Before we get into my new picks a quick position update.

I am quite chuffed with JCU Corporation, up 47% since my post in December. It hasn’t blasted off like other bottleneck plays- but it was always the most compelling Risk to Reward play for me, and I had this sitting at a 40% position initially.

I have reduced exposure because my portfolio suddenly became a one-trick pony, and I’d rather not have all my eggs in one basket.

JCU Corporation (4975.T) Update

Increased operating profit by +16.4% YoY with the chemicals segment up +9.5% YoY.

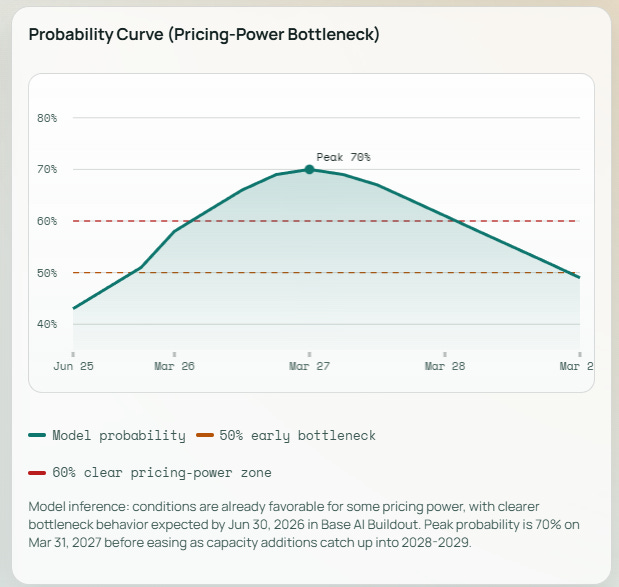

One question I have been trying to answer relentlessy is the bottleneck potential for names like JCU Corporation and C. Uyemura.

JCU Corporation has more optionality towards hybrid bonding in HBM with its TIPHARES brands - so it might see more upside late 2027, 2028.

C. Uyemura has more direct exposure to the current AI buildout in its chemicals segment “Wafers & PKG”.

But could the chemicals used hit a bottleneck?

The graph below is for C. Uyemura specifically, BUT, and huge BUT, this information relies heavily on my understanding of their processes.

A bottleneck would occur for chemicals because qualification takes long, there could be a point at which engineers are waiting for new capacity to be qualified but chemicals production capacity hit a bottleneck. But- huge disclaimer- I need to confirm this. If I can, JCU and C. Uyemura could be an early bottleneck play.

I am looking for any expert in this field to please reach out to me regarding the bottleneck potential here.

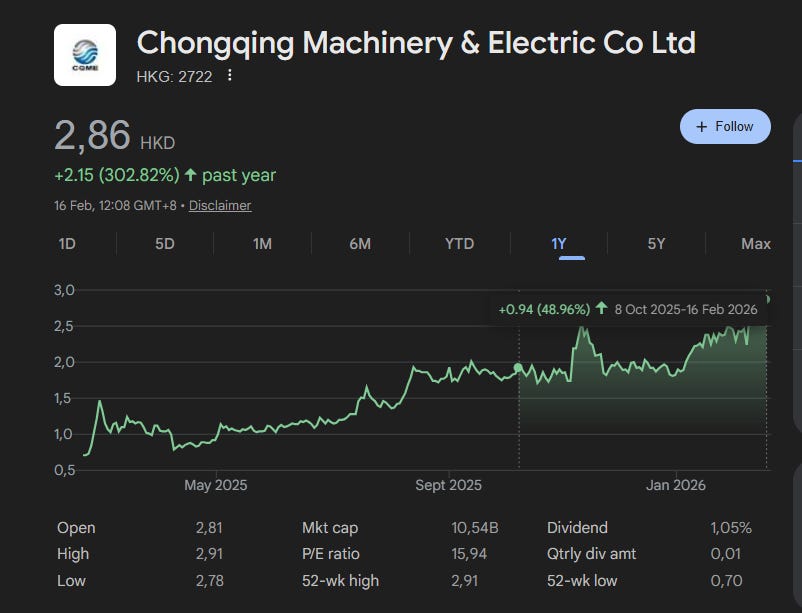

The other AI adjacent plays I profiled: Wasion Holdings and ChongQing Machinery & Electric Co LTD have both done even better. - Sometimes just recognizing the value others are putting out on Substack and X is all you need to beat the benchmark twice over.

Ever grateful to Maius Partners for ChongQing Unpacking Uncertainty for Wasion Holdings. If you want some alpha- follow these guys. Unpacking Uncertainty with only 456 subs on Substack? Undervalued.

Wasion Holdings (3393.HK) Update

Wasion Holdings doubling in share price since the mention. And I took some profits yesterday. But I am also still holding a position as Wayon Energy gets spun-off.

Wayon Energy has three business segments:

1- Smart Distribution Network: Smart Switchgear, high-efficiency transformers, and “Smart Distribution” solutions.

2- Data Center: Power infrastructure projects for power distribution modules, IT containers, HVDC power supply systems. There will be massive growth for this many years out.

3- Energy storage. Energy storage systems and PV + storage microgrids.

The big story is value-unlocking. Wasion is proposing to spin-off Wayon Energy.

I believe the share price has increased in part due to the value-unlock and most-part due to the fact that the market realizes its an AI buildout beneficiary.

ChongQing Machinery & Electric Co LTD (2722.HK)

2722.HK doing a solid 40% but still looking fairly priced and still largerly exposed to the AI buildout in China, which seems to lag behind the U.S.

So what’s next? What do I do with my big bag of profits?

Well I have two new picks. One is quite under-followed, the other has very recently started making the rounds on X.com

I believe both are worthy investments.