This guy is a pharma-wizard and he likes CRMD too:

Q3 update

CorMedix’s Q3 looks great for the original thesis!

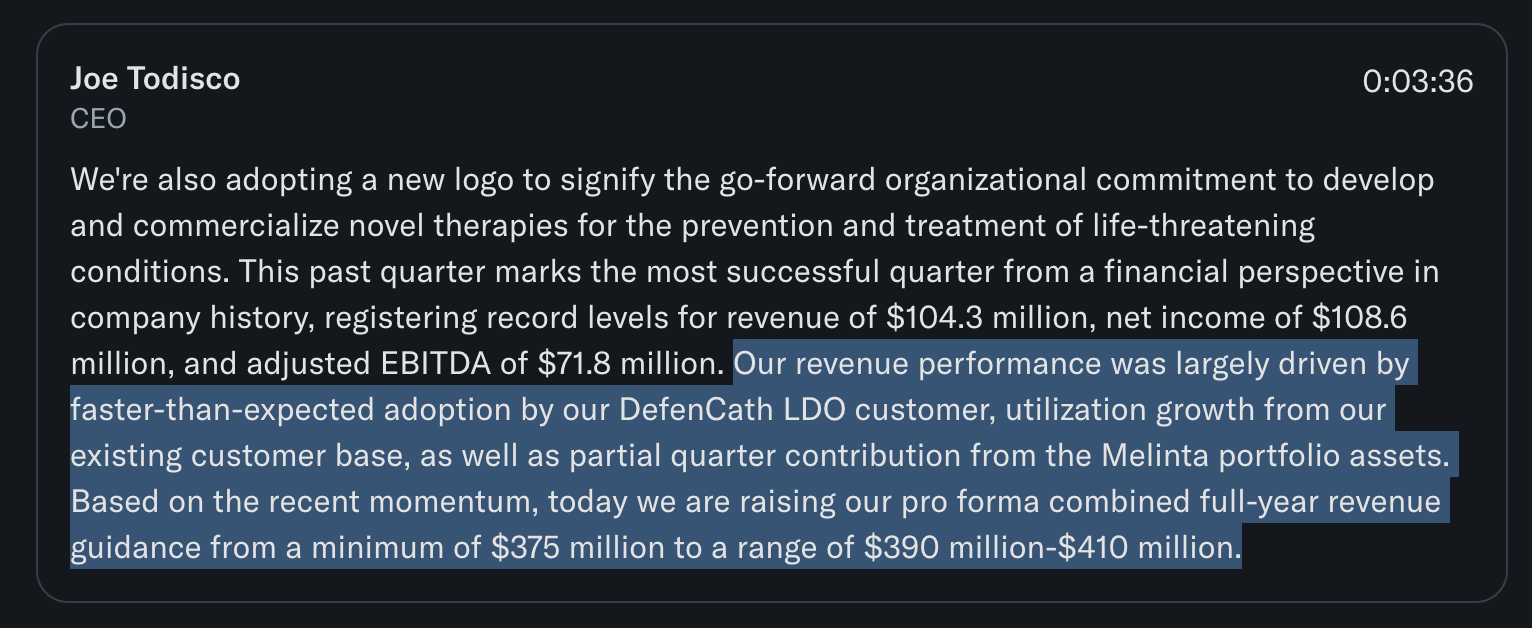

They reported $104.3m in net revenue, of which $88.8m was Defencath and about $15.5m came from one month of Melinta. Adjusted EBITDA was $72m.

On the thesis:

We are getting validated on our “Defencath launches well, throws off real cash, and gives them bargaining power for post-TDAPA”. LDO(Large Dialysis Organization) uptake is running ahead of expectation, and we’re already seeing strong EBITDA.

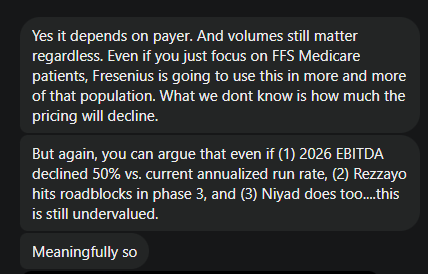

The part that says “long-term value depends on what happens after TDAPA and the add-on periods” is still unresolved. Q3 doesn’t answer what net price or what patient retention you get once Defencath is fully inside the bundle, it only shows they’re going into that phase with much more firepower.

On valuation,

EV now:

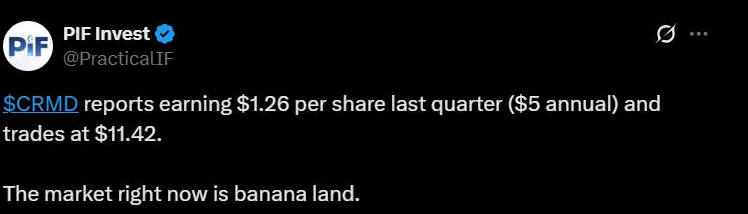

With the stock around $11.4, roughly 86m diluted shares out, $150m of converts and about $56m of cash and short-term investments, you’re looking at an enterprise value in the ballpark of $1bnCurrent EBITDA:

Q3 adjusted EBITDA was about $72m. Real Operating income around $50m. If you do nothing fancy and just annualise that single quarter (4 × 72), you get roughly $288m of “run-rate” EBITDA. Bear in mind- EBITDA should be growing like crazy until it gets fuzzy at H2 2026.Forward EV/EBITDA using that 72m:

Take an EV of about $1.0bn and divide by a $288m run-rate and you land at a forward 3.5× “Q3-run-rate” EV/EBITDA. Again- this is using a low EBITDA. EBITDA will most likely grow until H2 2026.

So unless the share price starts going up fast, this is going to hit a lot of screens as investors start seeing a company growing at double digits, with an EV/EBITDA below 5.

Below, the light-blue is my really meager assumptions. H2, 2026- we don’t really know what will happen with the prices of the vials, or the amount of patients on Defencath.

But at this price, with the economic value of this drug, this is a bet I want to take. Increasing my position.

From a health expert who works in the healthcare space in the U.S:

The opportunity has substantially de-risked since I first published on it. I'm using this as an opportunity to increase my position. This is not financial advice.

2. The acquisitions and what they do to the thesis

The Melinta deal is what really changes the story.

CorMedix closed Melinta on 29 August, paying with cash plus $150m of converts and some equity. In Q3 you saw just one month of Melinta revenue (about $15.5m, of which $12.8m were portfolio sales) flow into CorMedix’s P&L. Management now talks about $400m of pro forma revenue and $230m of fully-synergised adjusted EBITDA for 2025, implying a much larger, more diversified business but still with a core cash generator which is Defencath.

For our thesis it’s a positive. It means the company is more diversified. More avenues to make cash, and the acquisition happened at a decent multiple.

3. Some tidbits from the call that I enjoyed.

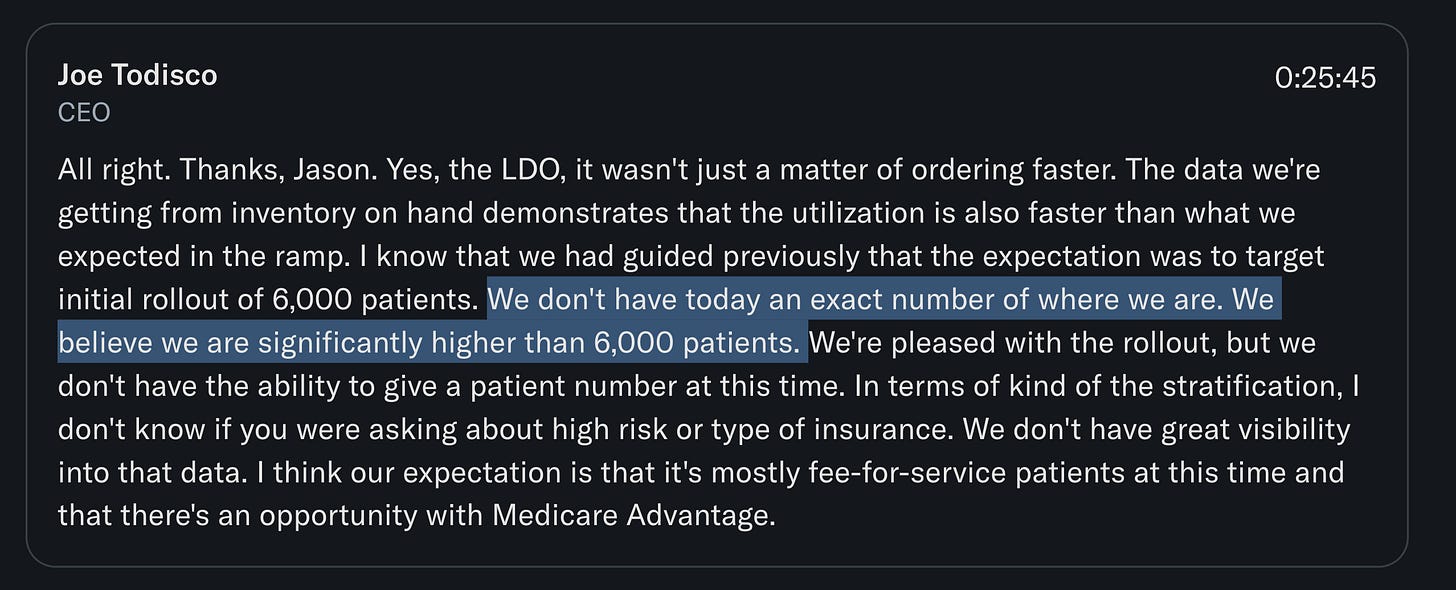

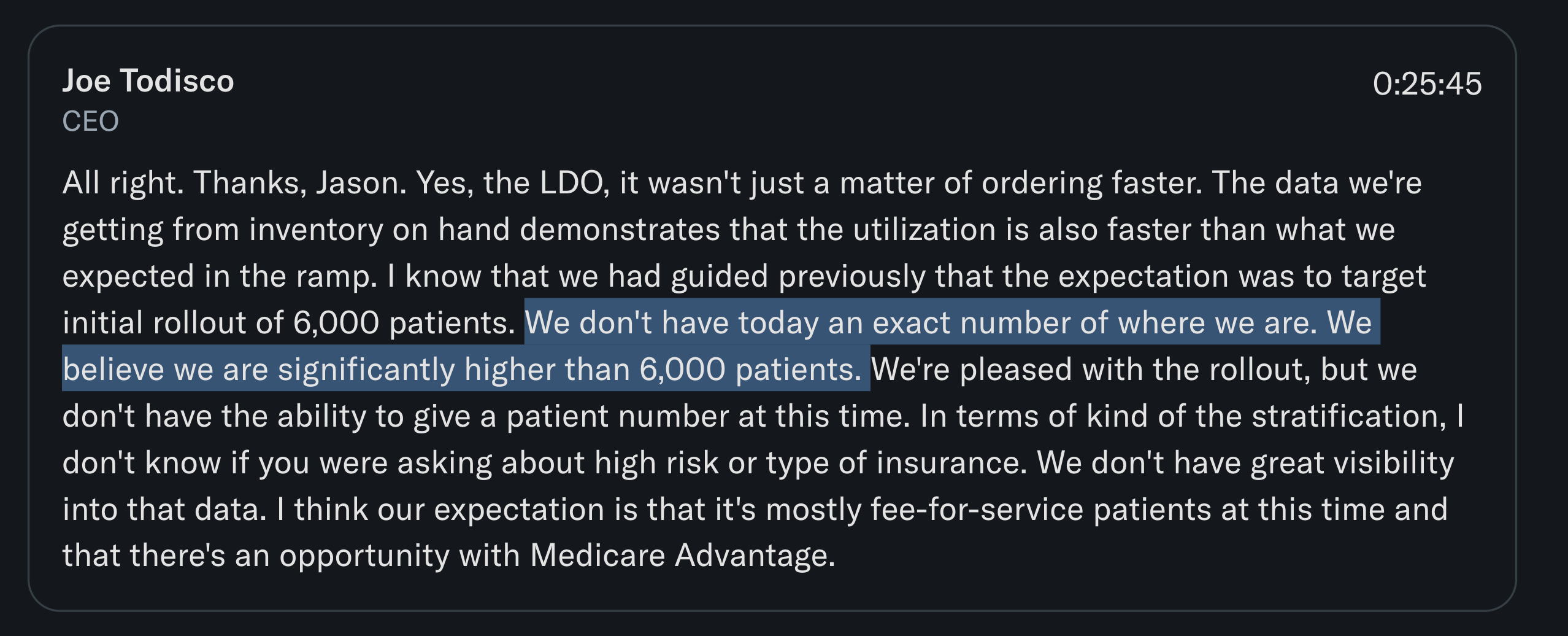

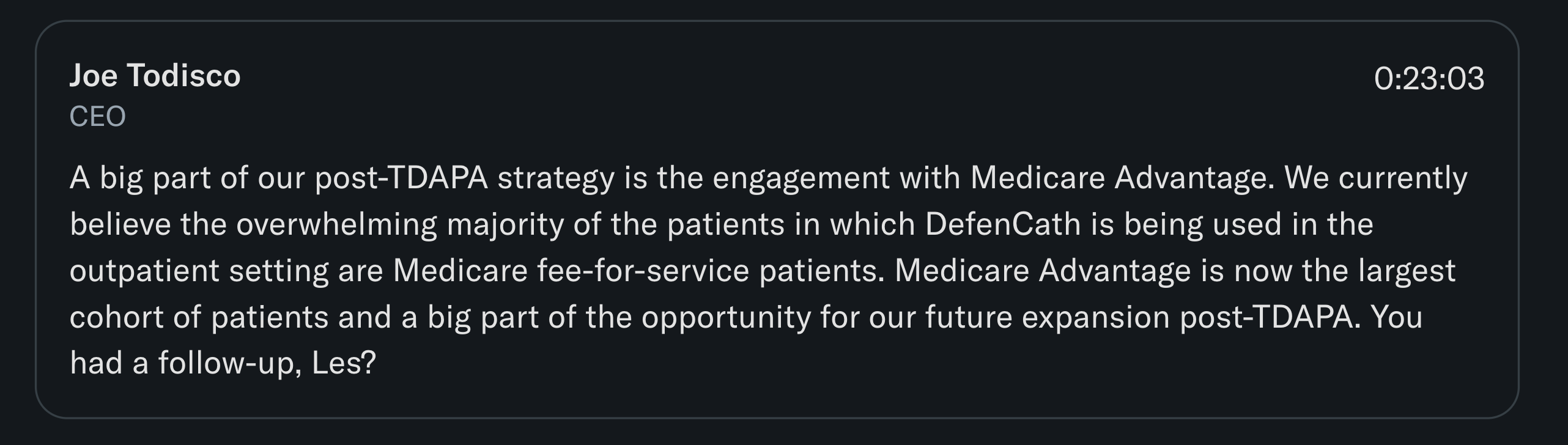

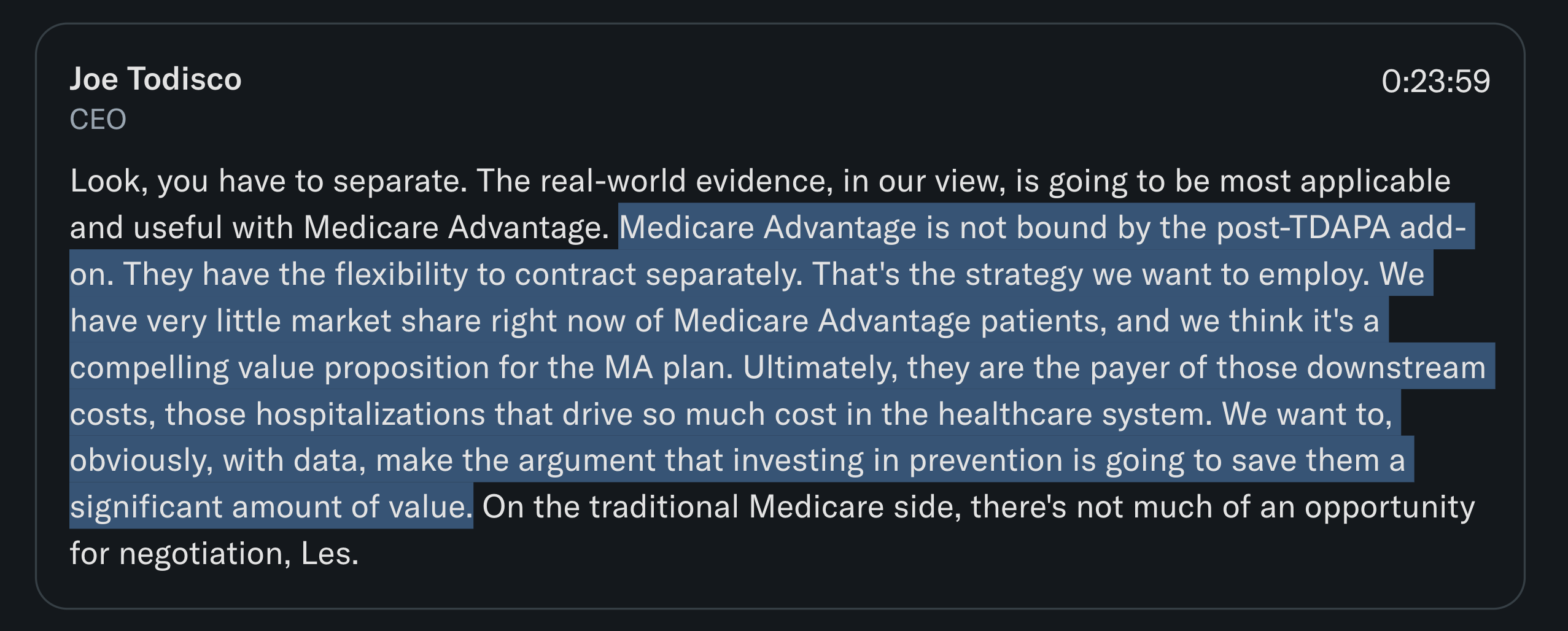

This might be confusing, but Medicare Fee-for-Service is different from Medicare Advantage. What Todisco is really saying is that Defencath today is used mostly in FFS patients, while Medicare Advantage is now the largest dialysis cohort that they’ve barely penetrated. That’s great because MA plans aren’t bound by the post-TDAPA add-on and can contract separately if the real-world data show Defencath truly cuts infections and hospitalisations.

Thanks for the update. Can I ask what are the main arguments of the bears? The short interest is significant at 20% and has kept rising thruout. Defencath uptake, post TDAPA pricing, Melinta acquisition?

Many thanks again, great work, much appreciated

Thanks. Bought when you said so.