Betsson AB is a Swedish-listed online gaming group.

It operates a portfolio of consumer brands (e.g., Betsson, Betsafe, NordicBet) and a proprietary tech platform that delivers:

Online casino games (slots, live-dealer, table games) – its largest revenue stream.

Sportsbook – pre-match and in-play betting on global sports.

Smaller verticals like poker and bingo.

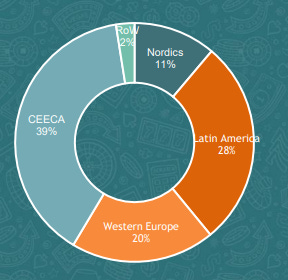

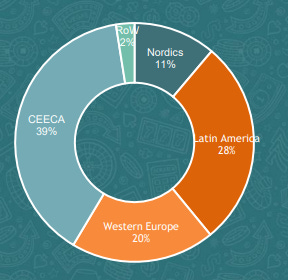

The company targets regulated or soon-to-regulate markets in Europe, Central & Eastern Europe, and, increasingly, Latin America (Brazil, Colombia, Peru). It also licenses its platform to third-party operators on a B2B basis.

Let me just say, I think the drop post-earnings was unwarranted. Results were good.

This is a capital light business, high cash conversion, with a product that is more addictive that fentanyl (I have no proof to substantiate this claim). It is also growing!

YoY Revenue grew at 12%.

What the market didn’t like

Operating cash flow came in much lower than before, due to non-structural issues- working capital outflow, and higher receivables.

Nordic revenue fell 28% YoY + Fines = Nordic bear case.

Flat customer growth.

Brazil hiked CCR tax from 12% to 18%

Why I think the market is wrong

The company now trades at a forward EV/EBITDA of ~6 in an industry where similar comps trade at EV/EBITDA of 15. So Betsson is undervalued on peer and standalone basis.

Extremely well run, CEO/Founder is an absolute champion if you look at how he allocates capital and positions for growth. They also have a tech platform they rent out.

Cash flow conversion was a temporary working capital flux.

LATAM is growing fast and is their 2nd biggest revenue by Geography.

Nibble more on the way down

Betsson is already one of my biggest position, I will continue to nibble if it goes lower, I think now is a fine entry point to start building a position.

Obviously this is not financial advice, do your own DD.