In future I will be posting all of my entries/exits in the Substack Chat and by email. Please flag my emails as IMPORTANT for Gmail to not flag it as “promotions”. This way you won’t miss out on entries like $OMSE or exits on things like $LFMD.

Closed Out Positions:

$LFMD

I took off most of my $LFMD for a 95% gain. (I did post about this on twitter).

I do realize that this sort of ‘trading’ needs to be better publicised. I expect to do a similar thing with my recently initiated position $QFIN- if we get a short-term pop, I would rather lock in the gain, especially something like 100% within a few months. I generally leave on a small tracer position, because there have been too many times where I see something blast off further.

The rest I got out basically at break-even but it was a nice ride. Market was not discounting the growth, since then, the thesis has changed quite a bit and I will not be re-instating a position.

Earnings Updates:

$CCSI

Still holding full position.

CCSI 0.00%↑ has completely round-tripped, from up 60% after posting to only up 5%. However, I think after the post-earnings plunge it offers an even better entry point. It has also been sold off further in this whole “small-caps mini-sell-off”, which I think offers a good opportunity for everyone. The situation with CCSI 0.00%↑ is far better than when I first posted it. I’m VERY bullish on CCSI at this price.

TL;DR - Corporate segment is growing, net retention rate is at 102% (perfect), management has almost hit debt-paydown goal and has indicated it will use cash flow on more equity buybacks. This looks better than when I originally wrote it up (even with the price appreciation factored in).

Price Action post earnings surprised me. I like the results. Management is being risk-averse using most of the excess cash flow to pay down debt (not a bad thing).

SOHO is down, naturally. Eventually SOHO’s decline will taper, but that is not core to our thesis- management is investing marketing dollars into growing the corporate segment.

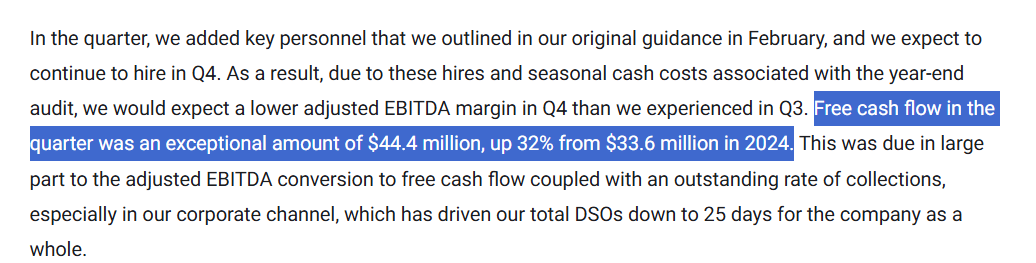

Free cash flow of $44.4m in one quarter on a stock with a market cap of $474m. This is absurdly cheap, and generating tons of cash. Hoping next quarter we see a bunch used for share repurchases- given the history of capital allocation, its highly likely.

Share based compensation (SBC):

SBC runs at around 18% of Free Cash Flow. It is quite generous. Digging further, we see that the price at where the PSUs vest are around $30. And then a mega amount at like $60.

Management has incentive to keep get the price to $60, because that’s actually where they make bank. The market will probably use this zone to sell, or it might be a point of resistance.

That being said, the price is cheap at these levels, and management is incentivized to increase the share price. My target to get out is around $50-55, before the real PSU’s vest.

Most importantly, the shares outstanding is decreasing, so the SBC is not disrupting the mechanics of buyback engine too much. Technically speaking, the reduction in shares outstanding leads to constant upward pressure on the share price.

$BETS-B

Still holding full position.

Bettsons total shareholder return (Dividend% + Sharebuyback%) is around 8%. I’m very happy to have this while Bettson continues to grow.

We have now completely round-tripped on Betsson AB since I posted. I am still holding my full position and I think the market is drastically undervaluing the company. I believe the pressure on the share price is from general iGaming market pressures- none of which I believe are that fundamental to Bettson given the growth in Brazil, and the rest of the South American market. The company, and the industry, are still growing fast there and its a big market.

Betsson is trading at an EV/EBITDA multuple of ~5-6X, compared to 15X+ which is the industry norm (especially for an established player like Betsson).

This reminds me a lot of my Super Group call which has done 200% since I posted. I believe Betsson is extremely well run, and in a similar position- I think its undervalued because of where its listed. They reported earnings a while ago (all good stuff)- here was my update.

$8371.HK Taste Gourmet Group Ltd

Still holding full position.

Taste Gourmet is doing as expected. Its up 25% since posting and that’s excluding its dividend, which is now running at a forward rate of around 10%.

It’s doing FAR better than the other restaurant groups I spoke about in the writeup. And I believe this is because management is balanced in their expansion strategy.

The market looks too pessimistic given what Taste Gourmet has been able to achieve over the last year.

Cash flow is extremely strong. Remember we have to account for lease payments which show up in the financing section of the cash flow statement. But dividends are up, and EBIT is up, and I am happy with the results. Not too much to say about this business but there are a few points to note:

Average spend decreased slightly, so we will have to monitor this.

New stores opened are still getting to max profitability, so there will be a constant drag on margins until this company stops opening new stores- at which point market will get a very clear indication of what steady state earnings will be, and multiple expansion should increase.

QFIN Qfin Holdings Inc

Still holding half a position. Not increasing.

QFIN is still extremely cheap. Like, extremely. And they are plunging their cash flow into buybacks and dividends. What’s not to like?

The reason I am not adding here is because the business got slightly weaker, but not weak enough to justify a complete change in the fundamentals, or the thesis. If I see the thesis changes fundamentally, I will cut this completely. Right now, its a wait-and-see.

There’s isn’t too much to add. What to watch:

Composition of their business- capital heavy vs capital light. (They have essentially two business segments- one where they lend money to consumers and they themselves bare the risk, and the other where their platform facilitates other lenders to make loans (the super high margin great business). It moved slightly to their more capital heavy business.

Delinquency rates increased. But within range of what they have seen historically. This is the MAIN thing to watch. If delinquency rates increase too much, then it signals there is a fundamental change in the structure of the market where they operate. We have seen this in China before, in China the market changes fast because the government is constantly tinkering with policy.

The short report Grizzly reported was basically (I think) just fear and doom and allowed grizzly to put a short position on and take it off immediately after they posted. It was lazy research. Their main “short-points” were:

1- SARM numbers not being the same as the SEC financials. QFIN has come out and publicly stated the numbers Grizzly used are wrong. I have not seen the documents, I tried to access them but cannot gain access even with my connections in China.

The governance is shady. Their main point was that the former controlling shareholder is a fraud. He doesn’t control the group anymore, though. The two points Grizzly makes are contradicting, if the company doesn’t make any money, then how have they such a large quantity on dividends and buybacks? If you have been following Grizzly Research for some time, you will know that they have been called out for having done lazy research. My honest opinion is that they run a short-fun where they post a ‘doom-report’ to benefit off of a short-term sell-off then cover their position immediately. Basically market manipulation, but in the gray area where they cannot properly get in trouble legally, even though they face a few lawsuits.

OMSE Energy Technologies Inc

Still holding full position.

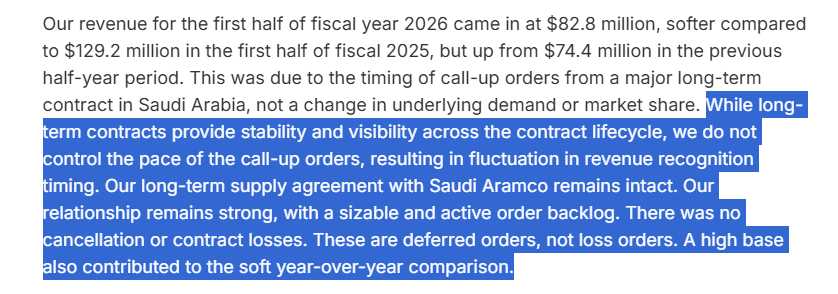

What a crazy market it has been for $OMSE. In the two weeks after I posted, the stock surged some 60-70%, only to completely round-trip back to where I bought it!

Its an interesting investing-psychology experiment, as it was zooming up many were messaging me asking if its still undervalued, is it still worth getting into at the current, elevated price? I wonder how many people now will want to get in now that the price has dropped. If you felt more confident as the price was rising- congratulations because you fell victim to ‘herd-mentality bias’. If you can start noticing what that feels like, becoming more aware of it, you can make real money in the stock market. You will always ‘feel’ that, its built into your primal psychic architecture. But notice it, be aware, and then go against it- when the fundamentals tell you to.

The OMSE 0.00%↑ earnings were fine. Management stated that current earnings were depressed from the norm due to abnormally large orders from their Saudi customer in the first half.

Welcome to small caps.

If we go on what the CEO says, the business is fine. Just fluctuating orders. He says demand is still great. Backlog is strong.

More importantly were his comments on capital allocation, which was essentially a non-answer given he said they would use the proceeds for everything- organic growth, joint ventures, acquisitions. He is just leaving the door open for any opportunity. If they can keep growing organically we can be happy. This company is dirt cheap.

Same here. Fantastic overview. Keep it up!

Great write up. Like it.