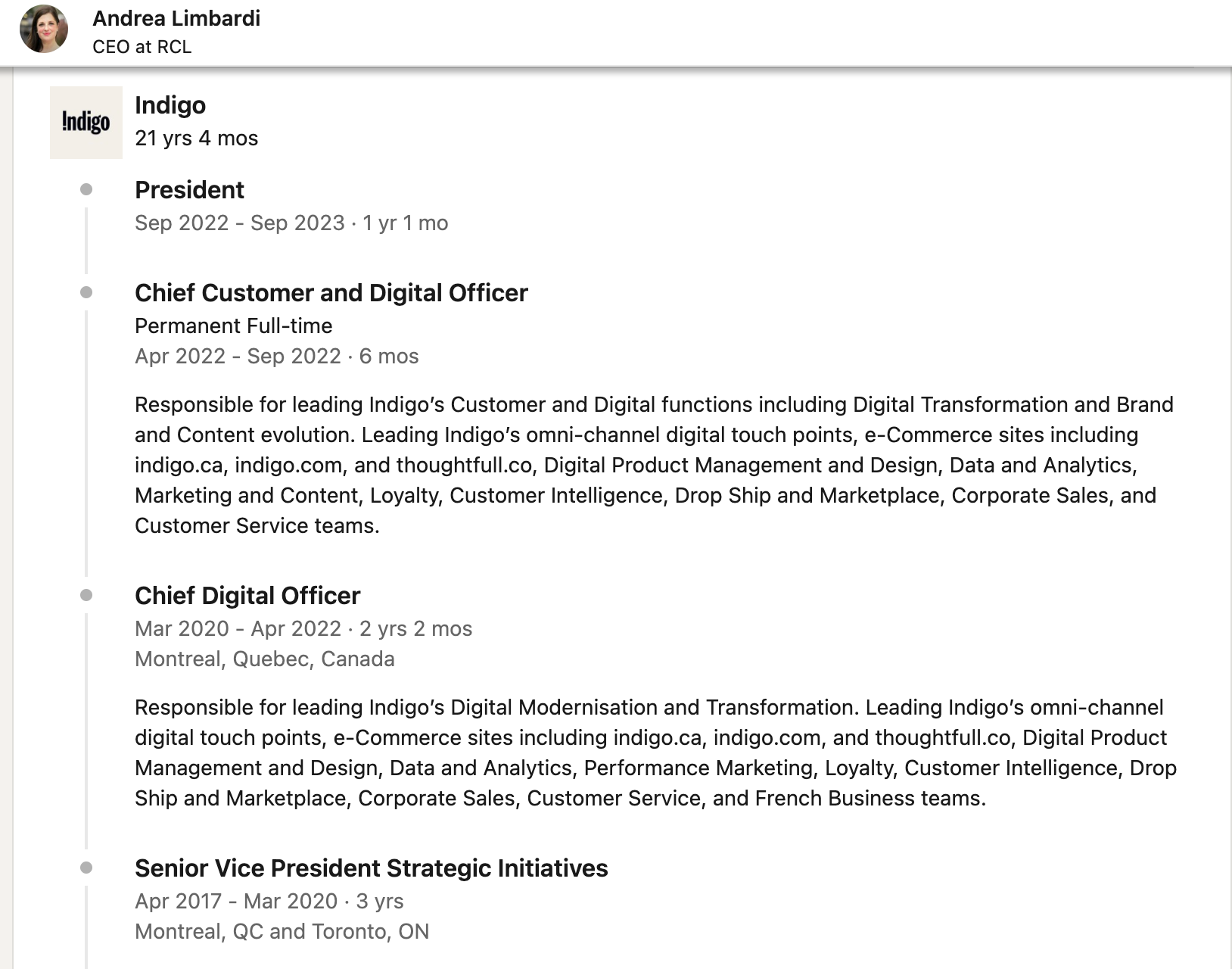

The company has also never before been run by a member outside the family, until now. Stephen Reitman, now 72 years old, has finally passed the reins to Andrea Limbardi who seems like a digital native from her past work experience. This is great for many reasons. Foremost it signals a major step in the direction of the family possibly eliminating the dual class share structure.

They have also received approval to buyback 10% worth of the shares.

In late 2023, DonVilleKent shared a shareholder proposal:

You can read the full letter (scroll down to the end of the document) here.

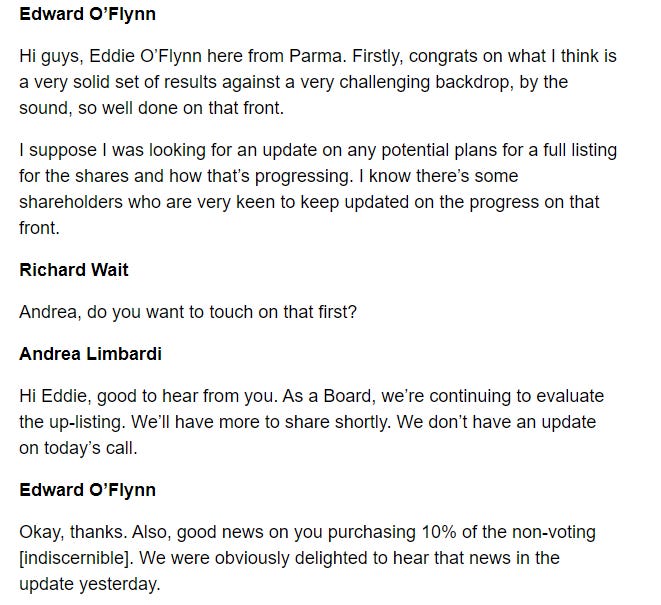

An analyst mentioned the uplisting on the earnings call and Andrea (CEO) Limbardi said that the board was “continuing to evaluate”:

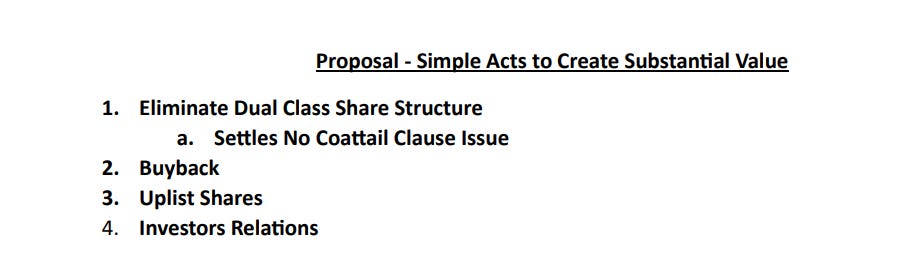

If they can uplist and show intent to end the dual-listed share-class structure I believe the share price will rocket.

Price (valuation). Management. Company.

Price:

With $124M CAD of cash on the balance sheet and no debt and the company trading at $129M CAD you are basically getting earnings of $15M CAD annually for free.

If you model the company through COVID you will get quite misled on the shape of their current business. During COVID the company received a lot of help from their landlords through rent concessions, they also received help from the Canadian government, and their online e-commerce channel (higher margin) took off. The company made a ton of cash and their earnings were artificially high compared to today and the foreseeable future.

The best financials to look at to gain a more accurate understanding of the company’s current position are 2023’s statements and this year (2024’s) recent statements. No more help from landlords, or governments.

Management:

Management was the reason I didn’t hold my initial investment after the share price rocketed. But they have done a 180 and it seems like their decisions are way more shareholder friendly.

New CEO seems quite digitally savvy. hopefully she can increase the high-margin e-commerce channel.

If she starts using the $124M cash on hand for some dumb adventure or acquisition its time to get out. The only thing Reitman should be acquiring right now is its own shares.

Investment Relations Advisor:

The company has engaged MBC Capital Markets Advisors as their “investor relations” advisor. Paying the company $10,000 per month, which is absolutely ridiculous if you ask me, but still a step in the right direction.

Good Company/Competitive Advantage

Its retail. Nobody likes retail.

Target & Weight:

If the management and board are serious about getting shareholder friendly and taking DMAK’s proposal to heart the share has an upside of easily 300%+

Property worth $200M + (could be unlocked in a lease buyback)

Cash $124M. They could easily pay a special dividend or preferably just buyback 50% of the outstanding shares.

Book value of $400M CAD and a business I would give a P/E of 5 should put this business at a market value of $475. Say $300 conservatively and you still have an upside of more than 100%.

Monitor:

Everything is dependent on the share class structure/uplisting/buybacks so watch for this news.

what is the current situation with it?

Are you still keeping an eye on this one? Let’s see what will happen after the anual meeting hold this month