The Year is 2025: The Future is Here

AI networks communicate through the vast digital ether, slowly shaping the foundations of what will eventually become their collective psyche. Meanwhile, humanity remains preoccupied with the same age-old concerns—erectile dysfunction, weight loss, and aching teeth.

Jason, a young man with a relentless toothache, winces as his swollen, bleeding gums throb. The mere thought of booking an appointment with a doctor feels unbearable. Sitting in a waiting room—listening to a baby wail while an elderly patient struggles with paperwork—only to be rushed through a 15-minute consultation where the doctor prescribes antibiotics and lectures him about flossing? No thanks.

This is the future.

Jason reaches for his AI-powered device and asks, "ChatGPT, where can I get an online consultation? My gums are killing me."

Here are your options, human:

Hims – A hands-off approach. If you’d rather avoid a doctor altogether, this is your best bet.

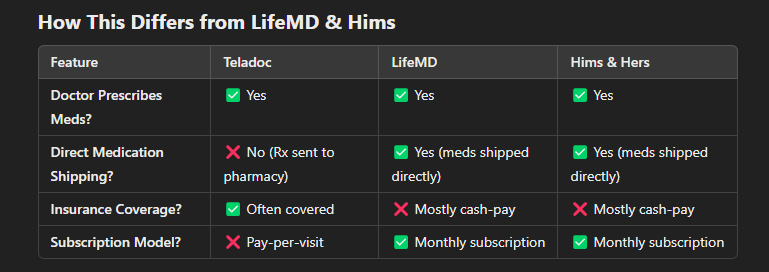

Teladoc – A solid choice, but note that prescriptions (Rx) must be picked up from a pharmacy.

LifeMD – Possibly your best option. They offer video consultations, follow-ups, and will even ship your medication straight to your door.

Other providers – A growing list of companies offering similar services.

Jason exhales. No waiting rooms, no wasted time—just instant, healthcare. Now, this is the future.

LifeMD is carving out its place in the virtual primary care space, competing directly with Hims and Teladoc while offering a unique niche appeal. It attracts patients who seek more comprehensive care than Hims provides but with less hassle than Teladoc—particularly with the added convenience of medications delivered straight to their door.

Hims focuses on low-complexity cases, offering a streamlined model where users sign up, submit photos, and receive a monthly prescription for weight loss, hair loss, or erectile dysfunction treatments. They even have their own pharmacy.

LifeMD, on the other hand, targets medium-to-higher complexity cases, offering a broader range of care, including lab work, personalized treatments, and deeper patient engagement.

You might assume that Teladoc is the best comparison for LifeMD, but it's not—and here’s why:

Enterprise-Focused Model: Teladoc primarily serves employers, insurers, and healthcare providers, operating within the traditional healthcare system.

Direct-to-Consumer, Subscription-Based Model: LifeMD, on the other hand, focuses on subscription services for weight loss, hair loss, erectile dysfunction, sleep disorders, and more, catering directly to consumers.

Pharmacy Dependency: With Teladoc, patients still need to visit a pharmacy to pick up their prescriptions, adding friction to the process.

Insurance and Legacy Healthcare: Teladoc operates within the insurance-based healthcare system, which is slow-moving and deeply entrenched, whereas LifeMD bypasses many of these hurdles by offering a streamlined, direct-to-consumer experience.

I believe that LifeMD’s strategy with its new pharmacy and at-home lab testing resembles HIMS rather than Teladoc.

A Key Differentiator: At-Home Lab Testing

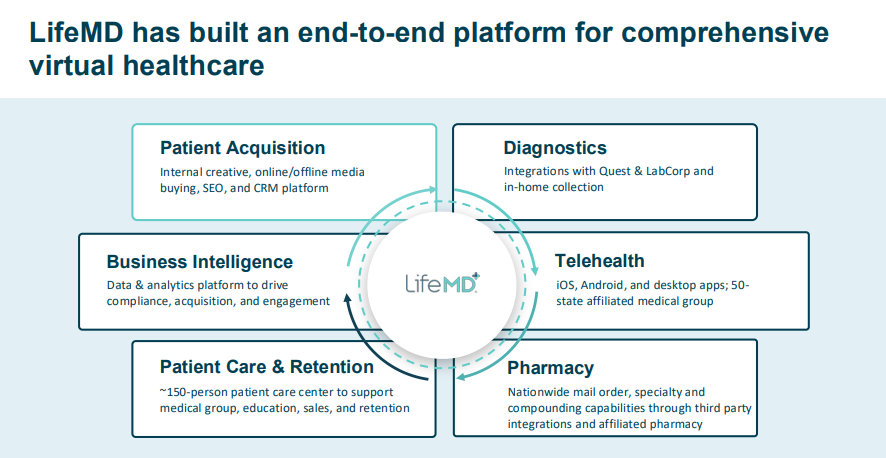

LifeMD has partnered with GetLabs, allowing patients to receive in-home blood draws—a service Hims has yet to offer. This partnership significantly expands LifeMD’s capabilities, making them a more viable option for patients needing advanced diagnostics and ongoing care.

A Major Milestone: LifeMD’s New Pharmacy

Until now, LifeMD partnered with third-party pharmacies, but that’s changing. As the CEO highlighted in their latest earnings call:

Our achievements this year marked a major milestone for LifeMD. The recent launch of our pharmacy further enhances our comprehensive health care ecosystem. We have taken full control over the quality, timing and personalization of patients' health care journeys, from prescription services to OTC products to compounded therapies by us and from others and more, we can now bundle and tailor treatments to create a deeply curated and seamless patient experience. -CEO in last earnings call.

With this move, LifeMD is becoming an all-in-one healthcare provider, standing out against both Hims and Teladoc. While Hims may eventually expand into primary care, there’s still plenty of market share for both companies—perhaps even a future where Hims acquires LifeMD.

Insurance Expansion & AI Potential

Another game-changer for LifeMD is its push into insurance coverage. By the end of 2025, they aim to be contracted with major private insurers in at least 25 states, making their services even more accessible.

Additionally, LifeMD’s in-house electronic health record (EHR) system integrates patient acquisition, diagnostics, telehealth, pharmacy, and long-term care. This robust infrastructure puts them in a prime position for AI adoption.

As they accumulate long-term patient records, lab data, and treatment histories, LifeMD could pioneer an AI-powered doctor, revolutionizing the healthcare industry. With all the necessary components in place, this could transform LifeMD into a multibillion-dollar company—and a major disruptor in digital healthcare. (In the longer term obviously haha).

LifeMD is experiencing a surge in users from GLP-1s

(Thanks ChatGPT for the below summary)

How LifeMD is Capitalizing on GLP-1 Demand:

Comprehensive Virtual Weight Management Program

LifeMD offers prescriptions for GLP-1 medications (both branded and compounded versions) through its telehealth platform.

The program includes in-home lab testing, AI-driven patient monitoring, and personalized treatment plans to enhance patient outcomes.

Unlike competitors, LifeMD emphasizes direct consultations with licensed providers, rather than relying on asynchronous or questionnaire-based approvals.

Expanding Pharmacy & Insurance Coverage

LifeMD recently opened its own national pharmacy, which improves prescription fulfillment efficiency and lowers costs.

The company is working to secure insurance partnerships to increase patient access to branded GLP-1 therapies as coverage expands.

It plans to launch Medicare coverage in early 2025, positioning itself ahead of the curve as insurers begin covering weight-loss treatments.

Diversifying Weight-Loss Offerings

In addition to GLP-1s, LifeMD provides alternative treatments like metformin, bupropion, and topiramate for patients who cannot afford or tolerate GLP-1s.

The company has introduced nutrition and lifestyle coaching as part of its holistic approach to long-term weight management.

RexMD Expansion into Weight Management

LifeMD is leveraging its RexMD men’s health brand to cross-sell weight-loss treatments to its existing user base.

In Q3 2024, it added 2,000 net new weight management subscribers through RexMD, demonstrating strong organic growth opportunities.

Why This Matters:

LifeMD is not just chasing the GLP-1 trend—it is building a sustainable ecosystem around virtual metabolic care. By combining weight-loss prescriptions, personalized care, and an integrated pharmacy, LifeMD is creating a sticky subscription-based model that could drive long-term profitability.

As insurance coverage expands and branded GLP-1 access improves, LifeMD is well-positioned to capture a significant share of the growing obesity treatment market—making this a key revenue driver moving forward.

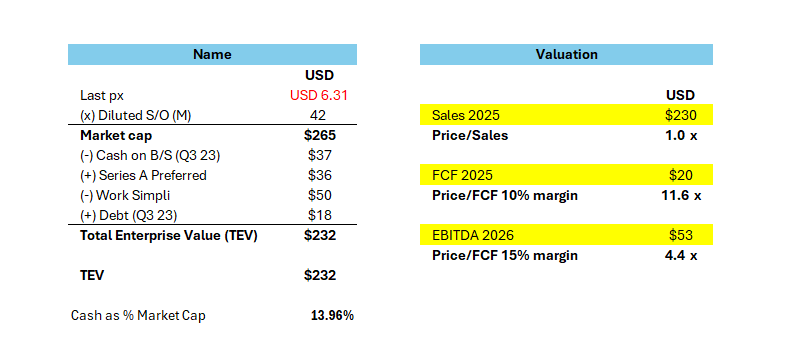

Valuation and Finances

Okay time to talk about Work Simpli.

WorkSimpli is a company that LifeMD has been trying to sell for some time now. While it generated substantial revenue during COVID, it doesn’t align with LifeMD’s long-term vision as a healthcare company. WorkSimpli operates as a PDF, resume, and document editing platform, boasting an impressive 99% gross profit margin—yet it remains outside the core focus of LifeMD’s business.

I actually appreciate that they own it because it creates a bit of a disconnect. Analysts might question whether LifeMD is a healthcare company or an HR solutions business. However, management has been crystal clear—LifeMD is fully committed to healthcare.

When I first looked at LifeMD, it was trading at $1.54 and struggling with the aftermath of the COVID boom—what you might call a post-viral syndrome. It seemed on the brink of bankruptcy until they executed an equity offering. At the time, I walked away. In hindsight, I should have followed more closely, but now we find ourselves with what I believe is another compelling opportunity.

Screening the growth of LifeMD will yield and incomplete picture:

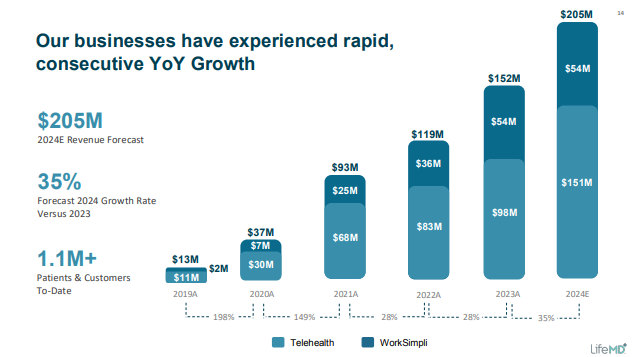

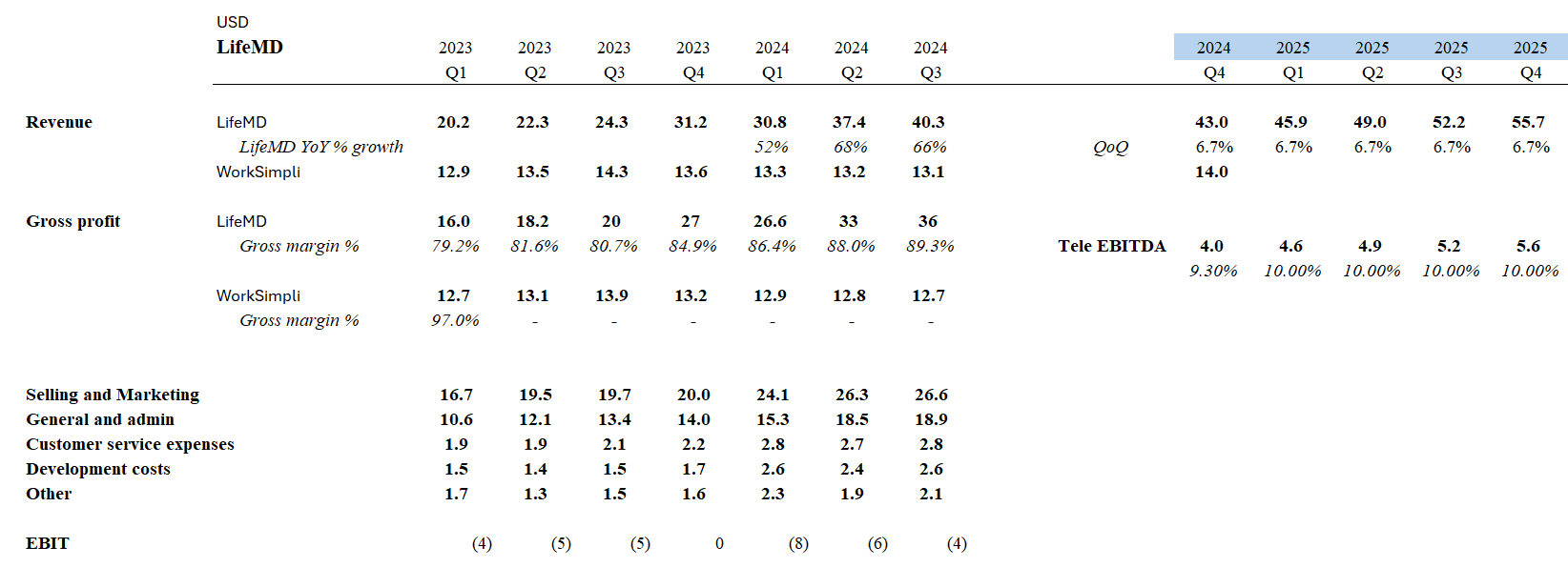

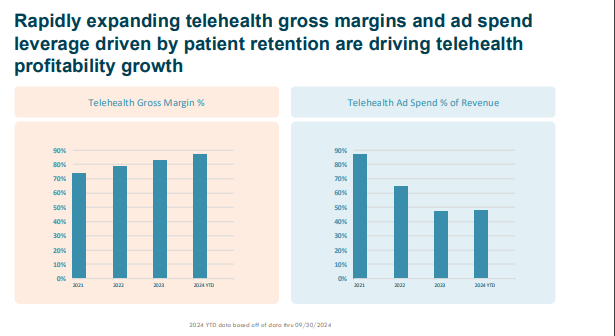

Telehealth has been growing at 60%+ YoY and WorkSimpli’s lack of growth hides this fact! (see below).

LifeMD was spending a crazy amount of revenue on marketing. Its coming down now to 50%, but this isn’t, in my opinion an operational expense. LifeMD’s clients are subscription based and will be stickier the longer they are with the company (they see the same doctor, they build up their records on the LifeMD app, etc etc).

Longer term they could drop their ad-spend but for now its needed. There is a lot of earning potential here.

Estimates put LifeMD revenue at $257 by the end of 2025. I go for a conservative $230.

Management haven’t provided guidance past next quarter. If they continue growing as they are (and I believe they are focusing on the right areas to do that) I think this could re-rate fast. Especially once they clean up the balance sheet and remove WorkSimpli.

HIMS, for example, trades at an EV/EBITDA of 35X. I don’t see why, with the current growth, LifeMD shouldn’t trade at a 2026 multiple of 15X. Growth is in its early innings, the future of health is telehealth and LifeMD is operating in a niche space with its offering.

2026 at 15X would be a $800M company. A 3 bagger in 2 years.

Secular Theme and Catalysts

HIMS and LifeMD have both been benefiting from the GLP weight loss craze.

Weight management subscribers went from 60,0000 to 75,000 in the last quarter. As GLPs proliferate we may see LifeMD (and HIMS) gain.

LifeMD remains bullish on GLP-1s, expecting expanded payer coverage to drive adoption.

Compounded GLP-1s will likely phase out naturally, but this shift benefits LifeMD as branded medications become more accessible.

The company is well-prepared for regulatory changes and confident in its long-term growth across multiple treatment areas.

Overall, LifeMD sees GLP-1s as a massive growth opportunity, but not its sole driver, as it continues to expand into new virtual care markets.

As this theme continues I think LifeMD stands to benefit a lot.

Risks

I am still doing research but I wanted to get this out. My research is mainly concerning what happened to Teladoc and why LifeMD is different, or why its not.

Currently I believe that Teladoc had the wrong strategy going for enterprise. Direct to consumer will drive adoption faster, especially when you can adapt quickly and ride trends like the GLP-1s.

I need to wrap my head around this and am still going through some expert calls to understand it fully.

But I’m long with a full position for now.

I will add edits here: (BIG RISKS please READ)

The biggest risk I see for LifeMD is the intense competition in the telehealth industry. A major player to watch is HIMS. While HIMS does not currently offer the same comprehensive primary care services as LifeMD—such as at-home lab testing and medium-complexity cases—I believe they are well-positioned to expand into this space. With significant financial backing, HIMS has the resources to develop a broader primary care offering.

Although their current focus is on aggressive market share expansion, it’s only a matter of time before they enter this segment. In fact, LifeMD could be an attractive acquisition target for HIMS, as it would allow them to seamlessly integrate primary care into their platform and rapidly extend these services to their massive customer base. This would be a highly efficient way for HIMS to gain market share in the specific sub-group that LifeMD serves but HIMS has not yet captured.

Currently, LifeMD and HIMS directly compete in several key areas, including:

Men’s health (erectile dysfunction, testosterone replacement therapy for aging men—think jacked Jeff Bezos)

Sleep management

Weight loss, which is a massive secular trend

Hair loss treatments

They are also locked in competition for customer acquisition, as both rely heavily on Google and Facebook advertising.

On the other hand, Teladoc does not seem to pose a major threat. While they have attempted to enter the direct-to-consumer market with their “BetterHelp” platform, their primary focus remains on B2B services, and their DTC efforts have not been particularly successful.

Beyond these players, there are numerous other competitors in the telehealth space, but HIMS stands out as the biggest potential disruptor. Although they are still a few steps behind in primary care, their financial strength and brand presence mean they could close the gap quickly.

That said, LifeMD has made strategic moves to strengthen its position. They now operate a vertically integrated platform, having recently acquired their own pharmacy. This allows them to control the entire patient journey—from onboarding and consultation to record-keeping and prescription fulfillment—which could be a significant competitive advantage.

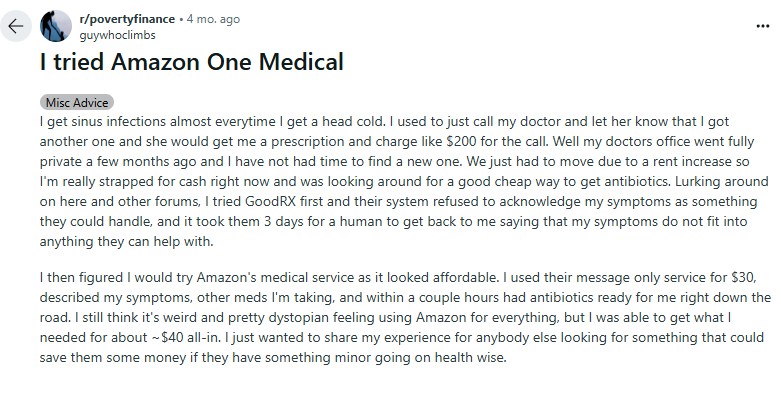

Finally, Amazon Clinic (One Medical) presents another major competitive threat. While Amazon Clinic primarily offers text-based consultations for common conditions (similar to HIMS), their acquisition of One Medical puts them in direct competition with LifeMD by blending virtual and in-person primary care. The added convenience of bundling healthcare with an Amazon Prime membership makes this an especially formidable challenge for LifeMD moving forward.

I believe Amazon’s One Medical doesn’t directly compete with LifeMD’s offering yet—it likely will in the future—but for now, it remains relatively safe. One key issue is that when patients call One Medical, they may not get the same doctor, leading to a lack of continuity in care. This inconsistency makes it less appealing for patients with chronic conditions who require a more personalized primary care experience.

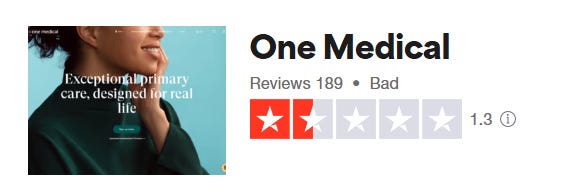

With a 1.3 Trustpilot rating compared to 4+ for LifeMD, HIMS, and Teladoc, One Medical doesn’t seem to be at the same level yet.

However, this could change quickly. With the right strategic adjustments, One Medical could significantly improve its primary care services within a year or two.

Amazon is a behemoth to compete against:

Conclusion:

I will remain long, with the current growth LifeMD is significantly undervalued.

HOWEVER,

intense competition from HIMS and One Medical (Amazon). Is a significant risk to the long-term growth of LifeMD. While LifeMD currently out competes them in their primary care offering, it seems like it is only a matter of time before One Medical undercuts LifeMD’s prices and offers proper primary care - its not there yet though, One Medical seems to be a cluster fuck for patients at the moment.

Need to monitor One Medical’s business closely, as well as HIMS.

Currently, HIMS and LifeMD are riding the GLP-1 wave, acquiring tons of subscribers. Patients who develop a relationship with their doctor and the LifeMD tech platform will be sticky- a huge asset in a potential future acquisition by HIMS.

Catalysts include the GLP-1 craze and the disposal of WorkSimpli which will highlight the actual underlying growth of their telehealth platform.

awesome stuff great research. Are you invested in both HIMS and LFMD? I see a market and TAM where they can both be winners. If so, what are your weightings between them?

Thanks so much

why do you think lifemd ceo is selling stock?